|

|

|

|

|||||

|

|

|

Nebius Group N.V. NBIS has rapidly positioned itself as a major player in the AI cloud and infrastructure market, driven by unprecedented demand for GPU capacity and long-term contracts with large technology companies. On the third-quarter 2025 earnings call, management highlighted the signing of two transformative mega deals: a contract with Microsoft valued between $17.4 billion and $19.4 billion and a new agreement with Meta worth approximately $3 billion over the next five years.

The company emphasized that demand continues to outstrip supply, with all available capacity sold out each quarter. Management noted that every time new capacity is brought online, it is immediately absorbed by customers. These agreements provide long-term visibility into revenue and utilization as Nebius accelerates its expansion toward 2.5 gigawatts of contracted power and up to 1 gigawatt of connected capacity by the end of 2026. The company expects these deals to be a key contributor to its ambition of reaching $7 billion to $9 billion in annualized run-rate revenue by the end of 2026, with more than half of this target already booked.

However, Nebius has tightened its full-year group revenue outlook to a range of $500 million to $550 million from the previous guidance of $450 million to $630 million. The company expects to land in the middle rather than the upper end, primarily relating to the timing of capacity coming online. Although the company expects adjusted EBITDA to turn slightly positive at the group level by year-end 2025, it will remain negative for the full year.

The company is grappling with macroeconomic uncertainties, rising expenses and heavy capital spending. For 2025, Nebius has raised its capital expenditure guidance from approximately $2 billion to around $5 billion. Elevated capital expenditure levels pose a risk if revenue growth fails to keep pace with the company’s capital intensity, particularly in an environment where AI demand may fluctuate amid competitive pricing pressures and evolving regulatory frameworks.

Moreover, the scale of the Microsoft and Meta contracts inevitably raises customer concentration risk. A substantial portion of future revenue growth is expected from these two customers beginning in 2026, with Microsoft reaching full annual run-rate contribution from 2027 and Meta largely at full run rate in 2026. This reliance means that performance, timing of deployments and ongoing demand from a small number of very large customers could have an outsized impact on Nebius’ financial results. While these mega deals provide stability, financing advantages and rapid scale, they also heighten exposure to concentration, making continued diversification across start-ups, enterprises and other large customers critical to balancing growth with risk.

CoreWeave, Inc.’s CRWV revenue backlog expanded sharply to $55.6 billion in the third quarter, up 271% year over year and nearly doubling sequentially. The growth was fueled by large, long-term agreements with major customers like OpenAI, Meta and other hyperscalers, highlighting robust demand for AI-centric cloud infrastructure. The company’s momentum was also supported by multi-billion-dollar partnerships with NVIDIA, including industry-first rollouts of GB300 NVL72 systems and RTX PRO 6000 Blackwell Server Edition instances, giving CRWV an early advantage in frontier AI and real-time workloads. Moreover, the company is expanding through acquisitions, adding Marimo in October after earlier deals such as OpenPipe and Weights & Biases.

Alphabet Inc.’s GOOGL investments in infrastructure, security, data management, analytics and AI are growing. Its strategic partnerships and acquisitions, and increasing number of data centers are helping Google to expand its cloud footprint worldwide. Alphabet is benefiting from its partnership with NVIDIA in the cloud. Google Cloud was the first cloud provider to offer NVIDIA’s B200 and GB200 Blackwell GPUs and will be offering its next-generation Vera Rubin GPUs. Introduction of 2.5 flash, Imagen 3 and Veo 2 are noteworthy developments. Recently, Alphabet’s Google Cloud and NextEra Energy announced an expanded partnership to develop multiple new gigawatt-scale data center campuses with accompanying generation and capacity.

Shares of Nebius have gained 212.3% in the past year compared with the Internet – Software and Services industry’s growth of 30.7%.

Valuation-wise, Nebius seems overvalued, as suggested by the Value Score of F. In terms of Price/Book, NBIS shares are trading at 4.68X, higher than the Internet Software Services industry’s 3.83X.

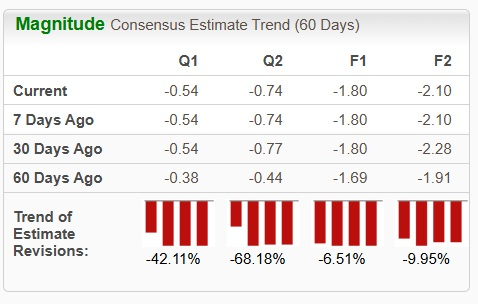

The Zacks Consensus Estimate for NBIS’ 2025 earnings has seen a downward revision over the past 60 days.

NBIS currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 42 min | |

| 1 hour | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 9 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite