|

|

|

|

|||||

|

|

|

What a brutal six months it’s been for Zscaler. The stock has dropped 26.5% and now trades at $229.31, rattling many shareholders. This may have investors wondering how to approach the situation.

Following the drawdown, is now a good time to buy ZS? Find out in our full research report, it’s free for active Edge members.

Pioneering the "zero trust" approach that has fundamentally changed enterprise network security, Zscaler (NASDAQ:ZS) provides a cloud-based security platform that connects users, devices, and applications securely without traditional network-based security hardware.

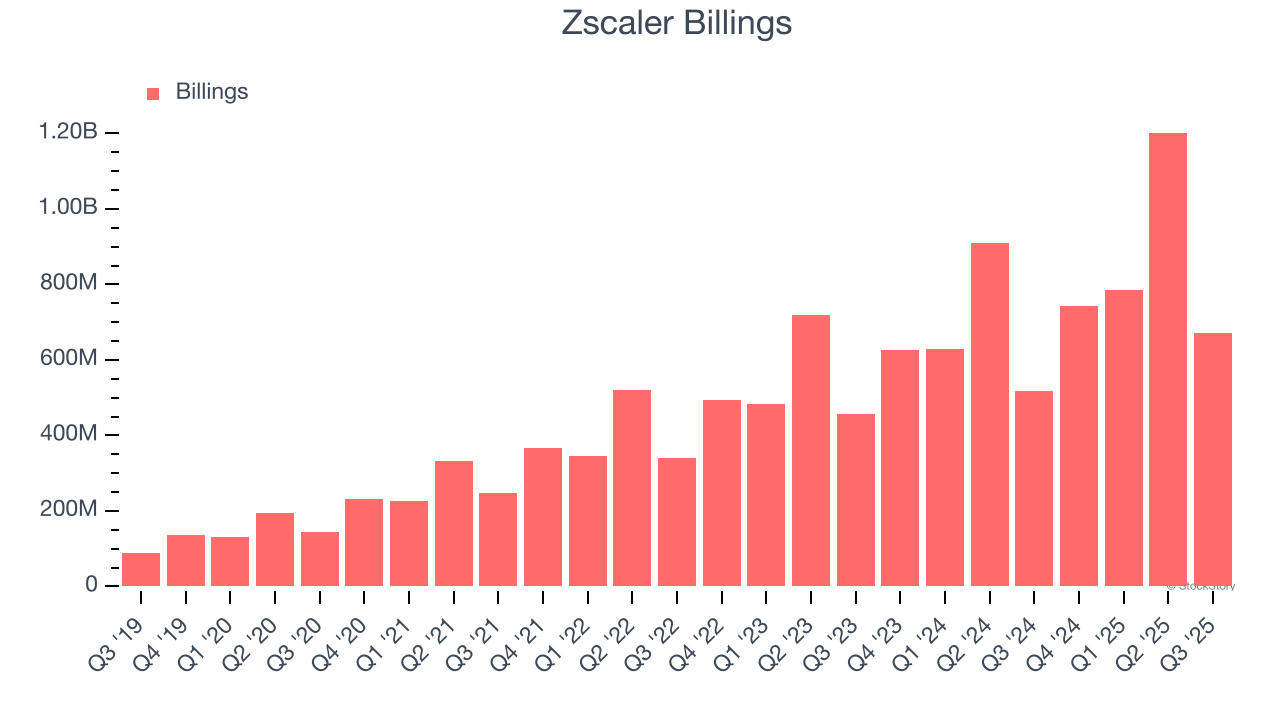

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zscaler’s billings punched in at $671.4 million in Q3, and over the last four quarters, its year-on-year growth averaged 26.3%. This performance was fantastic, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Zscaler’s revenue to rise by 21.6%. While this projection is below its 26.9% annualized growth rate for the past two years, it is commendable and suggests the market is baking in success for its products and services.

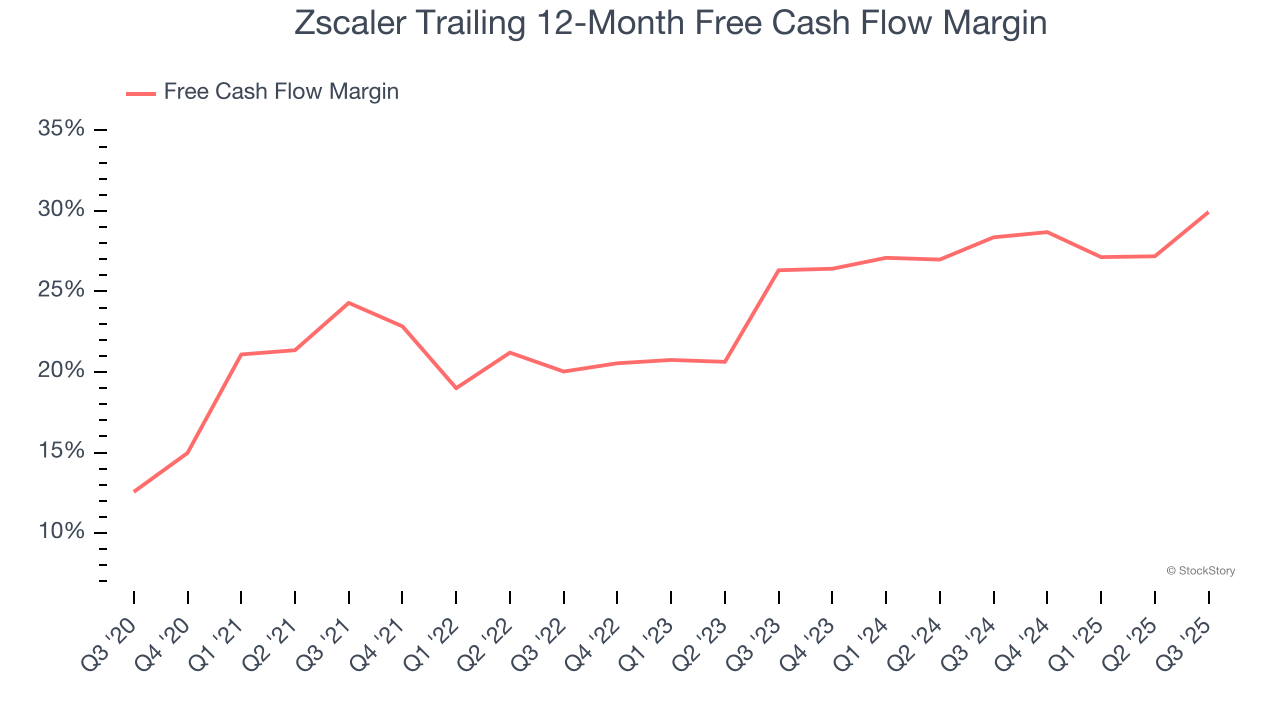

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Zscaler has shown robust cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that enable it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 29.9% over the last year, quite impressive for a software business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

These are just a few reasons why Zscaler ranks highly on our list. After the recent drawdown, the stock trades at 10.6× forward price-to-sales (or $229.31 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| 7 hours | |

| Mar-12 | |

| Mar-09 | |

| Mar-09 | |

| Mar-07 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-03 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite