|

|

|

|

|||||

|

|

|

Cathay General Bancorp has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 8.6% to $49.46 per share while the index has gained 11.7%.

Is there a buying opportunity in Cathay General Bancorp, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

We don't have much confidence in Cathay General Bancorp. Here are three reasons why CATY doesn't excite us and a stock we'd rather own.

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

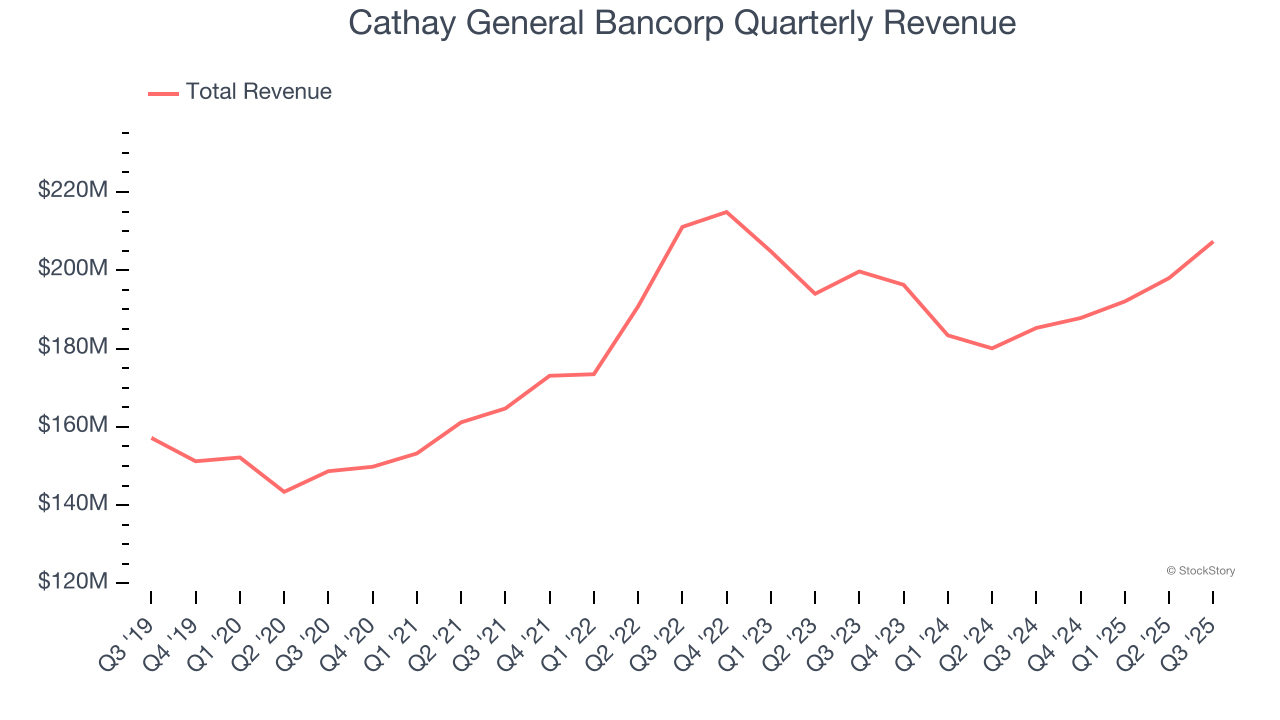

Unfortunately, Cathay General Bancorp’s 5.7% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the banking sector.

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Cathay General Bancorp’s net interest income has grown at a 5.4% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue.

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Cathay General Bancorp’s EPS grew at an unimpressive 9% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 5.7% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Cathay General Bancorp’s business quality ultimately falls short of our standards. That said, the stock currently trades at 1.2× forward P/B (or $49.46 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better investments elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-09 | |

| May-15 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-09 | |

| Feb-27 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite