|

|

|

|

|||||

|

|

|

Wrapping up Q3 earnings, we look at the numbers and key takeaways for the household products stocks, including Kimberly-Clark (NASDAQ:KMB) and its peers.

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

The 10 household products stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was 1% above.

While some household products stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.1% since the latest earnings results.

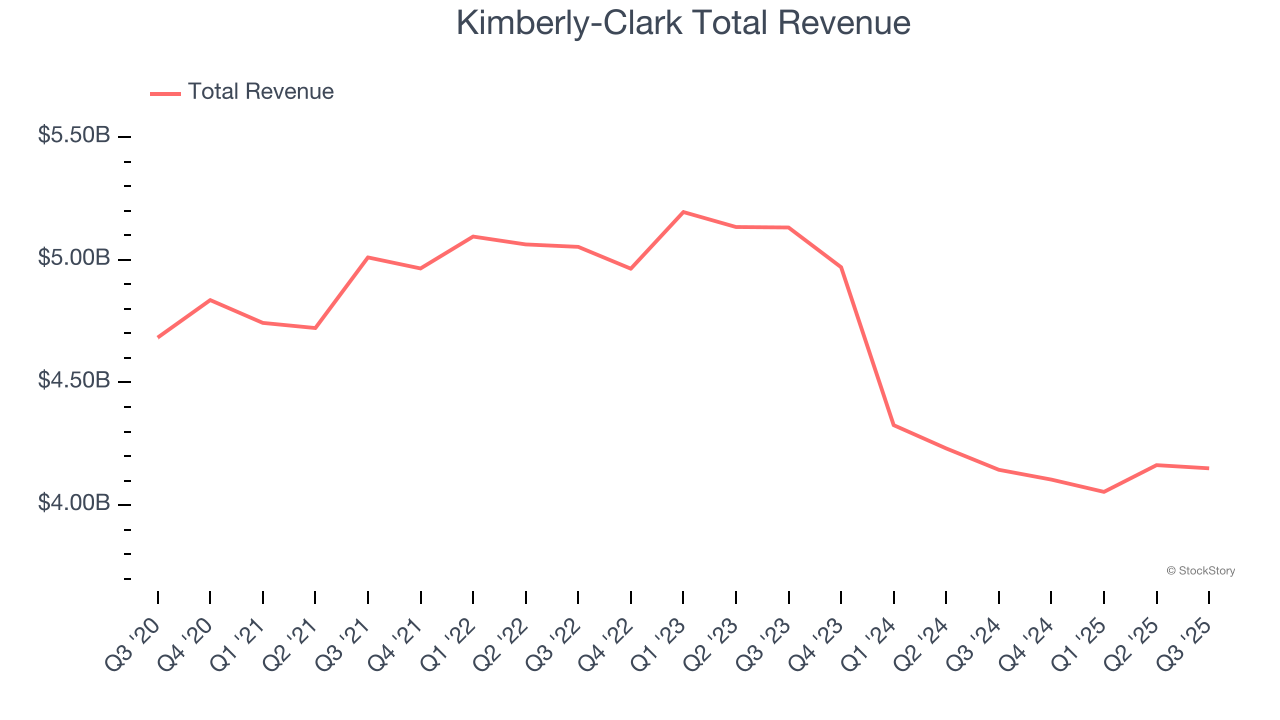

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NYSE:KMB) is now a household products powerhouse known for personal care and tissue products.

Kimberly-Clark reported revenues of $4.15 billion, flat year on year. This print was in line with analysts’ expectations, and overall, it was a satisfactory quarter for the company with a decent beat of analysts’ EBITDA estimates but gross margin in line with analysts’ estimates.

"The operating environment remains dynamic, but we continue to execute our strategy with discipline and excellence as we play to win," said Kimberly-Clark Chairman and CEO, Mike Hsu.

Unsurprisingly, the stock is down 11.6% since reporting and currently trades at $103.15.

Is now the time to buy Kimberly-Clark? Access our full analysis of the earnings results here, it’s free for active Edge members.

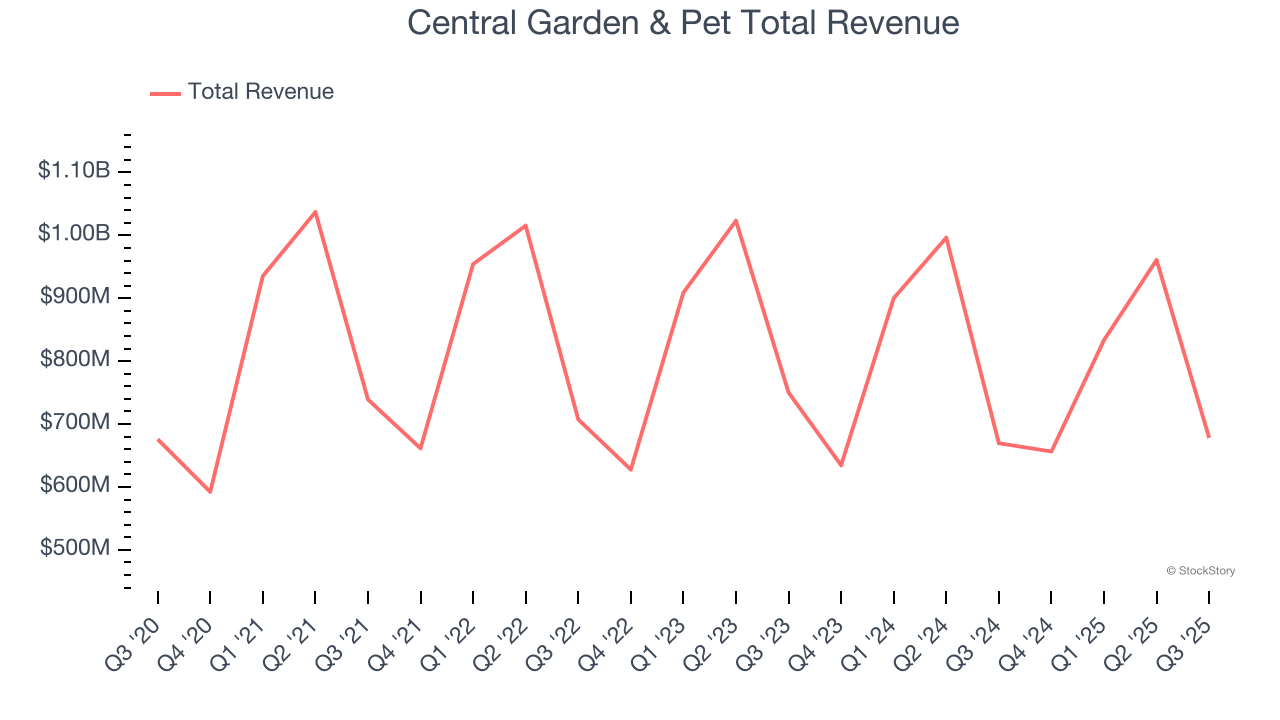

Enhancing the lives of both pets and homeowners, Central Garden & Pet (NASDAQ:CENT) is a leading producer and distributor of essential products for pet care, lawn and garden maintenance, and pest control.

Central Garden & Pet reported revenues of $678.2 million, up 1.3% year on year, outperforming analysts’ expectations by 3.9%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

The market seems happy with the results as the stock is up 8.1% since reporting. It currently trades at $33.98.

Is now the time to buy Central Garden & Pet? Access our full analysis of the earnings results here, it’s free for active Edge members.

Masterminds behind the viral Energizer Bunny mascot, Energizer (NYSE:ENR) is one of the world's largest manufacturers of batteries.

Energizer reported revenues of $832.8 million, up 3.4% year on year, exceeding analysts’ expectations by 0.8%. Still, it was a softer quarter as it posted EPS guidance for next quarter missing analysts’ expectations significantly and a miss of analysts’ gross margin estimates.

As expected, the stock is down 20.5% since the results and currently trades at $18.96.

Read our full analysis of Energizer’s results here.

Founded in 1913 with bleach as the sole product offering, Clorox (NYSE:CLX) today is a consumer products giant whose product portfolio spans everything from bleach to skincare to salad dressing to kitty litter.

Clorox reported revenues of $1.43 billion, down 18.9% year on year. This number beat analysts’ expectations by 2%. It was a strong quarter as it also logged an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ revenue estimates.

Clorox had the slowest revenue growth among its peers. The stock is down 5.4% since reporting and currently trades at $103.20.

Read our full, actionable report on Clorox here, it’s free for active Edge members.

Best known for its aluminum foil, Reynolds (NASDAQ:REYN) is a household products company whose products focus on food storage, cooking, and waste.

Reynolds reported revenues of $931 million, up 2.3% year on year. This result topped analysts’ expectations by 3.4%. Overall, it was a strong quarter as it also put up revenue guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ organic revenue estimates.

The stock is up 2.8% since reporting and currently trades at $24.36.

Read our full, actionable report on Reynolds here, it’s free for active Edge members.

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Mar-24 | |

| Mar-24 | |

| Mar-20 |

Inside the 'Buff Baby' Project That Questioned Everything About Diapers-and How We Shop

KMB

The Wall Street Journal

|

| Mar-18 | |

| Mar-11 | |

| Mar-11 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-04 | |

| Mar-04 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite