|

|

|

|

|||||

|

|

|

Target has been treading water for the past six months, recording a small loss of 0.6% while holding steady at $98.08. The stock also fell short of the S&P 500’s 11.7% gain during that period.

Is there a buying opportunity in Target, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

We're cautious about Target. Here are three reasons you should be careful with TGT and a stock we'd rather own.

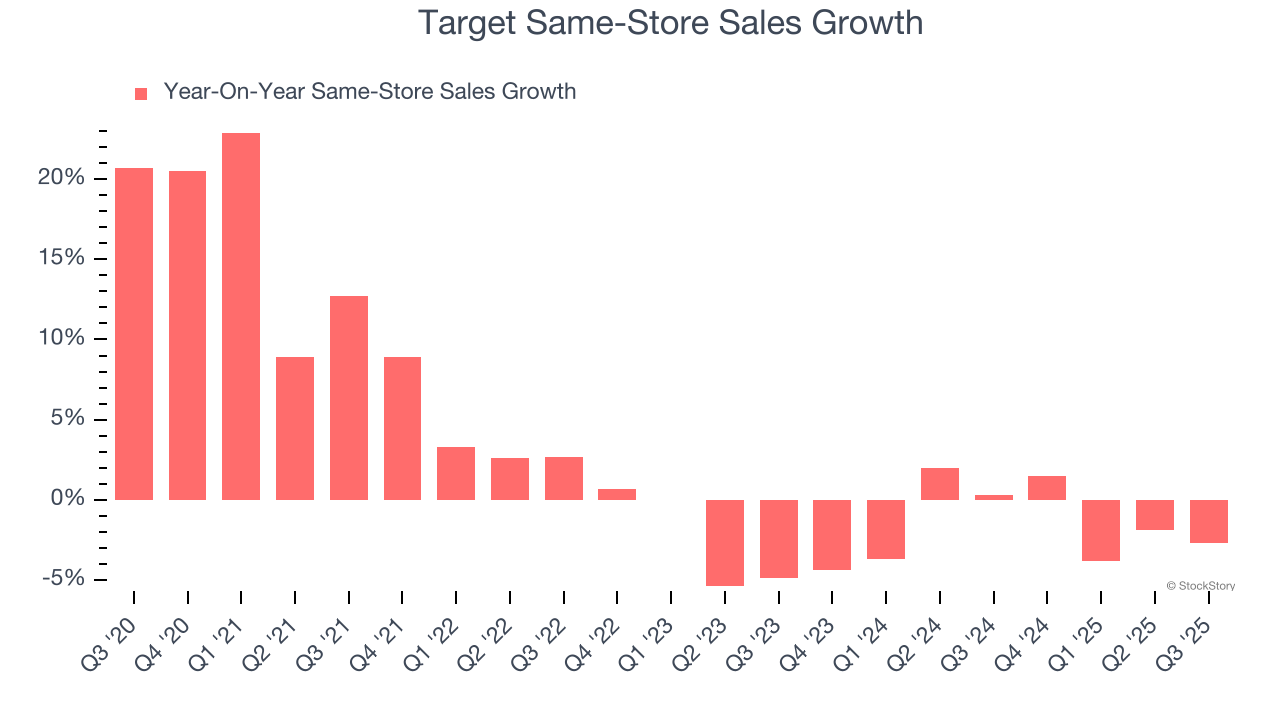

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Target’s demand has been shrinking over the last two years as its same-store sales have averaged 1.6% annual declines.

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Target has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 28% gross margin over the last two years. Said differently, Target had to pay a chunky $72.00 to its suppliers for every $100 in revenue.

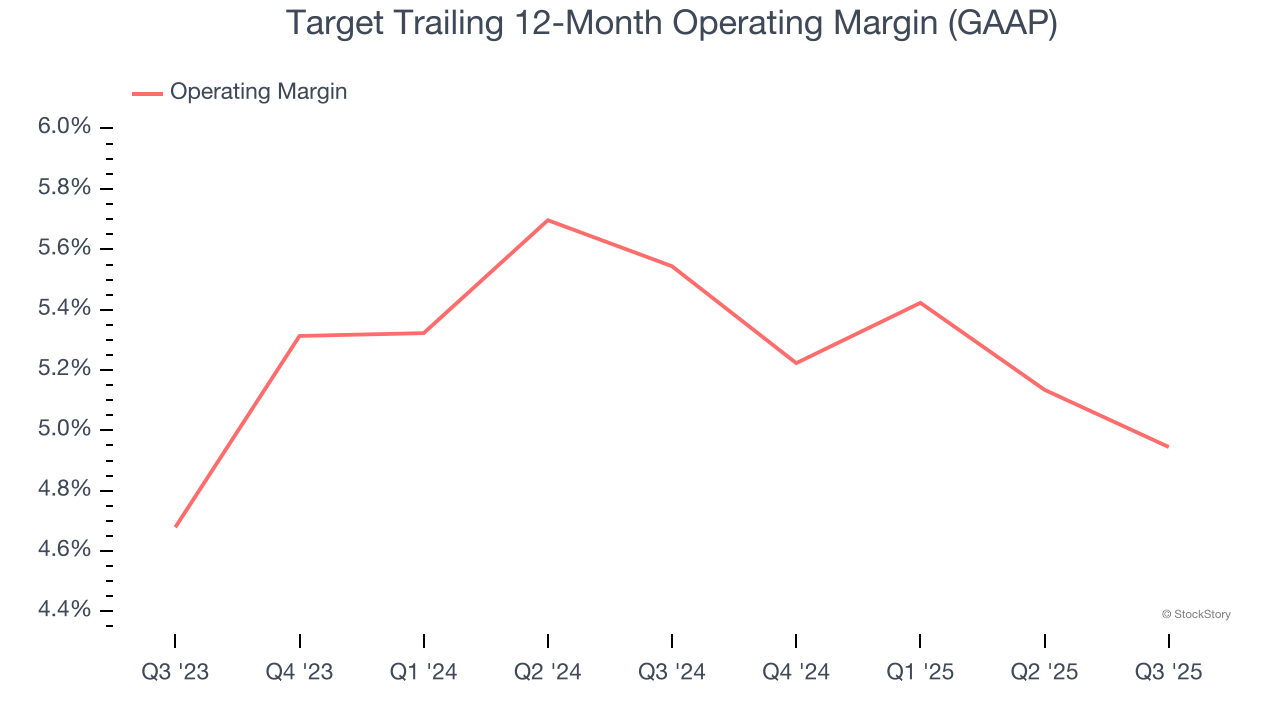

Operating margin is a key profitability metric because it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Target’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 5.2% over the last two years. This profitability was paltry for a consumer retail business and caused by its suboptimal cost structureand low gross margin.

Target doesn’t pass our quality test. With its shares lagging the market recently, the stock trades at 13× forward P/E (or $98.08 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are better stocks to buy right now. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-29 | |

| Mar-29 | |

| Mar-28 | |

| Mar-27 | |

| Mar-26 | |

| Mar-26 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite