|

|

|

|

|||||

|

|

|

Although Bank OZK (currently trading at $48.25 per share) has gained 7.4% over the last six months, it has trailed the S&P 500’s 13.6% return during that period. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Bank OZK, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

We're sitting this one out for now. Here are three reasons there are better opportunities than OZK and a stock we'd rather own.

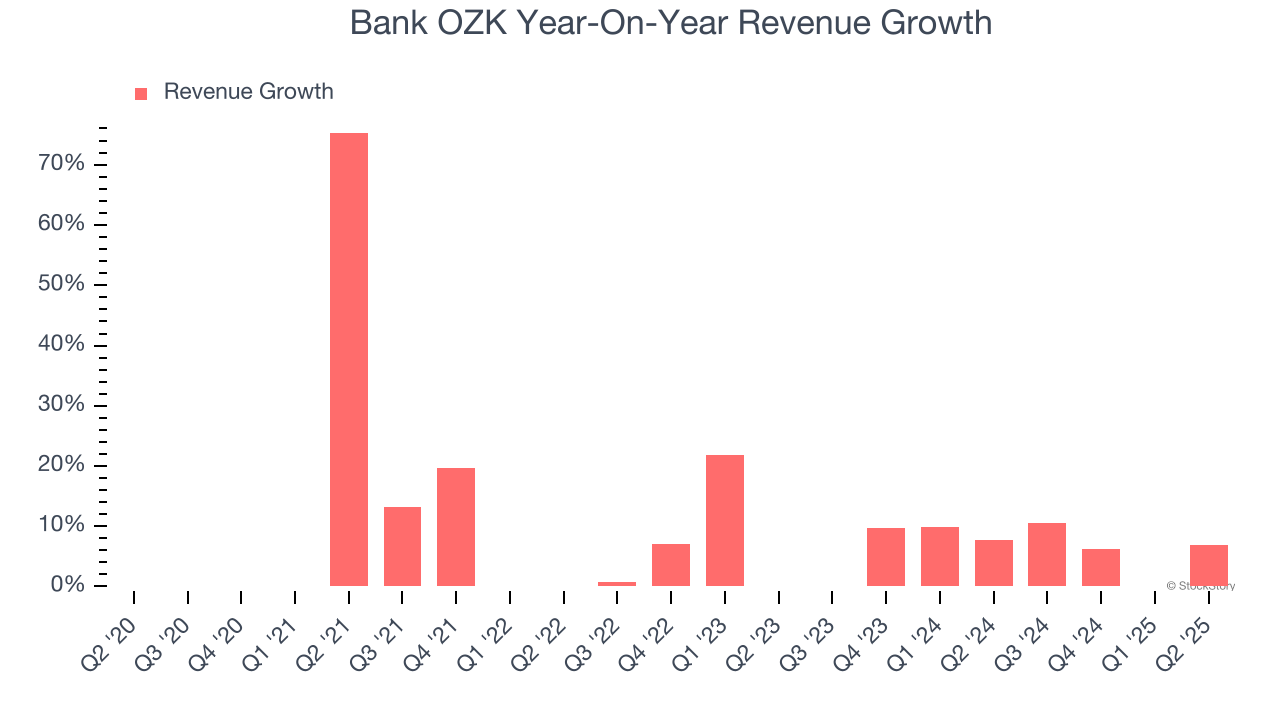

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. Bank OZK’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 9.1% over the last two years was well below its five-year trend.

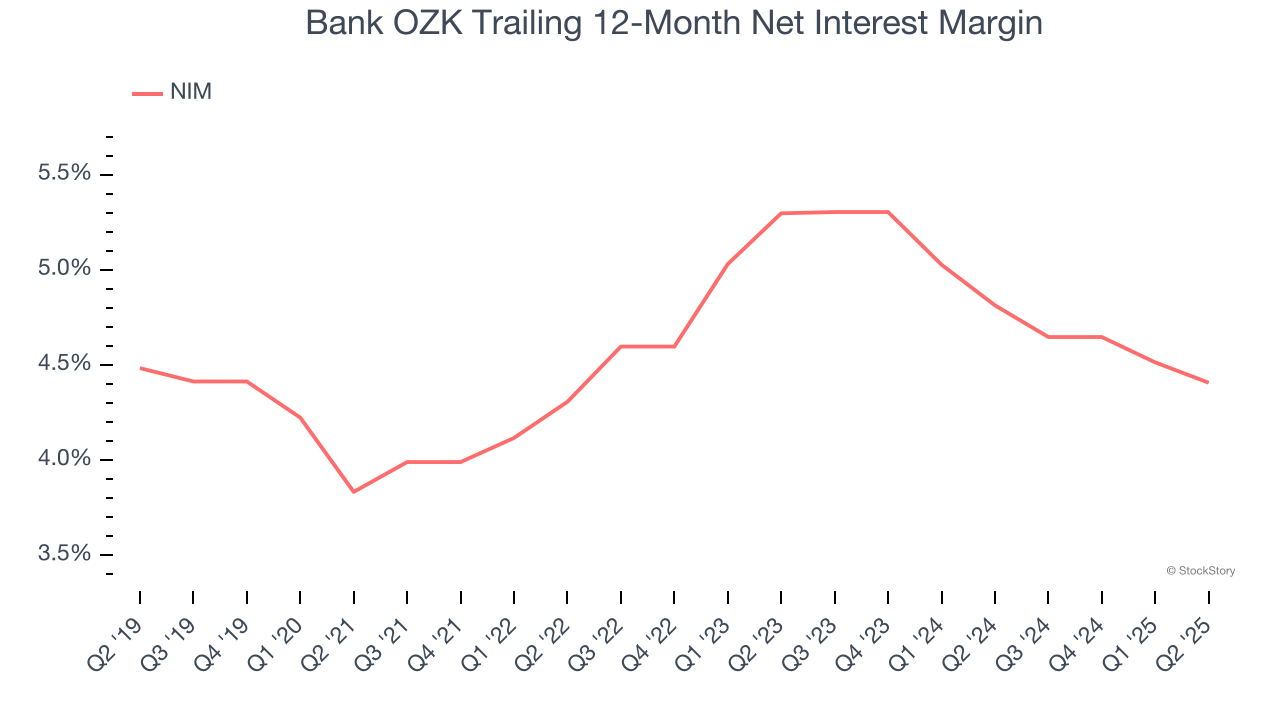

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, Bank OZK’s net interest margin averaged 4.6%. However, its margin contracted by 89 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Bank OZK either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

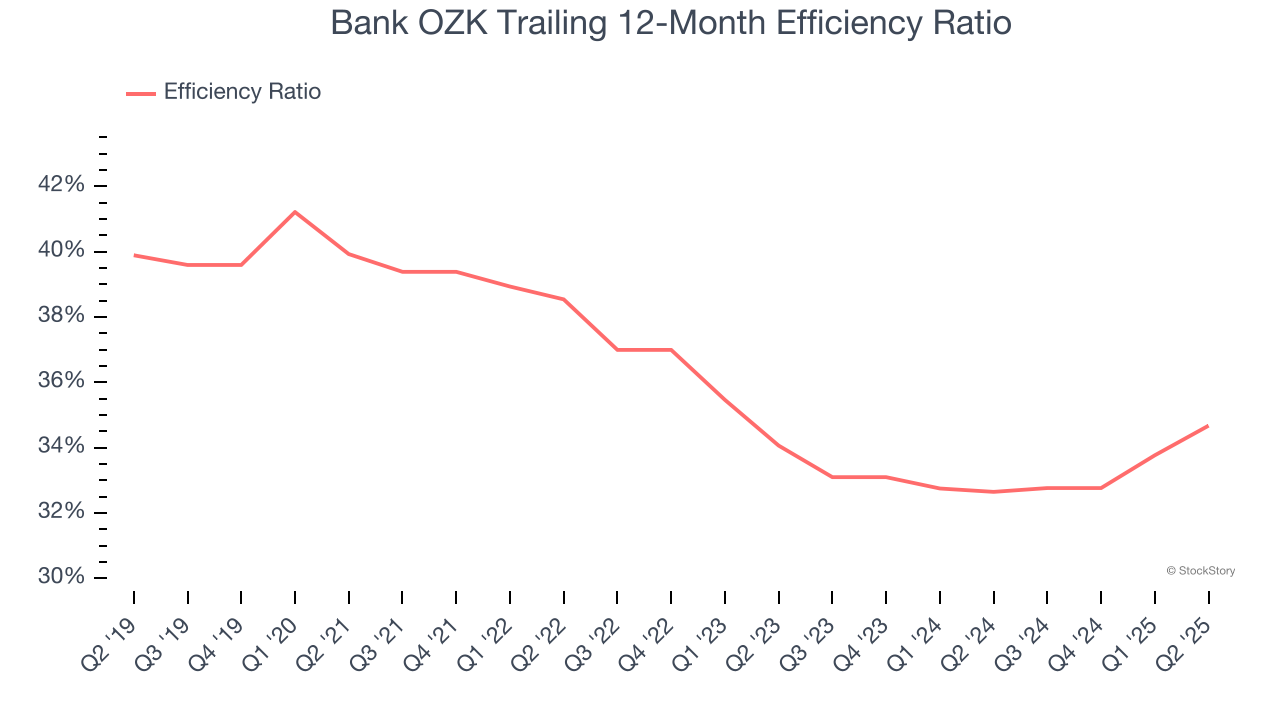

Topline growth alone doesn't tell the complete story - the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Markets emphasize efficiency ratio trends over static measurements, recognizing that revenue compositions drive different expense bases. Lower efficiency ratios signal superior performance by indicating that banks are controlling costs effectively relative to their income.

For the next 12 months, Wall Street expects Bank OZK to become less profitable as it anticipates an efficiency ratio of 37.6% compared to 34.7% over the past year.

Bank OZK isn’t a terrible business, but it isn’t one of our picks. With its shares trailing the market in recent months, the stock trades at 0.9× forward P/B (or $48.25 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better investments elsewhere. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-21 | |

| Jul-21 | |

| Jul-15 | |

| Jul-01 | |

| Jun-30 | |

| Jun-29 | |

| Apr-23 | |

| Apr-22 | |

| Apr-21 | |

| Apr-21 | |

| Apr-01 | |

| Mar-31 | |

| Mar-05 | |

| Mar-03 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite