|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Gilead Sciences, Inc. GILD and Bristol Myers Squibb BMY are leading biotechnology companies with broad and diverse portfolios and a global footprint.

Gilead Sciences is a pioneer in developing treatments for human immunodeficiency virus (HIV). The company’s wide portfolio also includes drugs for liver, hematology/oncology and inflammation/respiratory diseases.

On the other hand, Bristo Myers is focused on discovering, developing and delivering transformational drugs for oncology, hematology, immunology, cardiovascular, neuroscience and other diseases. BMY also has a robust pipeline of promising candidates.

Both of these biotech giants have strong footholds in their targeted businesses, delivering consistent returns to shareholders. In such a scenario, choosing one stock over the other can be tricky. Let us delve into their fundamentals, potential growth prospects, challenges and valuation levels to make a prudent choice.

Gilead is a dominant player in the HIV market. The company’s flagship drug, Biktarvy (bictegravir 50 mg/emtricitabine 200 mg/tenofovir alafenamide 25 mg, BIC/FTC/TAF), for HIV-1 infection has become the number-one prescribed regimen for both treatment-naïve and switch patients. It continues to maintain its dominant position with an increasing market share for treatment and prevention. Descovy continues to drive growth as a prevention option for HIV and has maintained over 40% market share in pre-exposure prophylaxis (PrEP) in the United States.

Late-stage studies, PURPOSE 1 and PURPOSE 2, validated lenacapavir’s potential to prevent HIV. A potential approval of twice-yearly lenacapavir for PrEP will significantly boost Gilead’s HIV franchise, as lenacapavir needs to be taken twice yearly, unlike daily oral pills.

GILD has also collaborated with Merck MRK to evaluate the investigational combination of islatravir and lenacapavir for the treatment of HIV.

Gilead’s oncology portfolio, comprising the Cell Therapy franchise and breast cancer drug Trodelvy, has diversified its overall business. The breast cancer drug Trodelvy has performed well since its approval. GILD has multiple ongoing studies looking to expand Trodelvy’s label further.

However, the Cell Therapy franchise, comprising Yescarta and Tecartus, is currently under pressure due to competitive headwinds in the United States and Europe that are expected to continue in 2025.

The Liver Disease portfolio includes treatments for HCV, chronic hepatitis B virus (HBV) and chronic hepatitis delta virus (HDV). Gilead is making efforts to expand this franchise further.

The recent FDA approval of seladelpar, under the brand name Livdelzi, for the treatment of primary biliary cholangitis has strengthened the liver disease portfolio.

As of Dec. 31, 2024, Gilead’s total debt-to-total-capital ratio was 59%. GILD had $10 billion in cash, cash equivalents and marketable debt securities and long-term debt of $25 billion at the end of 2024.

BMY’s Growth Portfolio, comprising drugs like Reblozyl, Breyanzi, Camzyos and Opdualag, has stabilized its revenue base amid generic competition for its legacy drugs. Thalassemia drug Reblozyl has put up a stellar performance since its approval, with strong growth in the United States and international markets. The drug is expected to contribute significantly in the coming decade.

Sales of its oncology drug, Opdualag, have also been robust, fueling the top line. Strong growth in the U.S. market and encouraging uptake in newly launched markets have boosted sales. Strong momentum in Camzyos should further drive growth.

Opdivo continues to maintain momentum on consistent label expansions. The FDA approval of Opdivo Qvantig (nivolumab and hyaluronidase-nvhy) injection for subcutaneous use should help extend the impact of its immuno-oncology franchise to patients into the next decade. Other drugs like Zeposia and Krazati should also contribute to top-line growth.

The company has made strategic acquisitions to broaden its portfolio and drive top-line growth. The recent FDA approval for xanomeline and trospium chloride (formerly KarXT), an oral medication for the treatment of schizophrenia in adults, was approved under the brand name Cobenfy. The approval of Cobenfy for schizophrenia broadens BMY’s portfolio and validates the acquisition of Karuna Therapeutics.

While the newer drugs boost sales, generic competition for legacy drugs, which account for the lion’s share of total revenues, is a major headwind and will impact top-line growth for the time being.

Nonetheless, BMY is looking to boost its bottom line through cost-cutting initiatives.

While BMY’s strategy of acquiring companies with promising drugs/candidates is encouraging, this has resulted in colossal debt to finance these acquisitions. As of Dec. 31, 2024, Bristol Myers’ total debt-to-total capital was a whopping 75.2%. The company had cash and equivalents of $10.3 billion and a long-term debt of $47.6 billion as of the same date.

The Zacks Consensus Estimate for GILD’s 2025 sales implies a year-over-year decrease of 0.39%, while that for earnings per share (EPS) suggests a year-over-year increase of 70.13%. EPS estimates for both 2025 and 2026 have moved north in the past 60 days.

The Zacks Consensus Estimate for BMY’s 2025 sales implies a year-over-year decrease of 5.11% while that for EPS suggests a year-over-year increase of 489.57%. EPS estimates for both 2025 and 2026 have moved south in the past 60 days.

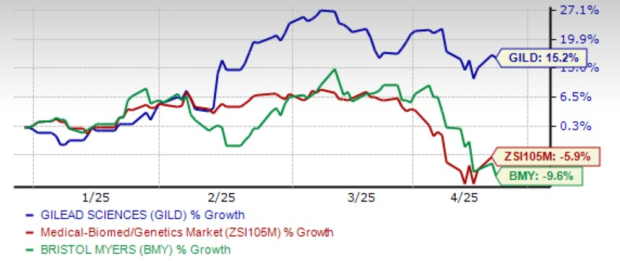

From a price-performance perspective, GILD has fetched better returns than BMY so far in the year. Shares of GILD have gained 15.2%, while those of BMY have lost 9.6%. The industry has declined 5.9% in the said period.

From a valuation standpoint, as the biotech industry has very few players with approved drugs, we use the P/E ratio of the large-cap pharma industry to compare these companies. Going by the same, GILD is more expensive than BMY. GILD’s shares currently trade at 13.23 forward earnings, higher than 7.61 for BMY.

Image Source: Zacks Investment Research

GILD and BMY’s attractive dividend yield is a strong positive for investors. However, BMY’s dividend yield of 4.83% is higher than GILD’s 2.97%.

Since both GILD and BMY currently carry a Zacks Rank #3 (Hold), choosing one stock over the other is a complex affair. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Gilead’s efforts to constantly innovate its HIV portfolio should enable it to maintain growth. A strong catalyst for the stock going forward is a potential approval of lenacapavir for HIV prevention (target action date in June 2025).

BMY’s efforts to revive the top line in the face of generic challenges for key drugs are commendable. However, we believe there is still time before the efforts reap a harvest for the company. The outlook for 2025 does not look bright as well.

Hence, GILD is a better pick for now despite its pricey valuation as we believe there is room for growth buoyed by solid fundamentals, potential approval of lenacapavir for HIV prevention and positive estimate revisions.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-22 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite