|

|

|

|

|||||

|

|

|

Merck MRK is focusing on driving its long-term growth with its new products and a promising set of pipeline candidates as its blockbuster PD-L1 inhibitor, Keytruda, faces patent expiration in 2028.

Keytruda, approved for several types of cancer, alone accounts for more than 50% of the company’s pharmaceutical sales. The drug has played a key role in driving Merck’s steady revenue growth over the past few years. Keytruda recorded sales of $23.3 billion in the first nine months of 2025, up 8% year over year.

As Keytruda approaches its expected loss of exclusivity in 2028, Merck’s expanding pipeline and newly launched products are expected to shape the company’s future business layout.

MRK’s phase III pipeline has almost tripled since 2021, driven by in-house pipeline progress and the addition of new candidates through various mergers and acquisitions (M&A) deals. This has positioned the company to launch around 20 new vaccines and drugs over the next few years, with many having blockbuster potential, creating long-term value.

These include Merck’s new 21-valent pneumococcal conjugate vaccine, Capvaxive, and pulmonary arterial hypertension (PAH) drug, Winrevair. Merck is pinning hopes on these two drugs to boost its top line once Keytruda loses exclusivity. Both products have witnessed a strong launch so far.

Merck’s newest respiratory syncytial virus (RSV) antibody, Enflonsia (clesrovimab), was approved in the United States in June 2025, while it is under review in the EU.

The company’s promising candidates in late-stage development include enlicitide decanoate/MK-0616, an oral PCSK9 inhibitor for hypercholesterolemia, tulisokibart, a TL1A inhibitor for ulcerative colitis, bomedemstat/MK-3543 for essential thrombocythemia, myelofibrosis and polycythemia vera, nemtabrutinib/MK-1026 for hematological malignancies and Daiichi-Sankyo-partnered antibody-drug conjugates (ADCs).

Merck, along with Daiichi Sankyo, is co-developing three DXd ADCs — patritumab deruxtecan, ifinatamab deruxtecan and raludotatug deruxtecan for several types of cancer indications.

A fixed-dose combination of doravirine and islatravir for the treatment of HIV is under review in the United States, with an FDA decision expected in April next year.

Merck has also made substantial investments in strategic M&A deals in recent times to build a more durable long-term portfolio. The company has struck multi-billion-dollar deals with Chinese biotechs like Hansoh Pharma, LaNova Medicines and Hengrui Pharma to expand its pipeline in various areas.

Merck recently inked an agreement to acquire Cidara Therapeutics for $9.2 billion. The impending acquisition will add Cidara’s lead asset, CD388, which is currently in late-stage development for the prevention of seasonal influenza. Earlier this year, Merck acquired Verona Pharma for $10 billion, which added Ohtuvayre, a novel, first-in-class maintenance treatment for chronic obstructive pulmonary disease, to MRK’s commercial portfolio.

However, it remains to be seen whether Merck’s new products and pipeline candidates will be sufficient to help the company successfully navigate the Keytruda LOE period and potential competition for the drug.

Keytruda faces competition from other PD-L1 inhibitors, including Bristol Myers’ BMY Opdivo, Roche’s RHHBY Tecentriq and AstraZeneca’s AZN Imfinzi.

BMY’s Opdivo, like Keytruda, is approved across multiple cancer types, including lung, melanoma and kidney cancers. Bristol Myers recorded $7.35 billion in Opdivo sales during the first nine months of 2025, up 8% year over year.

Tecentriq is Roche’s leading immuno-oncology drug approved for multiple cancer indications. RHHBY recorded CHF 2.61 billion in Tecentriq sales in the first nine months of 2025.

AZN’s Imfinzi generated sales of $4.32 billion in the first nine months of 2025, up 25%, driven by demand growth in lung and liver cancer indications. Imfinzi has strategically expanded its use across multiple cancer indications, strengthening AstraZeneca’s oncology portfolio.

Year to date, shares of Merck have lost 0.4% against the industry’s rally of 13.6%. The stock has also underperformed the sector and the S&P 500 during the same time frame, as seen in the chart below.

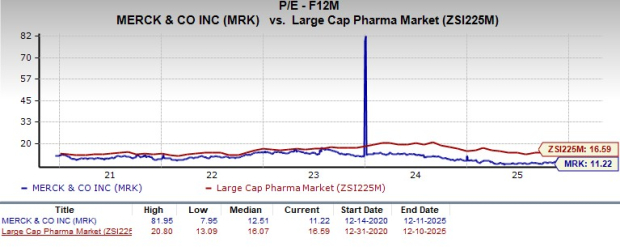

From a valuation standpoint, Merck appears attractive relative to the industry. Going by the price/earnings ratio, the company’s shares currently trade at 11.22 forward earnings, lower than 16.59 for the industry and its 5-year mean of 12.51.

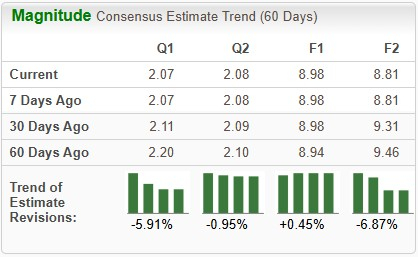

The Zacks Consensus Estimate for 2025 earnings per share has increased from $8.94 per share to $8.98, while the same for 2026 has decreased from $9.46 to $8.81 over the past 60 days.

Merck currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 43 min | |

| 3 hours |

Bristol Myers, NVIDIA join forces to build life sciences most powerful AI factory

BMY

Pharmaceutical Technology

|

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

MSD wins FDA approval for cholesterol pill to help plug Keytruda void

AZN MRK

Pharmaceutical Technology

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite