|

|

|

|

|||||

|

|

|

Assurant’s 20.9% return over the past six months has outpaced the S&P 500 by 7.5%, and its stock price has climbed to $241.51 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Assurant, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We’re glad investors have benefited from the price increase, but we're swiping left on Assurant for now. Here are three reasons we avoid AIZ and a stock we'd rather own.

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services.

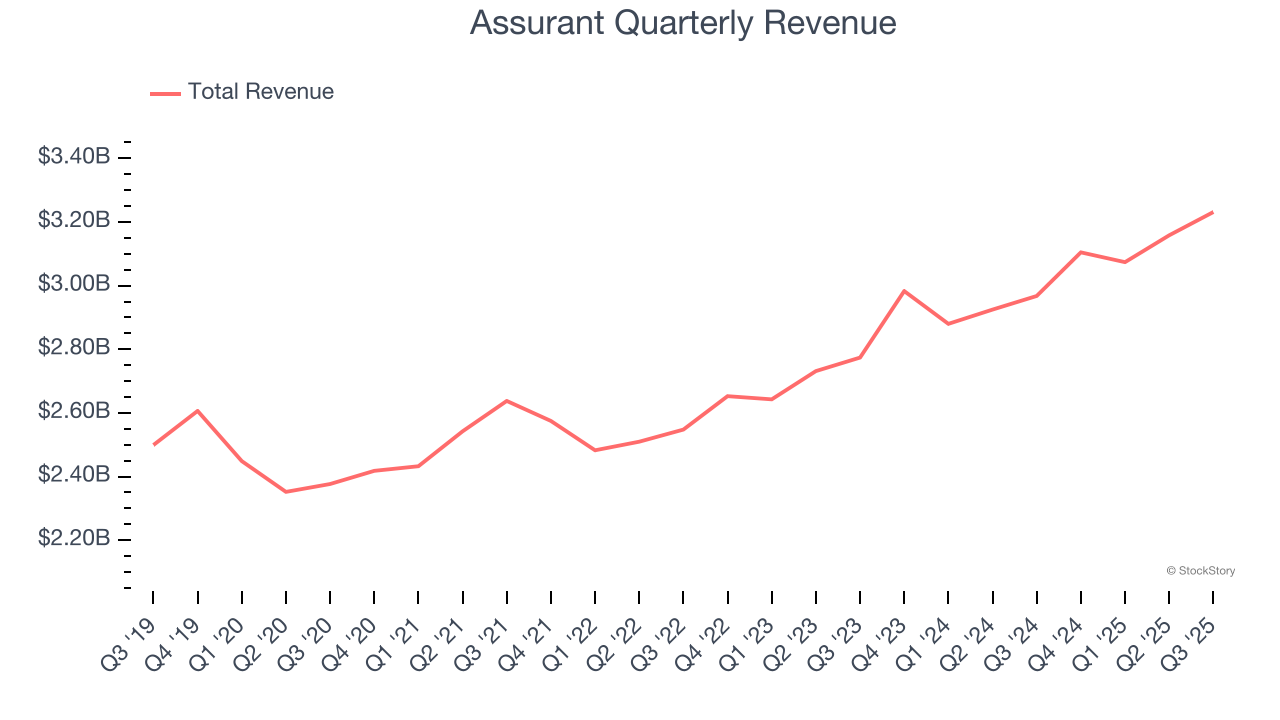

Over the last five years, Assurant grew its revenue at a tepid 5.1% compounded annual growth rate. This fell short of our benchmark for the insurance sector.

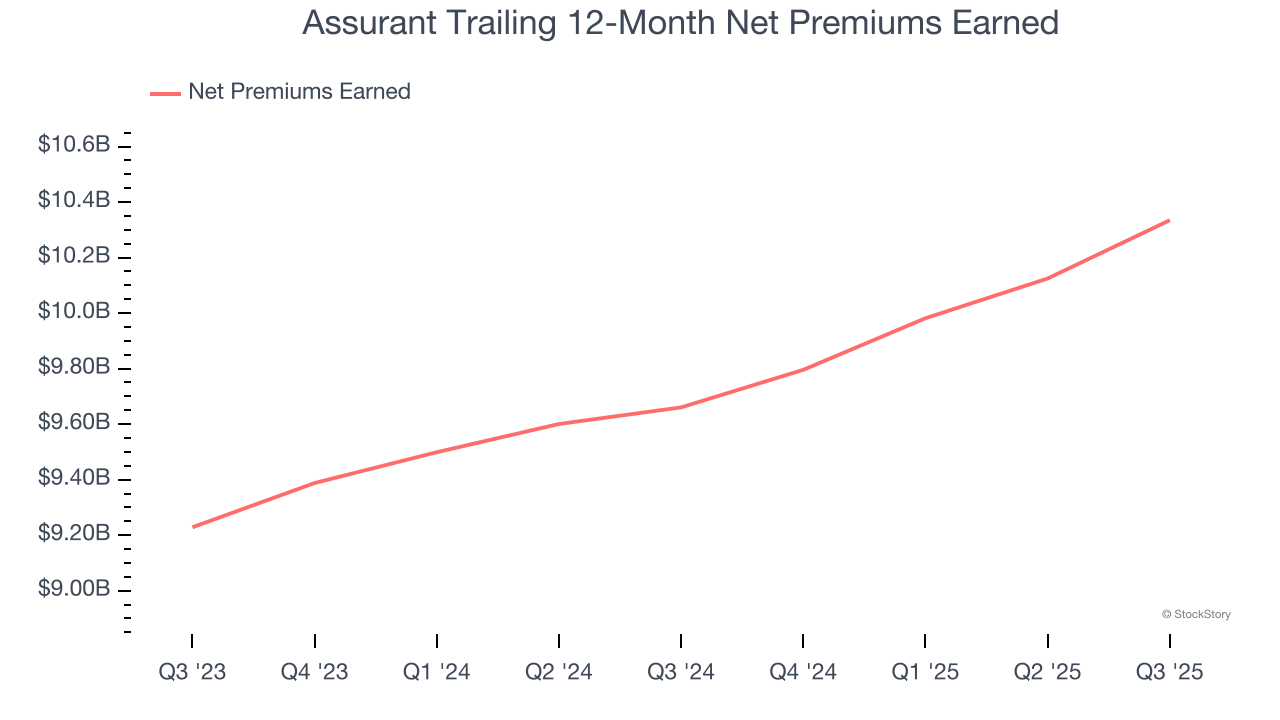

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

Assurant’s net premiums earned has grown at a 4.6% annualized rate over the last five years, worse than the broader insurance industry and in line with its total revenue.

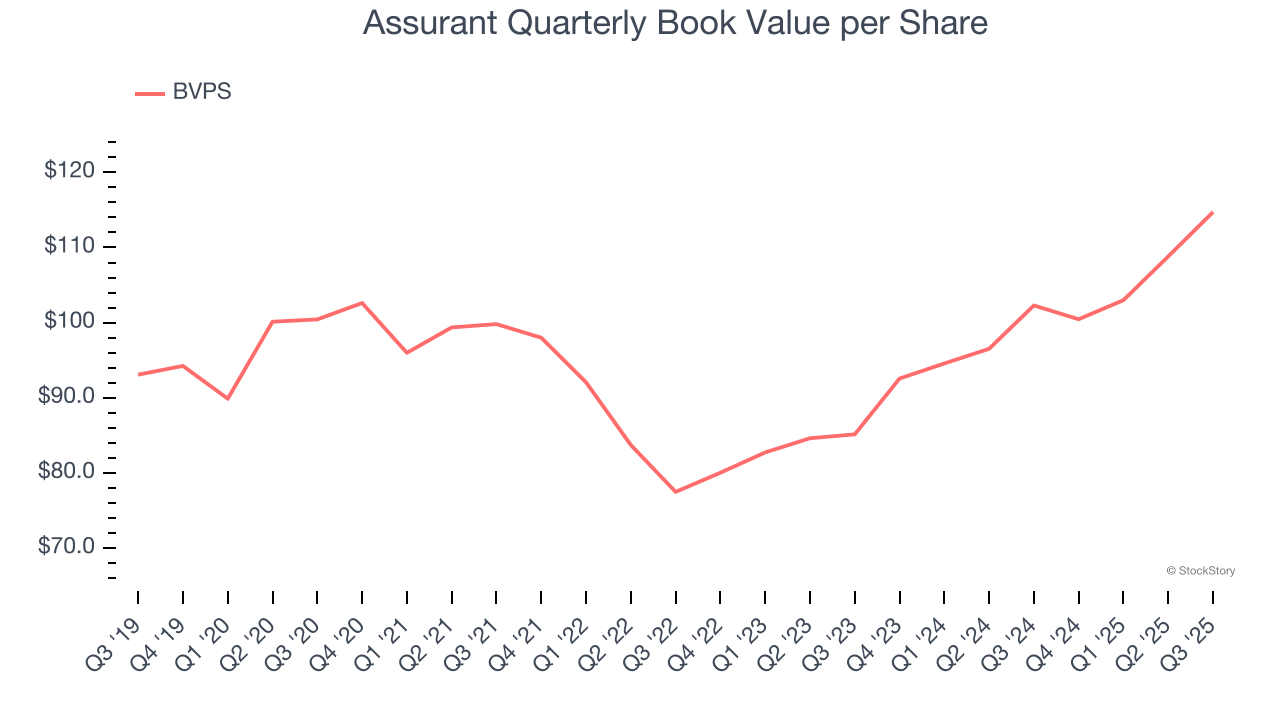

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

Although Assurant’s BVPS increased by a meager 2.7% annually over the last five years, the good news is that its growth has recently accelerated as BVPS grew at a solid 16.1% annual clip over the past two years (from $85.15 to $114.72 per share).

Assurant’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 2.1× forward P/B (or $241.51 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of our top software and edge computing picks.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Jul-30 | |

| Jul-23 | |

| Jul-23 | |

| Jul-06 | |

| Jun-30 | |

| Jun-09 | |

| Jun-03 | |

| May-21 | |

| May-14 | |

| May-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite