|

|

|

|

|||||

|

|

|

Five9 (FIVN) shares have declined 49.1% in the trailing 12 months, significantly underperforming the Zacks Computer and Technology sector's return of 27.3% and the Zacks Internet Software industry's appreciation of 4.5%. This underperformance is due to the headwinds from a challenging macroeconomic environment that pressured enterprise spending and a transitional period as FIVN recalibrated its commercial business while building AI capabilities.

However, FIVN's prospects are expected to benefit from surging demand for AI-powered customer experience solutions. Its enterprise AI products, unified cloud platform and strengthening bookings momentum continue to support its competitive standing.

For the year 2025, FIVN expects revenues between $1.1435 - $1.1495 billion, with an adjusted EBITDA margin of approximately 23%. For 2026, the company anticipates exceeding a non-GAAP EPS of $3.14, with adjusted EBITDA margin expanding to 24% or higher and annual free cash flow reaching approximately $175 million.

FIVN's differentiation lies in a platform that manages both AI agents and human agents using the full conversational history across every channel. The contact centre is often a company’s richest data repository and Five9’s ability to stitch together complete customer relationships—rather than isolated transactions—creates a learning loop that continually improves accuracy and personalisation.

AI point solutions cannot replicate this capability because they only see isolated transactions. This platform advantage has helped FIVN attract over 3,000 customers globally and deliver its highest number of new $1 million-plus ARR logo wins in two years during the third quarter of 2025.

Enterprises are consolidating around platforms that combine automation, intelligent routing and contextual data and Five9 is benefiting directly from this shift. In the third quarter of 2025, enterprise AI revenue grew 41% year over year and AI bookings rose more than 80%, signalling broad adoption.

Partnerships are amplifying this momentum. The launch of Five9 Fusion for ServiceNow NOW in September 2025 introduced turnkey transcription, intelligent routing and AI-generated summaries into a single workflow, helping customers reduce handle times and improve agent productivity. ServiceNow-related bookings have quadrupled year to date, highlighting strong demand for integrated workflows.

Momentum with Salesforce CRM remains robust as well, with bookings up over 60% due to deeper adoption of the Fusion integration framework. Alphabet’s GOOGL Google Cloud Marketplace partnership has tripled FIVN’s pipeline since early 2025, expanding reach across global and regulated industries.

The partnerships with ServiceNow, Salesforce and Alphabet position FIVN to capture a higher share in the $24 billion cloud-contact-centre market and participate meaningfully in the $210 billion AI-driven labour-arbitrage opportunity.

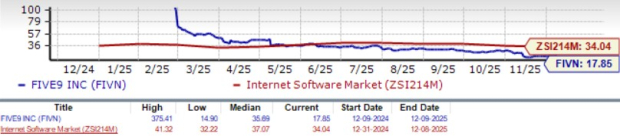

FIVN shares appear attractively valued with a Value score of A, suggesting a favourable valuation at current levels. In terms of the forward 12-month Price/Earnings, FIVN is trading at 17.85X, considerably lower than the industry's 34.04X and the sector's 29.04X. This discount reflects the stock’s steep decline over the past year rather than a deterioration in fundamentals.

Given the company’s strengthening AI pipeline, expanding enterprise adoption and improving profitability profile, this reset provides investors with an appealing entry point. The combination of discounted valuation and a clearer multi-year growth trajectory positions FIVN well for potential re-rating as execution remains steady and AI-driven demand accelerates.

For 2025, the Zacks Consensus Estimate for EPS is pegged at $2.93, up by 5 cents over the past 60 days. The figure indicates 18.62% year-over-year growth, reflecting increasing confidence in FIVN’s growing subscription-led mix.

The consensus mark for fourth-quarter 2025 EPS is pegged at 79 cents, up by a penny over the past 60 days. The figure suggests 1.28% year-over-year growth, suggesting a stabilising demand environment and support expectations of continued operational improvement.

Five9, Inc. price-consensus-chart | Five9, Inc. Quote

Even though FIVN shares have underperformed recently, the company is benefiting from strengthening fundamentals, a clear data-driven platform advantage and accelerating demand for AI-powered customer-experience solutions. Its expanding ecosystem, which is supported by strategic partnerships with ServiceNow, Salesforce and Alphabet, continues to deepen enterprise engagement and widen its competitive reach. With the stock trading at a meaningful valuation discount and earnings estimates trending higher, FIVN’s setup appears favourable for long-term investors. The stock currently has a Zacks Rank #2 (Buy), indicating that investors may consider accumulating shares at current levels. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 38 min | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 |

Big Companies Are Starting to Hire Again, Defying Predictions of AI Wipeout

GOOGL

The Wall Street Journal

|

| Jul-26 | |

| Jul-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite