|

|

|

|

|||||

|

|

|

Growth at Amazon's cloud computing segment is reaccelerating.

Advertising services is the fastest-growing division within Amazon.

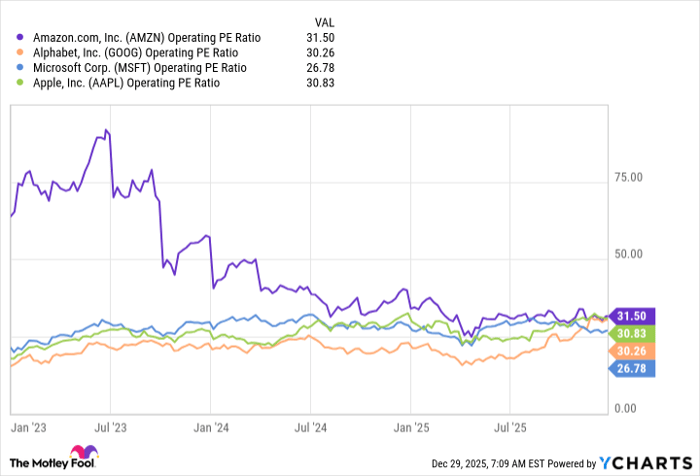

Yet, the tech giant's stock is at the same valuation level as its peers.

Amazon had a disappointing 2025, with the stock only rising around 6% while the S&P 500 gained around 18%. That's a sharp underperformance and will have been frustrating for investors since nearly every other big tech company had a much better year. However, thanks to its underperformance, Amazon may be slated to enjoy a much better year ahead.

So, could Amazon be the comeback stock of the year in 2026? I've got three reasons why I think that will be the case, and investors should consider adding Amazon to their portfolio as a result.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Amazon.

Although Amazon Web Services (AWS) may not be the first thing you think of when you hear Amazon, it's the most important in my opinion. AWS is Amazon's cloud computing wing, and is benefiting from two massive tailwinds.

First is the general migration to the cloud. Before cloud computing, companies had to host websites on premises and maintain expensive networking equipment. They also had to maintain servers to hold information, and if a server went down, it could have catastrophic consequences.

Now, many companies are migrating these workloads to the cloud, and AWS is the largest cloud provider in the market.

Cloud computing is also a key part of artificial intelligence, as few companies have the resources to build out their own data centers to house expensive computing equipment. Instead, many are opting to rent computing power from AWS to run these workloads, which is kick-starting a new phase of growth for AWS.

In the third quarter, the AWS segment saw revenue rise 20% year over year -- its fastest growth rate in multiple years. This is a big deal for Amazon, as AWS accounted for 66% of operating profits during the quarter. With Amazon's most profitable business unit reaccelerating its growth rate and well-positioned to cash in on two massive trends toward the cloud, it bodes well for Amazon's future.

Another key part of Amazon's business is advertising. Although Amazon doesn't break out its operating margin as it does with AWS, it's obvious that advertising services have played a key role in boosting Amazon's commerce operating margins over the past few years. Most advertising companies have an operating margin of around 30% to 40%. And so with Amazon's ad services generating $17.7 billion in revenue during Q3, the low end of that range would indicate $5.3 billion in operating profits.

In Q3, Amazon's North American and international commerce businesses combined to produce about $6 billion in operating profits. This shows how critical Amazon's ad services are for overall profitability. With advertising services posting the fastest growth rate of any division in Q3 (rising 24% year over year), this sets Amazon up nicely for a strong 2026.

Before 2025, I would have been fine with someone calling Amazon's stock overvalued. Compared to other big tech players, Amazon's stock carried a premium valuation from an operating price-to-earnings ratio standpoint.

AMZN Operating PE Ratio data by YCharts

Now, it's right in the middle of the pack, trading at a valuation level comparable to its peers. This allows the stock price for Amazon's stock to rise and fall alongside its business performance, rather than have its business gains go toward offsetting an expensive valuation.

For 2026, Wall Street analysts expect Amazon to grow sales at around 11%. That's about market average pace, which shouldn't come as a surprise to investors. The big deal will be how much Amazon's operating profits grow. As long as AWS and advertising services continue to post excellent results, its operating profit growth should be faster than revenue growth, leading to stock outperformance.

If Amazon can deliver that, I have no doubt that it will mount a huge comeback in 2026. If it fails to do that, then 2026 could be another disappointing year for Amazon shareholders.

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $505,641!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,143,283!*

Now, it’s worth noting Stock Advisor’s total average return is 974% — a market-crushing outperformance compared to 193% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 2, 2026.

Keithen Drury has positions in Amazon. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.

| 30 min | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours |

Globalstar Stock Jumps After Report Amazon Is In Talks To Acquire Satellite Firm

AMZN

Investor's Business Daily

|

| 8 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite