|

|

|

|

|||||

|

|

|

What a time it’s been for Opendoor. In the past six months alone, the company’s stock price has increased by a massive 1,124%, reaching $6.49 per share. This performance may have investors wondering how to approach the situation.

Is now the time to buy Opendoor, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Despite the momentum, we're swiping left on Opendoor for now. Here are three reasons we avoid OPEN and a stock we'd rather own.

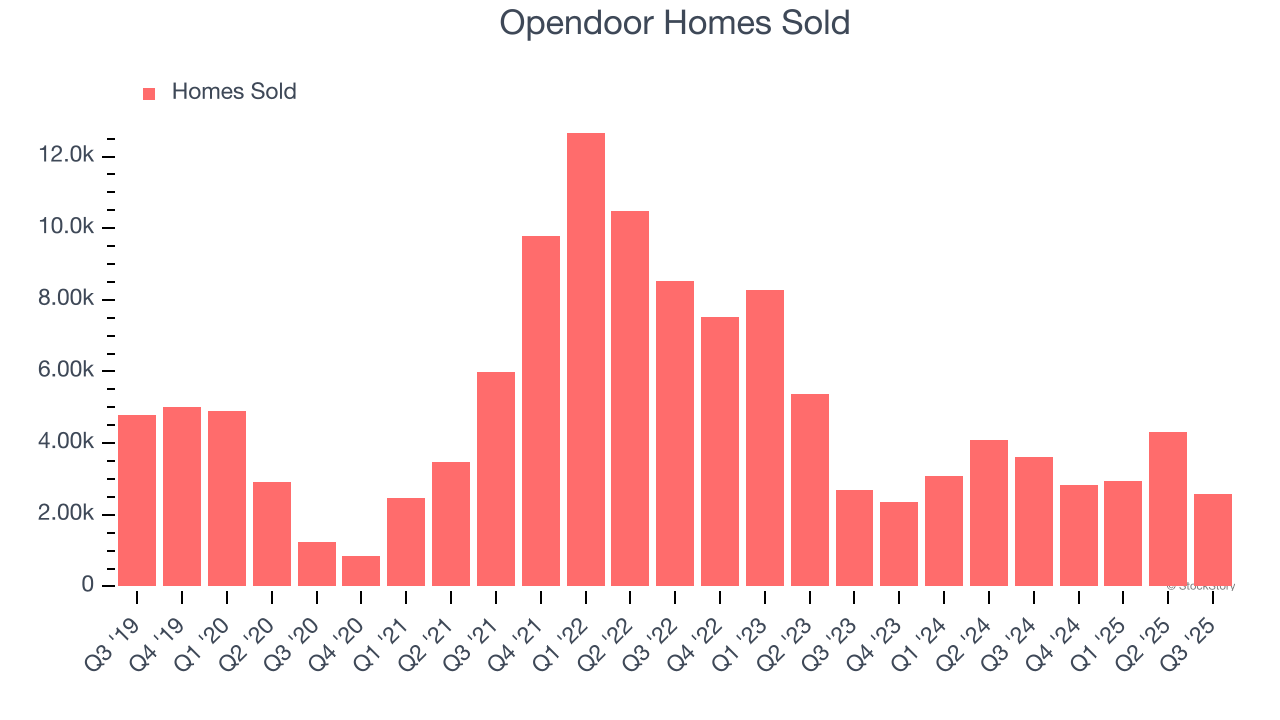

Revenue growth can be broken down into changes in price and volume (for companies like Opendoor, our preferred volume metric is homes sold). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Opendoor’s homes sold came in at 2,568 in the latest quarter, and over the last two years, averaged 16.2% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Opendoor might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Opendoor will flip from cash-producing to cash-burning. Their consensus estimates imply its free cash flow margin of 18.8% for the last 12 months will decrease to negative 3.6%.

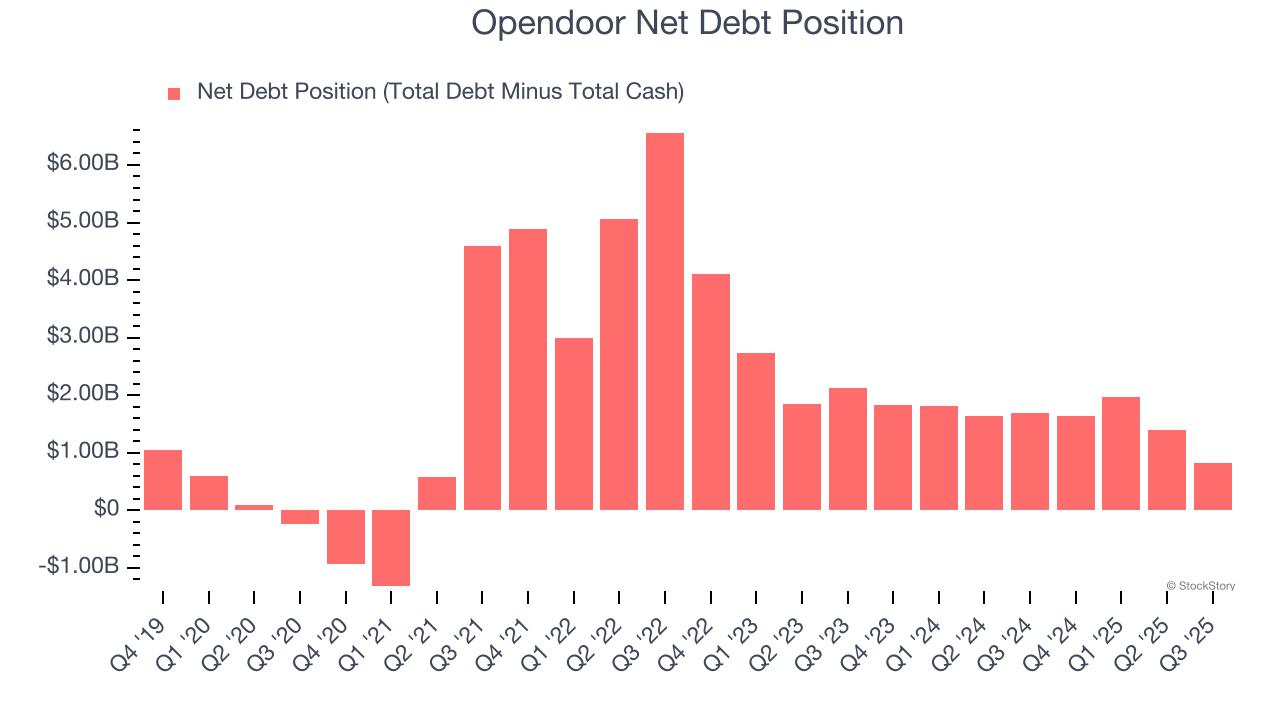

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Opendoor posted negative $89 million of EBITDA over the last 12 months, and its $1.79 billion of debt exceeds the $962 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Opendoor if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Opendoor can improve its profitability and remain cautious until then.

We cheer for all companies serving everyday consumers, but in the case of Opendoor, we’ll be cheering from the sidelines. After the recent surge, the stock trades at $6.49 per share (or a forward price-to-sales ratio of 1.1×). The market typically values companies like Opendoor based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. Let us point you toward the most entrenched endpoint security platform on the market.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Mar-12 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-04 | |

| Mar-04 | |

| Mar-03 | |

| Mar-03 | |

| Mar-03 | |

| Mar-02 | |

| Mar-02 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite