|

|

|

|

|||||

|

|

|

EMCOR Group, Inc. EME offers services across mechanical and electrical construction, and industrial and energy infrastructure, alongside building services. Its business model highlights several organic and inorganic efforts that are key to its growth momentum. However, besides inorganic efforts contributing to its growth, the organic strategies and favorable market fundamentals are proving to be single-handedly incremental to its revenue and profit visibility.

EME’s organic growth is attributable to excellence in execution, disciplined contract management and productivity enhancements enabled by Virtual Design and Construction (VDC), Building Information Modeling (BIM) and prefabrication capabilities. Moreover, a critical indicator of sustained organic momentum is the strength of EMCOR’s Remaining Performance Obligations (RPOs), which reached a record $12.6 billion, up 29% year over year, with more than 80% of the 2025 RPO growth in data centers coming organically. The network and communications end markets, particularly data centers, remain a powerful engine for multi-year growth. Mechanical and electrical construction revenues tied to this segment nearly doubled year over year, reflecting both scale and strategic investment in expanding into new geographies.

Apart from data centers, organic growth has been witnessed in health care, manufacturing and industrial, water and wastewater, and mechanical services. These diverse growth vectors reduce dependency on any single end market, supporting stable long-term organic expansion.

Owing to these favorable market trends, EMCOR highlighted high-single-digit to low-double-digit organic growth in the long term, with a robust project pipeline and a deep presence across mission-critical construction markets, catalyzing prospects. With strong execution, increasing productivity and secular demand tailwinds (especially in data centers), EMCOR appears well-positioned to maintain its high-single-digit organic growth trajectory.

EMCOR faces substantial competition in the market surrounding industrial and energy infrastructure, engineering and construction services from renowned market players, including Fluor Corporation FLR and MasTec, Inc. MTZ.

Fluor operates at the opposite end of the market as a global, full-service EPC house with deep engineering, heavy-civil and process capabilities. Its space includes winning the largest, technically complex energy and LNG projects where scale, integrated engineering and turnkey delivery are decisive. Contrarily, MasTec overlaps with EMCOR on power delivery and infrastructure. But it tilts more toward multi-discipline program execution across renewables, grid interconnection and communications backed by a recent surge in clean-energy backlog that gives it muscle on large bundled awards.

EMCOR’s competitive advantage is pragmatic rather than exotic: a broad service network that converts project wins into recurring maintenance and facility-lifecycle revenues, plus the financial flexibility to pursue targeted acquisitions that fill geographic or capability gaps. This positioning makes EME highly competitive for distributed energy, data-center electrification and industrial retrofit work where fast mobilization and long-term service contracts matter. Notably, Fluor’s competitive edge lies in mega EPC complexity, while that of MasTec lies in bundled renewables-to-delivery programs.

Shares of this Connecticut-based infrastructure service provider have tumbled 2.7% in the past three months, underperforming the Zacks Building Products - Heavy Construction industry and the S&P 500 index, but outperforming the broader Construction sector.

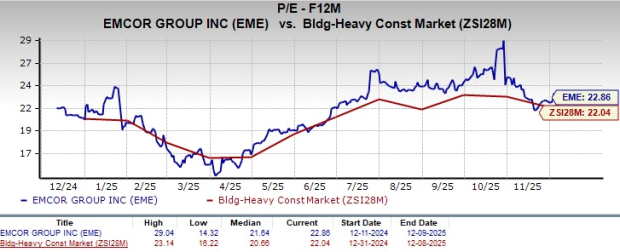

EME stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 22.86, as evidenced by the chart below.

EME’s earnings estimates for 2025 and 2026 have trended upward in the past 60 days to $25.24 and $27.41 per share, respectively. The revised estimates for 2025 and 2026 imply year-over-year growth of 17.3% and 8.6%, respectively.

EMCOR stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 hours | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-10 |

AI Data-Center Boom Has 'Longer Legs Than People Think': Infrastructure Veteran

MTZ

Investor's Business Daily

|

| Jul-09 | |

| Jul-07 | |

| Jul-07 | |

| Jul-01 | |

| Jul-01 | |

| Jul-01 | |

| Jul-01 | |

| Jun-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite