|

|

|

|

|||||

|

|

|

Wintrust Financial has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 11.3% to $145.41 per share while the index has gained 10.1%.

Is now the time to buy Wintrust Financial, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We're cautious about Wintrust Financial. Here are three reasons we avoid WTFC and a stock we'd rather own.

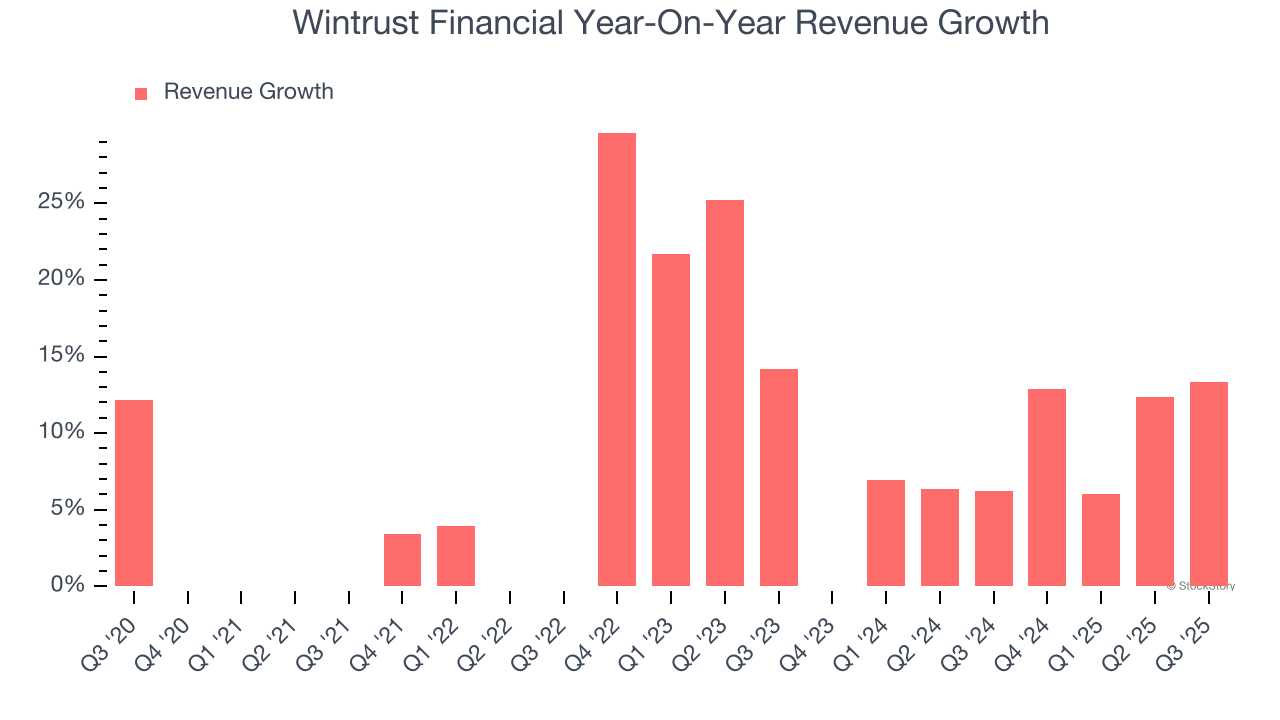

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. Wintrust Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 8.2% over the last two years was below its five-year trend.

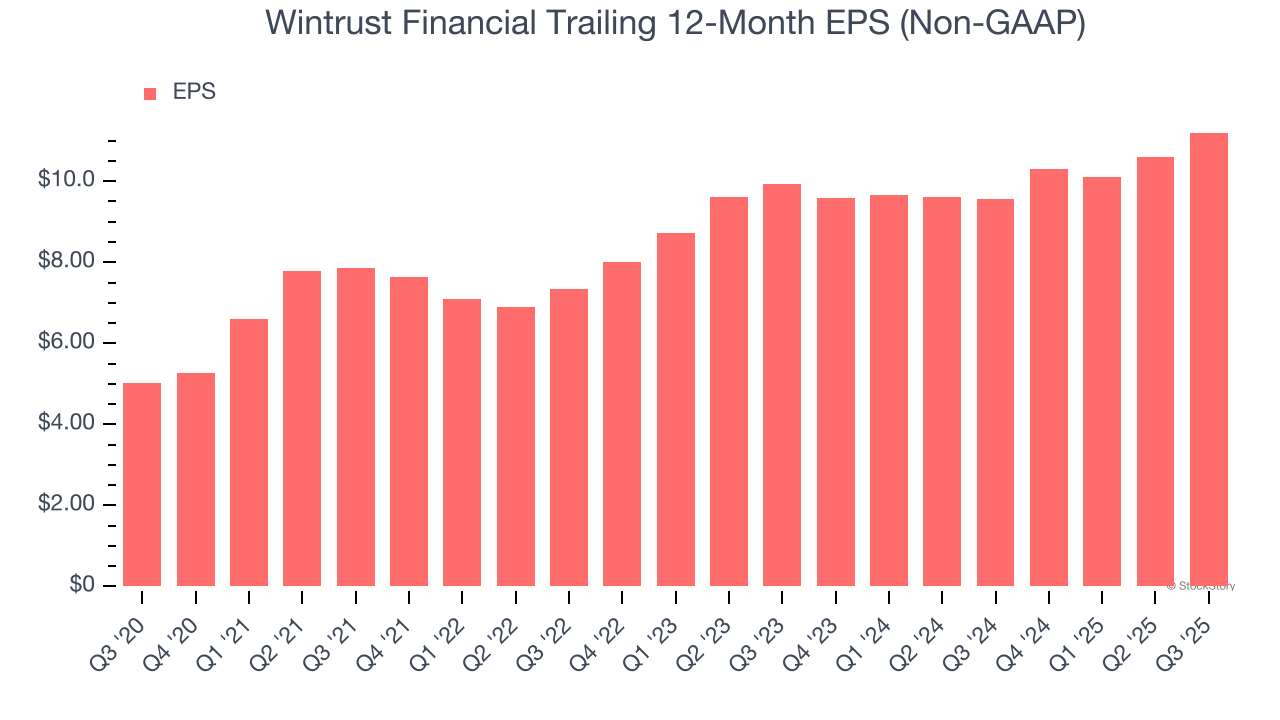

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Wintrust Financial’s EPS grew at a weak 6.1% compounded annual growth rate over the last two years, lower than its 8.2% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Wintrust Financial has averaged a Tier 1 capital ratio of 9.8%, which is considered unsafe in the event of a black swan or if macro or market conditions suddenly deteriorate. For this reason alone, we will be crossing it off our shopping list.

Wintrust Financial isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 1.4× forward P/B (or $145.41 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. We’d recommend looking at our favorite semiconductor picks and shovels play.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-06 | |

| Jun-30 | |

| Apr-22 | |

| Apr-21 | |

| Apr-20 | |

| Apr-20 | |

| Apr-15 | |

| Apr-09 | |

| Mar-18 | |

| Feb-26 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite