|

|

|

|

|||||

|

|

|

The market is underestimating Nvidia's growth potential for 2026.

The company's massive backlog, a potential increase in its margins, and the recent announcement by President Trump regarding its Chinese business should help Nvidia surpass estimates next year.

In 2025, Nvidia (NASDAQ: NVDA) became the world's largest company and briefly touched a market cap of $5 trillion. It also delivered yet another year of healthy returns to investors. The share price of the semiconductor giant is up 36% so far this year, and that's impressive considering it endured a few dips along the way.

Recent investor sentiment hasn't been positive, with the company's shares dropping 9.7% since the beginning of November. Concerns about circular financing in the artificial intelligence (AI) infrastructure market, an AI bubble, and the sustainability of the inflated levels of AI capital spending are weighing on the stock of late.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

However, don't be surprised to see Nvidia coming out of its recent rut and delivering impressive returns once again in 2026. There's also a possibility that the stock price could double by the end of 2026. Here's why I'm so bullish on Nvidia in 2026.

Image source: Getty Images.

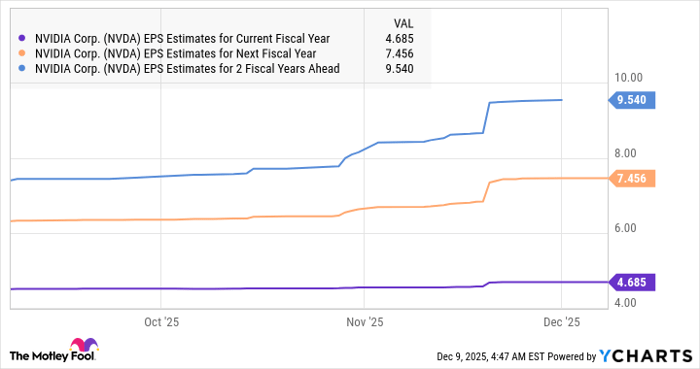

Nvidia manages to sustain its outstanding growth levels despite an already high revenue base. It's on track to end the ongoing fiscal year 2026 (which ends Jan. 31, 2026) with $213 billion in revenue, an increase of 63% from the previous year. Consensus analyst estimates project Nvidia's earnings to grow by 57% this fiscal year to $4.69 per share.

The good part is that analysts following Nvidia expect to maintain solid growth levels in fiscal 2027. Consensus estimates project its revenue to jump by 48% next year to $316 billion.

The company's earnings growth is expected to accelerate slightly to 59%, landing at $7.46 per share. But what's worth noting is that Nvidia's earnings estimate for 2026 was recently revised higher. It's not surprising to see why that's the case. Nvidia is likely to benefit from a mix of faster revenue growth and margin improvements next year.

Data by YCharts.

The company's revenue forecast for the current quarter points toward a 65% jump from the year-ago period, clearly indicating that it's going into the new year with momentum on its side. A massive backlog supports this solid guidance. Nvidia's AI chip order book is worth $500 billion for 2025 and 2026 combined and puts the company in an ideal position to grow at a faster-than-expected pace.

Given that Nvidia generated $167 billion in data center revenue in the past year, it's likely to clock another $58 billion in sales in the current quarter (considering that 90% of Nvidia's total sales come from the data center segment and the company is expecting overall revenue of $65 billion this quarter). That leaves Nvidia with a potential backlog of $275 billion in the data center business for next year (as it would have sold $225 billion worth of chips in the past five quarters).

However, the $500 billion backlog isn't a hard ceiling as Nvidia continues to receive more orders for its chips, as CFO Colette Kress remarked on the latest earnings call. Kress said that the backlog number "will grow" and there's an "opportunity for us to have more on top of the $500 billion that we announced." Moreover, Nvidia has been cleared by the Trump administration to sell its H200 data center GPUs to China, paving the way for even stronger growth next year.

Nvidia's data center business could end up outperforming expectations in 2026, paving the way for a bigger increase than the 48% growth that analysts are forecasting. Additionally, the company expects to hold its gross margin to around the mid-70% range next year.

That points toward a slight improvement over the company's gross margin this year. Nvidia's non-GAAP gross margin was 71% in fiscal Q1, followed by 72.2% and 73.6%, respectively, in the following two quarters.

As the margin ticks higher and revenue comes in at stronger-than-expected levels, there is a possibility that Nvidia's earnings will exceed the 59% growth that analysts are expecting next year.

Assuming Nvidia can deliver even 65% earnings growth next year, its bottom line could hit $7.74 per share (up from this year's estimated earnings of $4.69 per share). That would be significantly higher than the 14% earnings growth that the S&P 500 index is expected to deliver next year. Now, Nvidia stock trades at 29 times forward earnings, which is well below the U.S. tech sector's average earnings multiple of 46.

Given that Nvidia's bottom line is likely to grow at a much faster pace than the broader market and has the potential to consistently outperform analysts' expectations in the coming year, the market should ideally reward it with a higher multiple. Even if the company's stock trades in line with the U.S. tech sector's average earnings multiple of 46 and achieves $7.74 per share in earnings, its stock price could jump to $358.

That's close to double Nvidia's current stock price. This is why investors can still consider buying this AI stock going into the new year.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $499,978!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,126,609!*

Now, it’s worth noting Stock Advisor’s total average return is 971% — a market-crushing outperformance compared to 195% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of December 8, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

| 1 hour | |

| 1 hour | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite