|

|

|

|

|||||

|

|

|

The Goldman Sachs Group GS shares have been performing remarkably well of late. At present, the stock is trading near its 52-week high of $919.10 hit during Thursday’s trading session.

Over the past year, the GS stock has risen 51.5%, outperforming the industry and its close peers — JPMorgan JPM and Morgan Stanley MS, with gains of 33% and 38.3%, respectively.

Price Performance

With such strong momentum, investors are now wondering whether to hold on to the stock for now or cash out the profit. Let us delve deeper and analyze what is driving growth and whether there is more scope to grow.

Strong M&A Momentum to Aid IB Business: GS’s investment banking (IB) business continues to build on its momentum in 2025, buoyed by a resurgence in global deal-making activity. The bank reported IB fees of $6.8 billion, a 19% year-over-year increase in the first nine months of 2025, driven by higher advisory revenues, indicating a substantial rise in merger and acquisition (M&A) activity. In the third quarter alone, Goldman’s IB revenues jumped 42.5% year over year.

A friendlier rate environment, revived private equity transactions, and the reopening of capital markets supported GS IB business. Notably, GS ended the third quarter as the leader in both announced and completed M&A. The company advised on more than $1 trillion in announced M&A volumes in the first nine months of 2025.

This month, the Federal Reserve implemented its third consecutive 25-basis-point rate cut of this year, reigniting investor optimism. The move is likely to further accelerate deal-making momentum by lowering financing costs and prompting companies to revive delayed M&A and capital-raising plans.

Thus, a strong deal pipeline and sustained leadership in M&A advisory enable Goldman well to extend its deal-making dominance. Notably, given its commanding share of announced deal value, paired with favorable macroeconomic tailwinds, could make 2025 one of Goldman's strongest M&A years in decades.

Strategic Streamlining Progresses Well: The company’s streamlining efforts have been underway for some time as it retreats from the underperforming consumer banking ventures. Under CEO David Solomon, the company has embarked on a deliberate transformation to exit non-core consumer banking and double down on the divisions where Goldman maintains a clear competitive advantage.

In sync with its restructuring efforts, in November 2025, Goldman reached an agreement with ING Bank Slaski to divest its Polish asset management firm, TFI. The deal is targeted for completion in the first half of 2026. In the third quarter of 2025, Goldman completed the sale of its GM credit card business to Barclays. In 2024, Goldman completed the sale of GreenSky. In 2023, it sold its Personal Financial Management unit to Creative Planning and also sold all of Marcus’s loan portfolio, part of its broader retreat from consumer banking.

These moves demonstrate a well-thought-out exit, allowing the company to reallocate capital and attention toward higher-margin, more scalable businesses. The benefits of business restructuring began to show in the numbers. The Global Banking and Markets segment’s net revenues rose 17% year over year in the first nine months of 2025, while the AWM division’s net revenues rose 4% year over year, reflecting growing fee income and strength in private credit. In December 2025, GS agreed to acquire Innovator Capital Management, a leading provider of defined outcome exchange-traded funds (ETFs). The transaction significantly expands Goldman’s active ETF capabilities and is part of a broader pivot toward building “durable revenue streams” through diversified AWM offerings.

Betting Big on Private Equity to Aid Growth: The company is aggressively expanding its private equity and alternatives business through acquisitions, platform enhancements, and the integration of new investment capabilities, which will likely support its growth over the long run.

In sync with this, in October 2025, Goldman agreed to acquire Industry Ventures, a leading venture capital platform that invests across all stages of the venture capital lifecycle. The planned acquisition of Industry Ventures underscores Goldman’s intent to strengthen its position in private markets and expand access to high-growth technology companies for clients globally.

In September 2025, GS partnered with T. Rowe Price in a $1-billion deal to co-develop retirement and wealth products. Later, the firms expanded the partnership to roll out alternative investment offerings for wealthy clients in 2025 and retirement savers in 2026. In January 2025, the company also launched initiatives to grow private credit and other asset classes, including forming the Capital Solutions Group and expanding its alternatives team.

Further, Goldman is expanding its private equity credit services internationally, focusing on Europe, the U.K., and Asia. The company is also expanding distribution of alternative investments to third-party wealth platforms, targeting $8 billion in client assets by 2025-end, up from $5 billion in 2024, alongside an increase in its asset management team dedicated to individual investors. The company's Asset Management unit intends to expand its private credit portfolio to $300 billion by 2029.

Robust Liquidity Aids Capital Distribution: GS maintains a fortress balance sheet, with the Tier 1 capital ratios well above regulatory requirements. This financial strength allows it to return capital to shareholders aggressively through buybacks and a healthy dividend yield.

As of Sept. 30, 2025, cash and cash equivalents were $169 billion, and near-term borrowings were $73 billion. Given its strong liquidity, the company rewards its shareholders handsomely.

Post-clearing the 2025 Fed stress test, the company increased the quarterly dividend by 33.3% to $4 per common share. In the past five years, the company has hiked dividends five times, with an annualized growth rate of 21.8%. Currently, it has a dividend yield of 1.8%.

The Goldman Sachs Group, Inc. Dividend Yield (TTM)

The Goldman Sachs Group, Inc. dividend-yield-ttm | The Goldman Sachs Group, Inc. Quote

JPMorgan raised its dividends six times over the past five years and offers a dividend yield of 1.9%. Morgan Stanley has raised its dividends five times over the past five years and has a dividend yield of 2.2%.

Additionally, Goldman has a share repurchase plan in place. In the first quarter of 2025, the board approved a share repurchase program of up to $40 billion of common stock. At the end of the third quarter, the company had $38.6 billion worth of shares available under authorization.

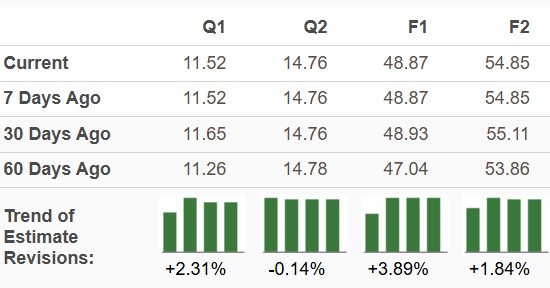

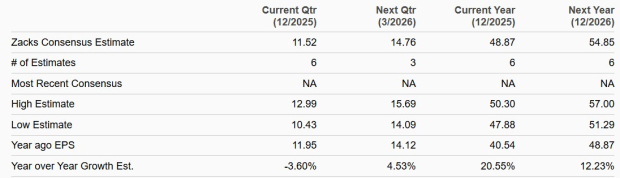

Analysts are bullish on GS. Over the past 60 days, the Zacks Consensus Estimate for 2025 and 2026 earnings has been revised upward.

Estimates Revision Trend

The Zacks Consensus Estimate for Goldman’s 2025 and 2026 earnings implies year-over-year growth of 20.6% and 12.2%, respectively.

Earnings Estimates

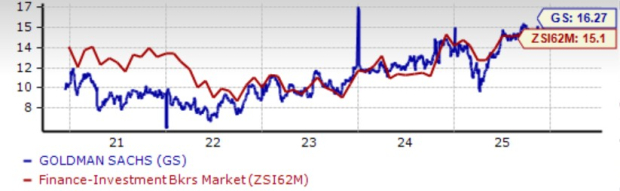

In terms of valuation, the GS stock looks expensive compared with the industry. The stock is trading at a forward price/earnings (P/E) of 16.3X above the industry average of 15.1X. Its peers, JPMorgan and Morgan Stanley, have forward P/E multiples of 15.1X and 17.3X, respectively.

Price-to-Earnings F12M

GS’s ongoing growth initiatives, consistent capital returns, and a steadily improving AWM business provide a strong foundation for long-term financial performance. The rebound in M&A activity and a healthy deal pipeline continue to underpin the firm’s IB momentum, while its robust liquidity profile supports a sustainable and disciplined capital distribution strategy.

In pursuing growth across business segments, operational efficiency remains central to Goldman’s strategy. The company’s recent performance and forward-looking initiatives reaffirm its progress toward achieving its mid-term goals of a 14-16% return on equity and a 60% efficiency ratio.

With resilient earnings prospects and favorable momentum in deal-making and asset management, investors may consider holding on to Goldman’s stock for now to capitalize on its sustained strength and long-term growth trajectory.

The company currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 18 min | |

| 39 min | |

| 48 min | |

| 54 min | |

| 59 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 8 hours | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite