|

|

|

|

|||||

|

|

|

General Motors GM and Ford F have long been fierce rivals in the American auto industry—but which stock looks like the better investment now? Both automakers have been resilient and weathered multiple economic cycles. Both possess ample liquidity and are navigating toward electric and software-defined vehicles.

So far this year, GM stock is up 56%, handily outperforming Ford’s 36% gain. With momentum building and 2026 approaching, let’s take a closer look at their fundamentals, growth drivers, and key risks to determine which stock investors should bet on next.

GM remains the top-selling automaker in the United States, holding around 17% market share. Demand across core brands—Chevrolet, Buick, GMC, and Cadillac—continues to drive sales, led by pickups and SUVs. Upcoming launches, including the next-generation Cadillac CT5, a redesigned XT5, and the relaunch of the Orion Assembly plant in early 2027 to produce the Cadillac Escalade and new full-size pickups, reinforce GM’s focus on meeting domestic demand.

China, previously a major drag, is showing signs of recovery. GM has streamlined its product lineup, shifted focus to profitable models, and reduced exposure to weaker segments. These changes resulted in third-quarter 2025 vehicle sales in China to rise 10% year over year, marking the second consecutive quarter of growth.

GM is also gaining momentum in software and services, which are becoming meaningful growth drivers. Year to date, the company has recognized about $2 billion in revenues from Super Cruise, OnStar and other software offerings. Deferred software revenues climbed more than 90% year over year to $5 billion by the end of the third quarter, highlighting GM’s progress toward software-defined vehicles and advanced driver-assistance technology.

Another underlying catalyst is GM’s strategic role in the U.S. push to secure domestic battery materials. The company is a joint venture partner in Lithium Americas’ Thacker Pass project in Nevada and is expected to become one of North America’s largest lithium sources.

Finally, General Motors has remained highly shareholder-friendly. It repurchased more than $3.5 billion of stock through the third quarter, reducing its share count by 15% year over year, with $2.8 billion still available under its buyback authorization.

For GM, the Zacks Consensus Estimate points to a modest 0.3% sales decline in 2026 and a 13% increase in EPS.

General Motors Company price-consensus-eps-surprise-chart | General Motors Company Quote

Ford is adjusting its strategy amid slower EV adoption, shifting U.S. regulations under the Trump administration and rising costs. Instead of pushing aggressively into large, capital-intensive EVs, the company is leaning more on hybrids, gas-powered vehicles, and smaller, more affordable electric models.

At the center of this reset is Ford’s new Universal EV Platform, designed to lower costs and improve flexibility. The first vehicle on this platform will be a midsize electric pickup, scheduled for production at the Louisville Assembly Plant starting in 2027. In parallel, Ford is launching a battery energy storage systems business, leveraging its wholly owned plants in Kentucky and Michigan and using lithium iron phosphate (LFP) technology. These moves are aimed at improving margins across Ford Blue, Ford Pro and Ford Model e.

Ford expects the biggest turnaround in its EV unit. While Model e continues to weigh on profitability, the company now expects the segment to reach breakeven by 2029, with meaningful improvements beginning in 2026. However, this transition comes at a cost. Ford expects to record roughly $19.5 billion in special items (mostly in the fourth-quarter 2025), largely tied to rationalizing its U.S. EV assets and product roadmap. About $5.5 billion of this is expected to impact cash flow, primarily in 2026 and 2027.

One bright spot for the company is Ford Pro, which continues to deliver solid momentum. Strong demand for Super Duty trucks, healthy order books, and growing software and service revenues are reinforcing Ford Pro’s role as a key growth engine. Additionally, Ford maintains a strong liquidity position, and its dividend yield of more than 4% remains attractive for income-focused investors.

The Zacks Consensus Estimate suggests Ford’s 2026 sales will decline about 3% year over year, while earnings are expected to jump roughly 35%.

Ford Motor Company price-consensus-eps-surprise-chart | Ford Motor Company Quote

General Motors stands out as the more compelling investment heading into 2026. The company expects 2026 to be a stronger year than 2025 as it sharpens its focus on long-term profitability. The company is actively narrowing EV-related losses, reducing warranty expenses, offsetting tariff pressure, streamlining regulatory compliance, and maintaining tight control over fixed costs. These initiatives, combined with strong momentum in software, improved performance in China, and consistent share buybacks, provide greater earnings visibility and downside protection.

Ford, meanwhile, is making sensible strategic adjustments by prioritizing hybrids, commercial vehicles and capital discipline. However, the sizable one-time charges tied to its EV reset and the delayed profitability timeline for Model e weigh on the near-term investment case. While Ford Pro remains a bright spot and the dividend is attractive, execution risks remain elevated.

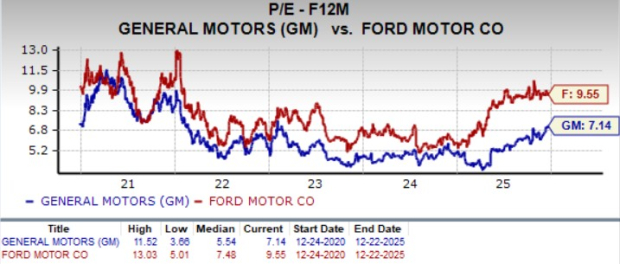

Valuation further tilts the balance in GM’s favor. General Motors trades at a forward earnings multiple of 7.14x, notably cheaper than Ford’s 9.55x.

Taken together, GM’s operational execution and more attractive valuation make it the better stock to buy heading into 2026. General Motors sports a Zacks Rank #1 (Strong Buy), while Ford carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 27 min | |

| 37 min |

Trump imposes 50% tariffs on Canada: Markets are accustomed to 'heavy hand' tactic

GM

Yahoo Finance Video

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite