|

|

|

|

|||||

|

|

|

What a time it’s been for Lattice Semiconductor. In the past six months alone, the company’s stock price has increased by a massive 58.7%, setting a new 52-week high of $80.75 per share. This performance may have investors wondering how to approach the situation.

Is now the time to buy Lattice Semiconductor, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

We’re happy investors have made money, but we're swiping left on Lattice Semiconductor for now. Here are three reasons there are better opportunities than LSCC and a stock we'd rather own.

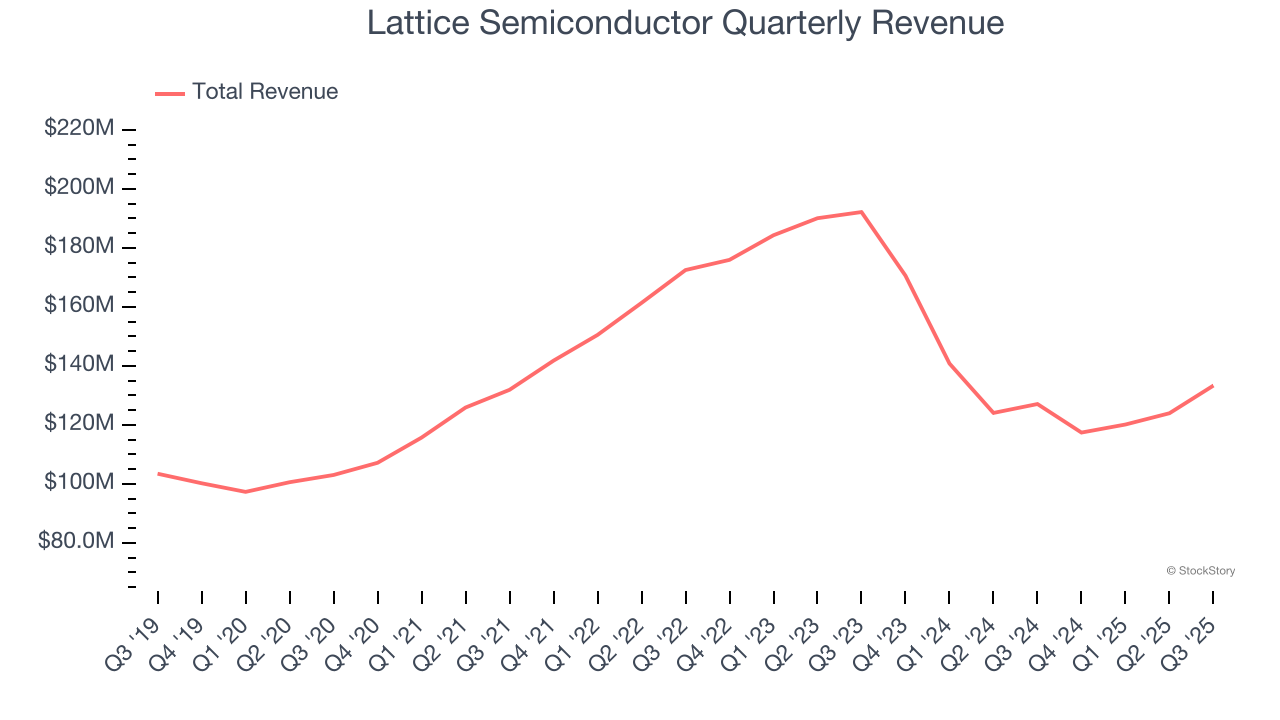

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Lattice Semiconductor’s 4.3% annualized revenue growth over the last five years was mediocre. This was below our standard for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

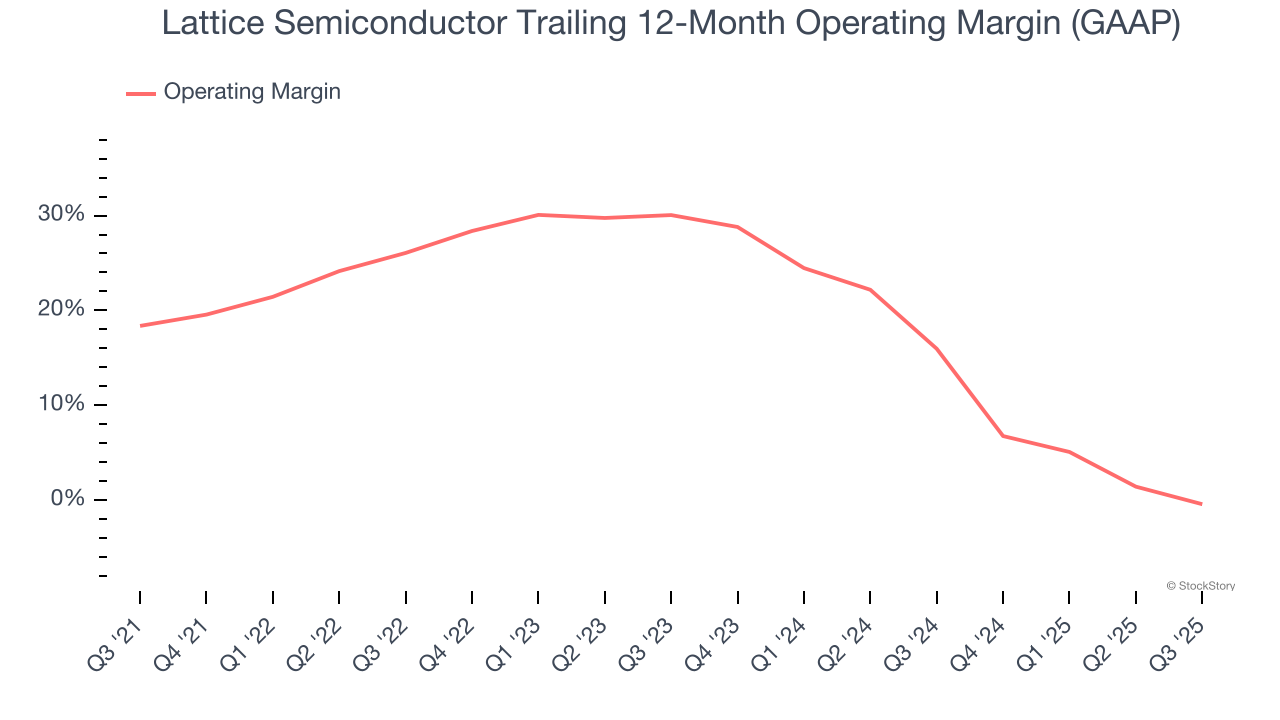

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Analyzing the trend in its profitability, Lattice Semiconductor’s operating margin decreased by 18.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Lattice Semiconductor’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was breakeven.

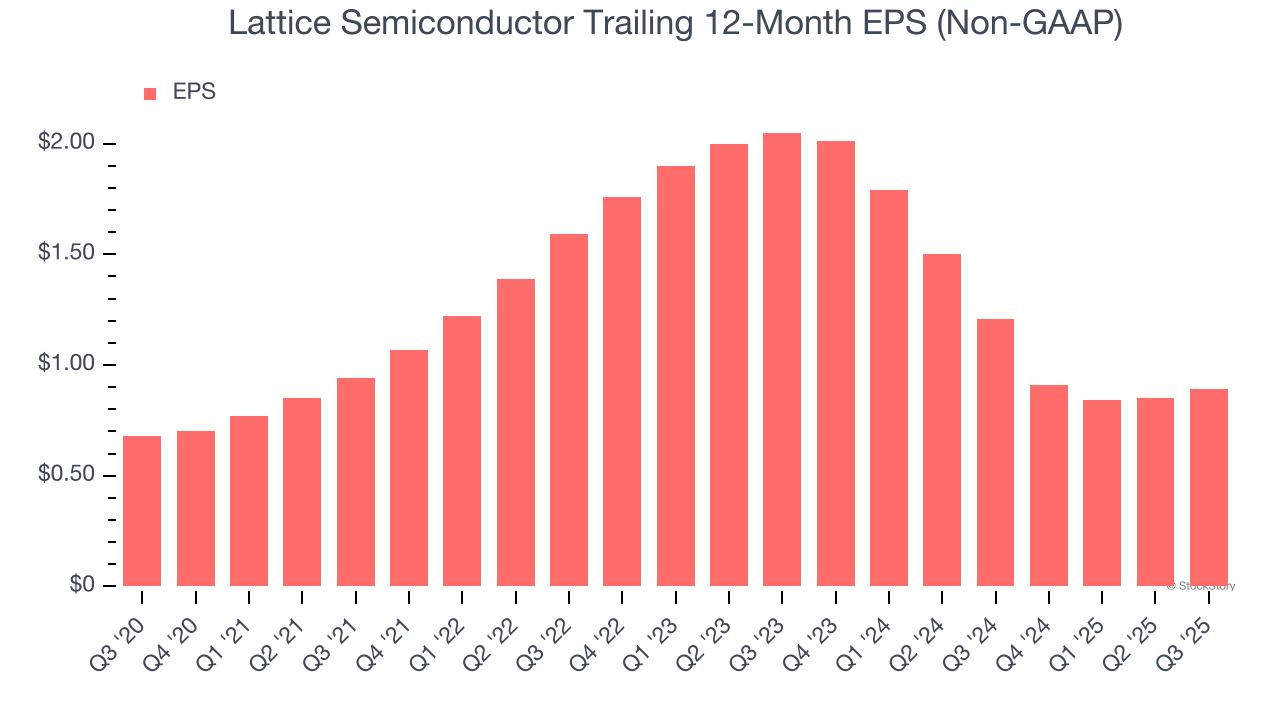

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Lattice Semiconductor’s unimpressive 5.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Lattice Semiconductor’s business quality ultimately falls short of our standards. Following the recent surge, the stock trades at 57.4× forward P/E (or $80.75 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-21 | |

| Jul-21 | |

| Jul-14 | |

| Jul-09 | |

| Jul-07 | |

| Jul-01 | |

| Jul-01 | |

| Jun-25 | |

| Jun-16 | |

| May-28 | |

| May-27 | |

| May-26 | |

| May-26 | |

| May-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite