|

|

|

|

|||||

|

|

|

Over the past six months, Dine Brands has been a great trade, beating the S&P 500 by 7.8%. Its stock price has climbed to $33.86, representing a healthy 21.7% increase. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Dine Brands, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Despite the momentum, we're cautious about Dine Brands. Here are three reasons there are better opportunities than DIN and a stock we'd rather own.

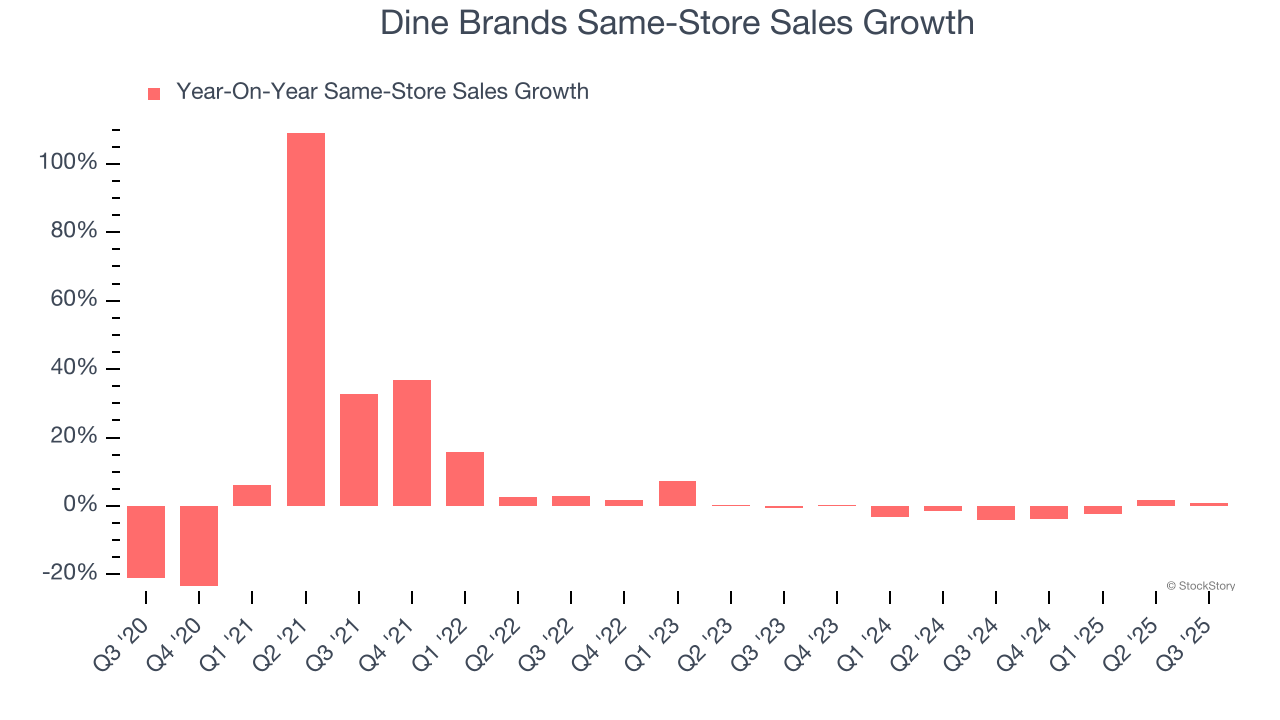

Same-store sales is a key performance indicator used to measure organic growth at restaurants open for at least a year.

Dine Brands’s demand has been shrinking over the last two years as its same-store sales have averaged 1.5% annual declines.

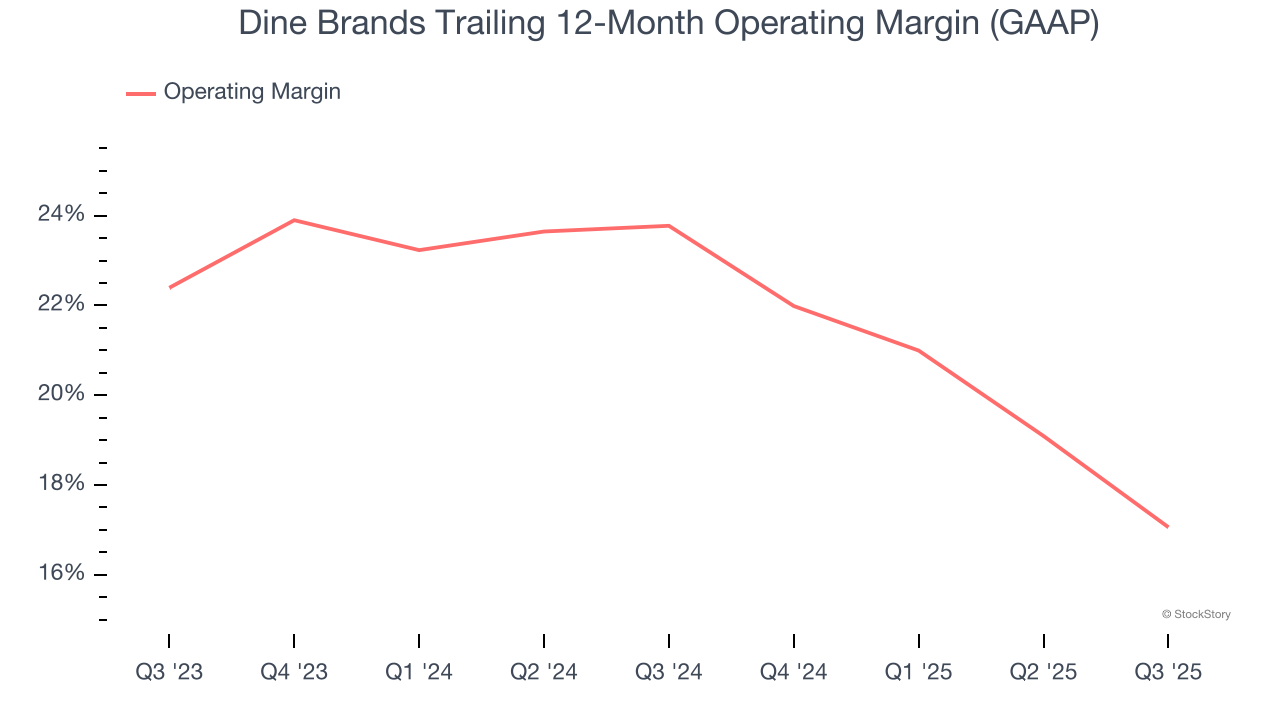

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, Dine Brands’s operating margin decreased by 6.7 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Dine Brands become more profitable in the future. Its operating margin for the trailing 12 months was 17.1%.

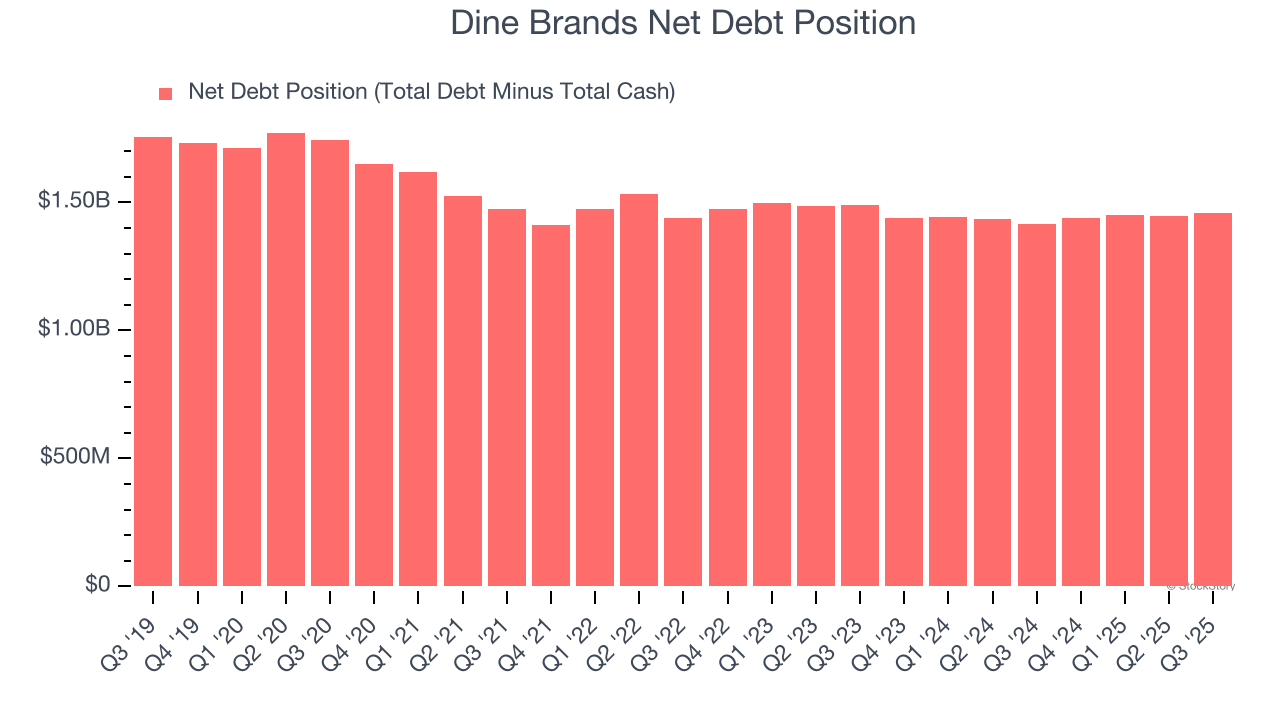

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Dine Brands’s $1.63 billion of debt exceeds the $168 million of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $210 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Dine Brands could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Dine Brands can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

We see the value of companies helping consumers, but in the case of Dine Brands, we’re out. With its shares outperforming the market lately, the stock trades at 7.4× forward P/E (or $33.86 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-15 | |

| Jul-13 | |

| Jul-13 | |

| Jul-07 | |

| Jun-24 | |

| Jun-22 | |

| May-19 | |

| May-18 | |

| May-14 | |

| May-11 | |

| May-11 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite