|

|

|

|

|||||

|

|

|

Boot Barn currently trades at $195.13 and has been a dream stock for shareholders. It’s returned 377% since December 2020, blowing past the S&P 500’s 83.9% gain. The company has also beaten the index over the past six months as its stock price is up 19.5% thanks to its solid quarterly results.

Is there a buying opportunity in Boot Barn, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Despite the momentum, we're cautious about Boot Barn. Here are three reasons there are better opportunities than BOOT and a stock we'd rather own.

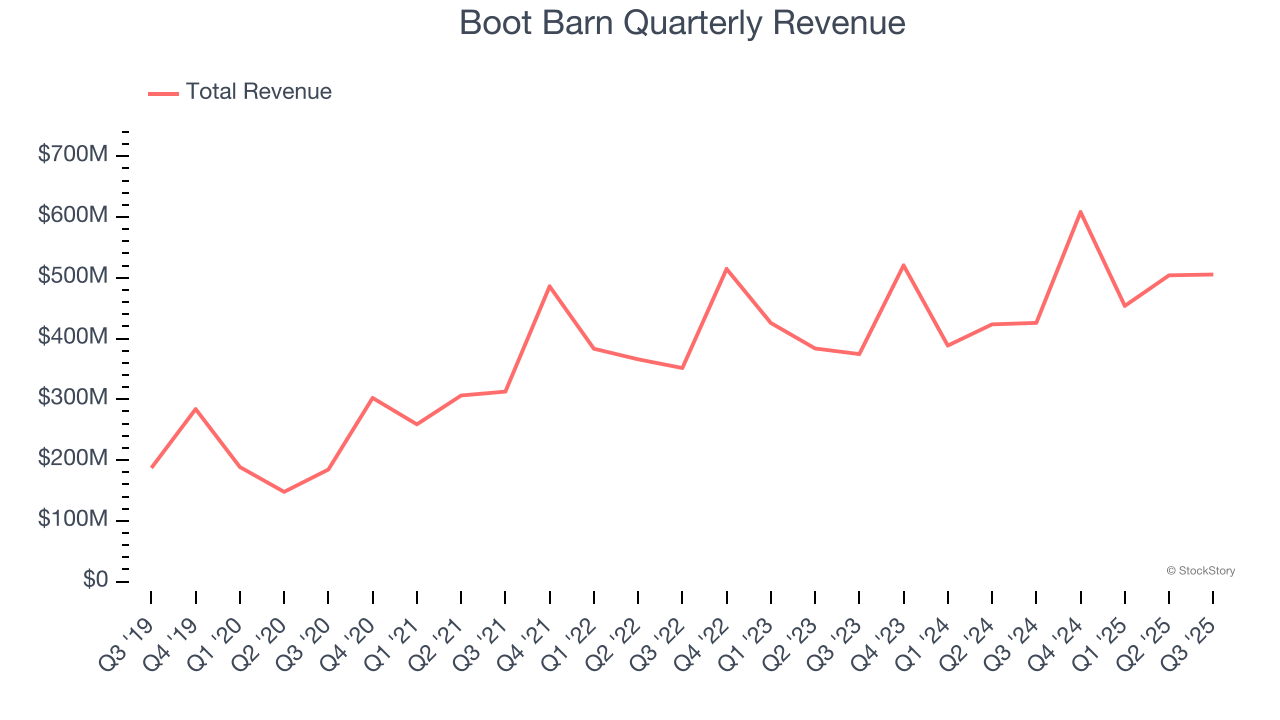

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Boot Barn’s sales grew at a mediocre 9.3% compounded annual growth rate over the last three years. This was below our standard for the consumer retail sector.

With $2.07 billion in revenue over the past 12 months, Boot Barn is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

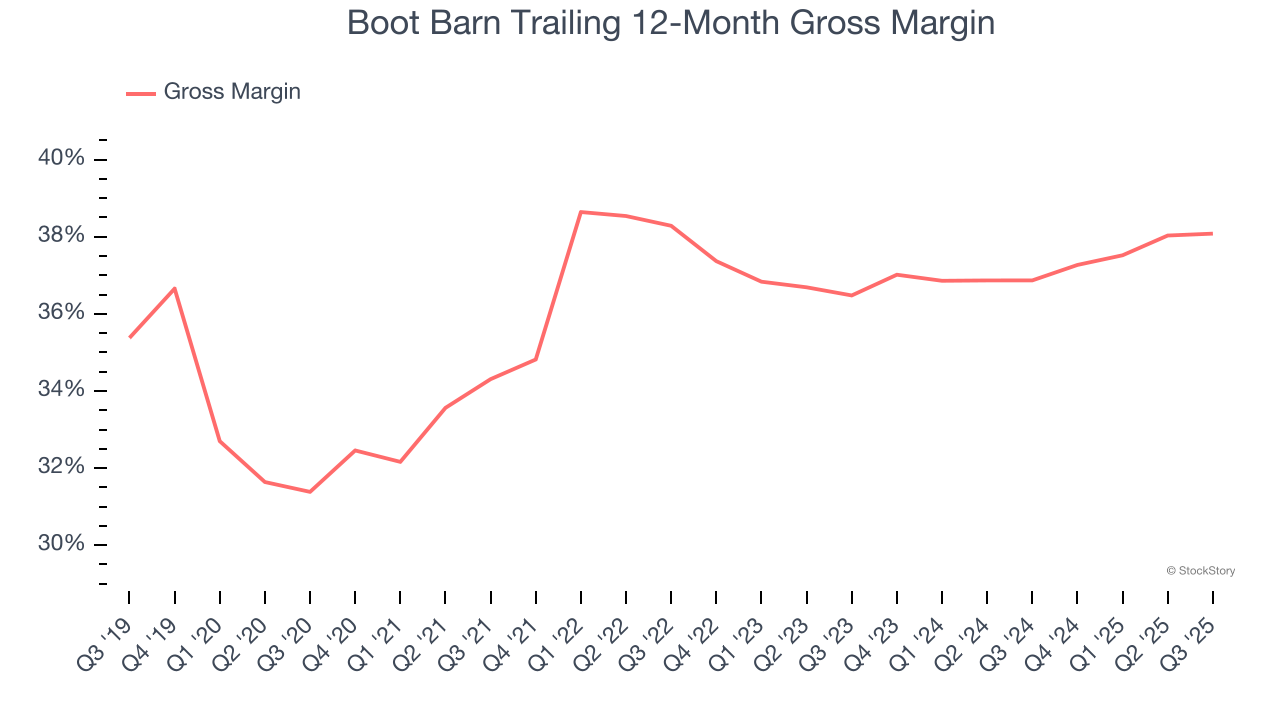

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Boot Barn has bad unit economics for a retailer, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 37.5% gross margin over the last two years. That means Boot Barn paid its suppliers a lot of money ($62.48 for every $100 in revenue) to run its business.

Boot Barn’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 27.9× forward P/E (or $195.13 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Mar-27 | |

| Mar-19 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite