|

|

|

|

|||||

|

|

|

Alibaba BABA confronts persistent headwinds in its core e-commerce operations despite management's aggressive pivot toward artificial intelligence investments. The company reported 5% year-over-year revenue growth to RMB247.8 billion in its second quarter of fiscal 2026, but this modest expansion masks troubling deterioration in profitability metrics.

Non-GAAP earnings plunged 71% year over year to RMB4.36 per American Depositary Share, significantly underperforming analyst expectations by approximately 20%. Operating income plunged 85% from RMB35.2 billion to just RMB5.4 billion, reflecting the substantial margin compression from strategic investments.

The China commerce segment faces intensifying competitive pressure from PDD Holdings, ByteDance's Douyin and JD.com, forcing Alibaba into costly defensive strategies. While local e-commerce revenues expanded 16% during the fiscal second quarter, supported by government consumption stimulus measures, this growth required elevated marketing expenditure and aggressive subsidies through the company's "10-Billion Subsidy" program. Management emphasized optimization of quick commerce unit economics, achieving a 50% reduction in per-order losses since mid-2025, yet these improvements remain insufficient to offset broader margin degradation.

In December 2025, Alibaba announced expanded instant commerce infrastructure through its Cainiao logistics arm, planning new or expanded warehouses across 31 mainland Chinese cities by January 2026 to enable four-hour grocery deliveries. However, this infrastructure investment compounds capital expenditure concerns, with the company already reporting RMB21.8 billion negative free cash flow last quarter, driven by an 80% year-over-year increase in capital spending. The balance sheet deterioration raises questions about Alibaba's ability to sustain simultaneous investments in AI infrastructure, quick commerce logistics and margin-eroding subsidies while defending against relentless competitive encroachment in its traditional e-commerce stronghold.

Amazon AMZN has aggressively accelerated its quick commerce footprint throughout late 2025, establishing over 300 micro-fulfillment centers across India's major metropolitan areas. Amazon's "Amazon Now" service promises 10-minute deliveries across select areas in Bengaluru, Delhi and Mumbai, with daily orders growing 25% month over month since the September 2025 expansion. The e-commerce giant announced in December 2025 plans to open two new dark stores daily, targeting 300 total facilities by year-end, exclusively in its three operating cities. Amazon's infrastructure investments remain substantial yet focused, concentrating resources on high-density urban markets where Prime membership penetration provides customer acquisition advantages.

Meanwhile, JD.com JD surpassed 700 million annual active customers in October 2025, driven partly by its JD NOW instant retail platform. It delivered products in as fast as nine minutes from over 500,000 physical stores across 2,300 Chinese counties and cities. JD.com achieved sequential investment reduction in its food delivery business during the third quarter, demonstrating improved unit economics performance that contrasts sharply with Alibaba's mounting losses. JD.com's November 2025 Singles' Day performance showcased 40% year-over-year growth in shoppers and nearly 60% order volume increases, with 95% of retail orders fulfilled within 24 hours.

Both Amazon and JD.com face similar infrastructure cost pressure as Alibaba, yet appear better positioned to absorb expansion expenses, given stronger baseline profitability and more disciplined capital allocation strategies.

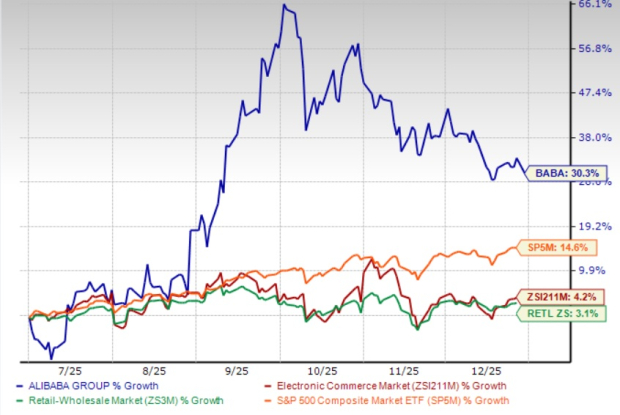

BABA shares have surged 30.3% in the past six-month period, outperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 4.2% and 3.1%, respectively.

From a valuation standpoint, BABA stock is currently trading at a forward 12-month price/sales ratio of 2.23X compared with the industry’s 2.14X. BABA has a Value Score of D.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $6.42 per share, implying a 28.7% year-over-year decline.

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Alibaba currently has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite