|

|

|

|

|||||

|

|

|

What a brutal six months it’s been for Molina Healthcare. The stock has dropped 42.1% and now trades at $168.08, rattling many shareholders. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for MOH? Find out in our full research report, it’s free for active Edge members.

Founded in 1980 as a provider for underserved communities in Southern California, Molina Healthcare (NYSE:MOH) provides managed healthcare services primarily to low-income individuals through Medicaid, Medicare, and Marketplace insurance programs across 21 states.

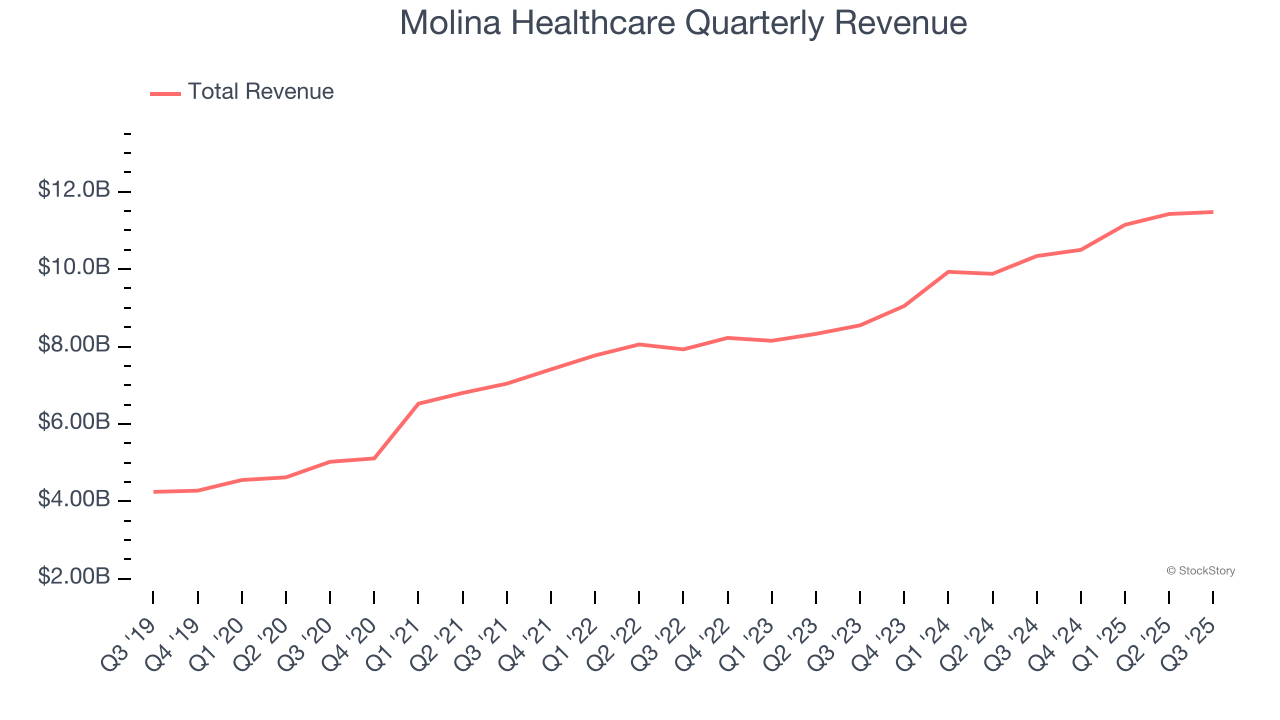

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Molina Healthcare’s sales grew at an impressive 19.3% compounded annual growth rate over the last five years. Its growth surpassed the average healthcare company and shows its offerings resonate with customers.

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $44.55 billion in revenue over the past 12 months, Molina Healthcare boasts impressive economies of scale. It may not be as large as heavyweights such as UnitedHealth Group and The Cigna Group from a topline perspective, but its heft is still an important advantage in a healthcare industry that is heavily regulated, complex, and resource-intensive.

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

Molina Healthcare’s total customers came in at 5.63 million in the latest quarter, and over the last two years, their count averaged 4.2% year-on-year growth. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in landing new contracts.

Molina Healthcare’s merits more than compensate for its flaws. With the recent decline, the stock trades at 14.7× forward P/E (or $168.08 per share). Is now a good time to buy? See for yourself in our full research report, it’s free for active Edge members.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jun-02 | |

| Apr-29 | |

| Apr-29 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-07 | |

| Apr-06 | |

| Mar-17 | |

| Mar-13 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite