|

|

|

|

|||||

|

|

|

Micron has been in the spotlight, but another company is also benefiting from the memory boom.

Lam Research stock has more than doubled in 2025, and it still trades at a reasonable valuation.

This company can continue soaring as memory manufacturers boost their production capacity.

The memory industry has been in red-hot form over the past couple of years. Market research firm Yole Group estimates that the industry's revenue grew by a whopping 78% in 2024 to $170 billion, followed by another healthy double-digit increase in 2025 to $200 billion.

The good news is that the memory industry is poised to deliver solid growth once again in 2026. Massive demand for high-bandwidth memory (HBM) deployed in artificial intelligence (AI) server chips has created a supply shortage in the memory industry, bumping up prices as a result.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Not surprisingly, companies such as Micron Technology (NASDAQ: MU) have been witnessing phenomenal growth in their revenue and earnings. The memory specialist's revenue jumped by 57% year over year in the most recent quarter to $13.6 billion, while non-GAAP (adjusted) earnings jumped by nearly 2.7 fold. Micron expects its growth to accelerate significantly in the current quarter, driven by the favorable demand-supply dynamics.

Micron's attractive valuation makes it one of the best ways to capitalize on the growth of the memory market in 2026 and beyond. However, we will take a look at another key memory industry player that's also set to win big from this market's booming growth: Lam Research (NASDAQ: LRCX).

Image source: Getty Images.

The demand for AI-focused HBM chips is so strong that manufacturers are unable to fulfill orders. That's not surprising, as the dynamic random-access memory (DRAM) industry bit shipments are estimated to have increased in the low-20% range in 2025, according to Micron CEO Sanjay Mehrotra. He anticipates bit shipments to increase by around 20% in the new year, which isn't a major improvement.

However, Micron has significantly raised its HBM revenue estimate. It now expects these chips to pull in $100 billion in revenue by 2028 as compared to $35 billion in 2025. It was previously expected that the HBM industry would achieve the $100 billion milestone by 2030. Micron, therefore, is now forecasting the HBM industry to grow at an annual rate of almost 42%, which is significantly higher than its prior estimate of 23% annual growth.

Also, the anticipated growth in HBM is much higher than the estimated growth in memory bit shipments. While this will lead to an increase in prices, it also means that the likes of Micron will be unable to meet all the demand that's coming their way. As a result, Micron and its peers are raising their capital expenses to bring additional production capacity online.

Micron, for instance, has raised its fiscal 2026 capital expenditure budget to $20 billion from the prior estimate of $18 billion to support HBM demand. That would be a 45% increase over its fiscal 2025 capex. Samsung, on the other hand, is reportedly planning to bump its HBM capacity by 50% in 2026, as per reports.

Similarly, SK Hynix is reportedly going to start HBM production at one of its facilities four months ahead of schedule. It would be ramping up the capacity at this facility by a big margin by the end of 2026. All this is good news for a company that gets a nice chunk of its revenue from selling memory manufacturing equipment, like Lam Research.

Lam Research made investors significantly richer in 2025, with the stock rising 143% during the year. The stock can still be bought at an attractive 11.5 times sales and 36 times forward earnings despite this surge. Buying this memory stock looks like the right thing to do as its red-hot run isn't over yet.

Its revenue in the previous quarter (which ended on Sept. 28) increased by 28% from the prior year to $5.32 billion, while earnings increased by 44%. The company attributed this impressive growth to "better than expected high-bandwidth memory or HBM-related investments," as pointed out by CEO Tim Archer on the company's earnings call. Lam gets 34% of its revenue from selling memory equipment.

The CEO is confident that spending on memory and other semiconductor equipment will remain robust in 2026, driven by AI-related demand. That's not surprising considering the moves that Micron, Samsung, and SK Hynix are making to shore up the production of HBM. Even better, Lam points out that the booming demand for AI data centers, which require HBM, high-speed storage, and advanced processing chips, is going to substantially expand its total addressable market (TAM).

Lam estimates that for every $100 billion in data center investment, an additional $8 billion in wafer fabrication equipment (WFE) spending is required. At the same time, the company notes that converting existing manufacturing facilities to produce more advanced storage chips could increase its addressable market by $40 billion over the next few years.

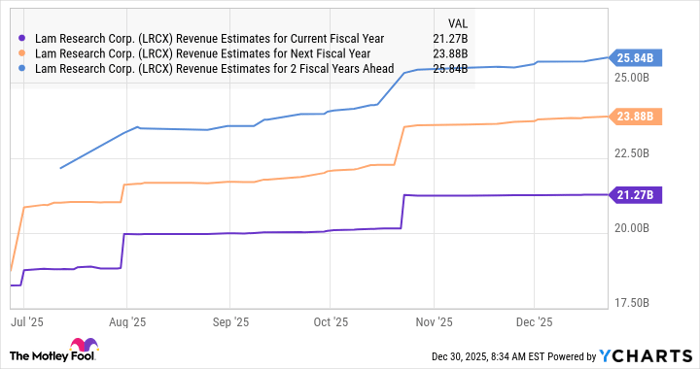

Lam Research is expected to clock $21.3 billion in revenue in the current fiscal year, an increase of 15% from the prior year. Analysts are expecting it to grow at healthy rates over the next couple of years as well.

LRCX Revenue Estimates for Current Fiscal Year data by YCharts

However, don't be surprised if it exceeds those expectations, considering the extent of the addressable opportunity discussed above. As the company outperforms Wall Street's expectations in 2026 and in the long run, its stock price could continue to rise. All this makes Lam Research a top AI stock to buy right now, as it is on track to benefit from higher spending on memory equipment, as well as an increase in overall semiconductor spending to support the proliferation of AI.

Before you buy stock in Lam Research, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lam Research wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $505,641!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,143,283!*

Now, it’s worth noting Stock Advisor’s total average return is 974% — a market-crushing outperformance compared to 193% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 2, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Lam Research. The Motley Fool has a disclosure policy.

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite