|

|

|

|

|||||

|

|

|

Zacks Rank #5 (Strong Sell) stock Acadia Healthcare Company, Inc. (ACHC) is a behavioral healthcare provider. Headquartered in Franklin, TN, Acadia Healthcare owns and operates a vast network of 262 facilities across 39 states and Puerto Rico, making it one of the largest standalone behavioral health companies in the U.S. ACHC’s healthcare facilities have ~12,000 beds with 163 comprehensive treatment centers (CTCs). Among the CTCs, 21 are owned properties of Acadia Healthcare, and 142 are leased properties.

A bombshell 2024 New York Times (NYT) article suggested that Acadia forced patients to stay in their facilities against their will to increase profits from insurance payments. The article resulted in numerous subpoenas from the U.S. Department of Justice (DOJ) and the SEC regarding its admissions, length of stay, and billing practices. As a result, Acadia has agreed to pay massive settlements to attempt to clear its legal woes, including a $17 million settlement for a Medicaid fraud scheme in West Virginia.

In addition to rising legal costs, ACHC continues to face rising costs from higher wages, benefits, and supply prices. Total expenses surged 15% year over year. Meanwhile, ongoing DOJ scrutiny and heightened media attention are likely to keep these expenses elevated, pressuring margins.

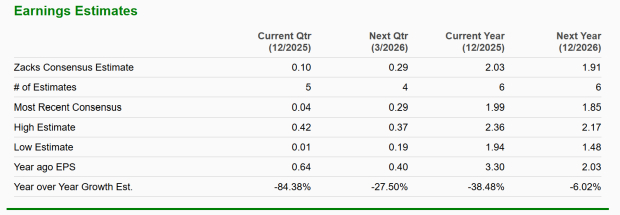

ACHC is facing negative growth prospects over the next few quarters. For the current quarter, Zacks Consensus Estimates suggest EPS growth will plunge 84.38% year-over-year. Meanwhile, the negative EPS growth is expected to continue into next year.

Additionally, the company’s reduced 2025 guidance reflects continued financial strain. ACHC management now expects adjusted EPS between $2.35 and $2.45, down from $2.45-$2.65 previously. Adjusted EBITDA is forecast at $650–$660 million, lower than the prior $675–$700 million range. Operating cash flow guidance was lowered to $400 to $425 million. The downgrades highlight cost pressures and slower recovery momentum across operations. Management still plans capital expenditures of $505–$515 million for 2025, suggesting limited flexibility despite moderated earnings expectations. With softer guidance and rising expenses, near-term growth prospects remain constrained.

ACHC shares are -64.53% year-to-date, dramatically underperforming the major market indices and exhibiting troubling relative weakness. Meanwhile, shares are well below their 200-day moving average. As Paul Tudor Jones warns, “Nothing good happens below the 200-day moving average.”

Bottom Line

Overall, Acadia Healthcare faces a difficult near-term outlook as legal and regulatory overhangs, rising cost pressures, and sharply weakening earnings momentum weigh on operations. With guidance moving lower, margins under stress, and the stock showing pronounced technical weakness, ACHC remains challenged on both fundamental and market fronts.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-09 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-02 | |

| Aug-02 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite