|

|

|

|

|||||

|

|

|

Leading discount retailer Costco has seen its stock struggle to gain momentum in 2025, but a positive quarterly result could help spark a turnaround.

Costco is poised to report its fiscal first-quarter earnings on Thursdayevening. We expect continued strength from the company’s membership-driven model amid a value-conscious retail landscape.

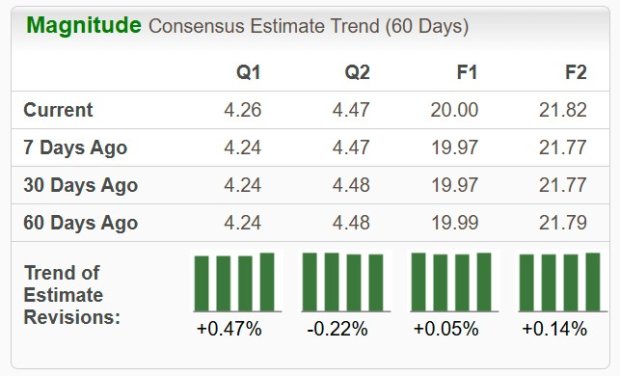

Our Zacks Consensus Estimate shows Q1 EPS projections pegged at $4.26, reflecting an 11.5% increase year-over-year. Estimates have inched up slightly over the past 60 days. Total revenues are anticipated to come in at $67.3 billion, up 8.3% from the prior-year quarter. This outlook builds on preliminary sales data showing fiscal Q1 net sales of $65.98 billion, an 8.2% rise.

Costco stands tall as a dominant force in the warehouse retail sector. Its distinctive membership-based model and emphasis on bulk sales differentiate the company from traditional competitors.

Total comparable sales in the latest quarter rose 6.4%, driven by gains of 5.9% in the U.S., 6.5% in Canada, and 8.8% in Other International markets. The figures reflect steady consumer spending trends as we inch closer to peak holiday activity.

E-commerce sales remain a key growth engine, with digitally enabled comparable sales surging over 20% in the quarter based on early indicators, extending a trend of double-digit gains seen in recent periods. This follows 15.6% e-commerce comp growth in Q4 FY25, driven by investments in Costco Logistics and targeted online promotions for big-and-bulky items like furniture and appliances.

While e-commerce represents a relatively minor portion of overall sales, its significance has been steadily increasing in recent years. Its margin-accretive nature and synergy with in-store traffic position it as a differentiator against pure-play online rivals.

Membership trends continue to underpin Costco's profitability, with global renewal rates holding steady at over 90%. Preliminary data suggests membership fee income could rise another 9% in FY26 as online sign-ups introduce younger demographics and executive upgrades boost higher-margin revenue.

Consumer spending patterns reveal a shift toward value and replenishment with shoppers prioritizing groceries, Kirkland Signature private labels, and lower-priced essentials over discretionary dining out, amid lingering inflation and economic uncertainty from events like the recent government shutdown. This favors Costco's bulk model where basket sizes remain robust, though some softening in non-essentials like apparel reflects broader caution.

Risks ahead of this evening’s announcement include SNAP reductions and a potential consumer pullback, but Costco's premium positioning and 93% U.S. renewal rates suggest outperformance versus peers amid a promotional holiday season.

The Zacks Rank #3 (Hold) rating for Costco COST stock indicates steady but tempered expectations. While the stretched valuation (44.4 times forward earnings) remains a concern, Costco boasts a remarkable track record of exceeding earnings estimates, with only three misses on the bottom line in the past five years.

Investors will be closely monitoring this evening’s results for signs of sustained momentum. Costco’s growth strategies, better price management, and promising membership trends could help the stock resume its former glory.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite