|

|

|

|

|||||

|

|

|

Opendoor Technologies Inc. OPEN is rewriting its iBuying strategy after a prolonged period of extreme caution that prioritized risk control over transaction volume. The third-quarter 2025 earnings call marked a clear pivot; management is moving away from wide spreads and defensive buying toward a higher-velocity, market-maker style model focused on flow, speed and tighter margins.

Under new leadership, the company openly acknowledged that excessive risk aversion damaged the business. Home acquisitions in third-quarter 2025 fell to just 1,169 units, leaving the company with older, less attractive inventory and weaker margins. While revenues of $915 million exceeded guidance, profitability suffered as legacy homes selected under the prior strategy weighed on results. Management’s takeaway was direct, when volume collapses, pricing discipline alone cannot protect returns.

The new playbook emphasizes buying and selling more homes quickly, supported by aggressive use of AI in pricing, inspections and operations. Opendoor has already doubled its weekly acquisition pace in recent months by lowering spreads on high-quality homes while tightening selection standards. This approach aims to reduce days in possession, lower holding costs and rebuild a healthier inventory mix.

Crucially, cost discipline remains intact. Operating expenses are structurally lower than last year, giving Opendoor room to scale volumes without a proportional rise in fixed costs. The company is also layering in ancillary services such as mortgage and warranty products, which could lift unit economics over time.

The shift is not without risk, higher volumes expose OPEN to market volatility. Still, treating iBuying as a liquidity business rather than a directional bet appears more aligned with the model’s strengths. If execution holds, Opendoor’s renewed focus on velocity may prove to be the right iBuying strategy after all.

Opendoor’s pivot toward higher transaction volume and tighter spreads places it in sharper contrast with other players that have either exited or narrowed their iBuying ambitions.

Zillow Group ZG, once Opendoor’s most formidable competitor, famously shut down Zillow Offers after concluding that home price forecasting at scale introduced unacceptable risk. Zillow has since repositioned itself as a marketplace and advertising platform, prioritizing capital-light returns over inventory exposure. In that sense, OPEN is now deliberately pursuing the path Zillow stepped away from, but with a stronger emphasis on AI-driven pricing and faster inventory turns to reduce balance-sheet risk.

Offerpad Solutions OPAD represents another point of comparison. Like Opendoor, Offerpad continues to operate an iBuying model, but at a smaller scale and with more limited liquidity. While Offerpad has focused on cost control and selective buying, Opendoor’s renewed push for volume aims to create a market-making flywheel that smaller competitors may struggle to replicate.

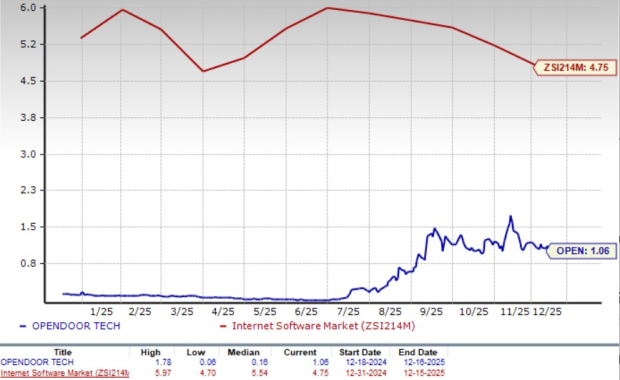

Shares of Opendoor have skyrocketed 289% in the past year compared with the industry’s growth of 5.1%.

From a valuation standpoint, OPEN trades at a forward price-to-sales (P/S) multiple of 1.06, significantly below the industry’s average of 4.75.

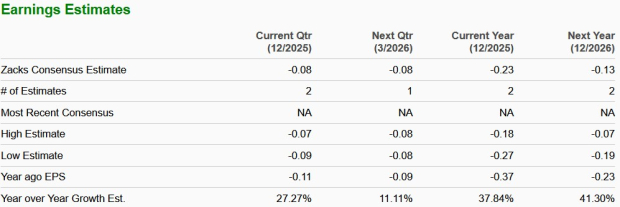

The Zacks Consensus Estimate for OPEN’s 2026 earnings implies a year-over-year uptick of 41.3%. Earnings per share estimates for 2026 have increased in the past 60 days.

OPEN stock currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours |

Mortgage and refinance interest rates today, Tuesday, July 21, 2026: Inching lower

ZG

Yahoo Personal Finance

|

| Jul-20 | |

| Jul-19 | |

| Jul-18 | |

| Jul-17 |

Mortgage and refinance interest rates today, Friday, July 17, 2026: Rates are mixed today

ZG

Yahoo Personal Finance

|

| Jul-16 |

Mortgage and refinance interest rates today, Thursday, July 16, 2026: Rates on the rise

ZG

Yahoo Personal Finance

|

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 |

Mortgage & refinance interest rates today, Tuesday, July 14, 2026: Rates mixed this morning

ZG

Yahoo Personal Finance

|

| Jul-14 |

Mortgage & refinance rates today, Tuesday, July 14, 2026: Rates mixed this morning

ZG

Yahoo Personal Finance

|

| Jul-13 | |

| Jul-12 |

Mortgage and refinance interest rates today, Sunday, July 12, 2026: Mostly down from last week

ZG

Yahoo Personal Finance

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite