|

|

|

|

|||||

|

|

|

Consolidated Edison’s ED capital investment program is expected to strengthen its core infrastructure and operational capabilities, leading to improved service reliability for customers and greater resilience against system stresses.

However, this Zacks Rank #3 (Hold) company faces risks related to regulator-approved rate plans.

Consolidated Edison continues to follow a systematic capital investment plan for infrastructure development and maintain the reliability of its electric, gas and steam delivery systems. The company has a robust capital expenditure plan of $38 billion through 2029. Over the next 10 years, it aims to invest $72 billion in significant energy infrastructure. Such investments should enable it to provide reliable, resilient, safe and clean energy to its customers.

With industries across the board rapidly adopting clean energy as their preferred choice of energy source, utility providers like Consolidated Edison are expanding their renewable energy portfolio to earn the economic and environmental, social, and governance incentives offered by the utility-scale renewable energy market.

The company is currently building the Brooklyn Clean Energy Hub, a transmission substation designed to strengthen New York’s power grid and provide flexibility for offshore wind resources to interconnect during construction and after operations commence. This hub, expected to be completed by 2028, should be able to accommodate up to 1,500 megawatts (MW) of electricity.

The company’s pricing is regulated by state utility authorities, which approve the amount the utility is allowed to charge customers for electricity or gas. These approved rate plans are designed to let the company recover most of its operating and investment costs, and to earn a reasonable return on the money it has invested. However, the plan includes rate-related conditions. If actual costs rise faster than expected, are disallowed by regulators, or occur between rate cases, the company may be unable to pass all such costs on to customers, meaning full cost recovery is not guaranteed.

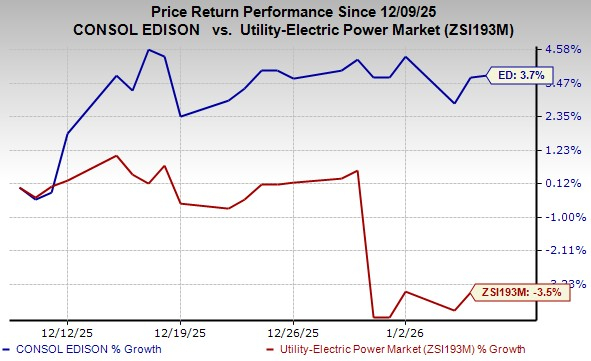

In the past month, shares of the company have risen 3.7% against the industry’s 3.5% decline.

Some better-ranked stocks from the same industry are NiSource NI, Alliant Energy LNT and Edison International EIX, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

NiSource’s long-term (three to five years) earnings growth rate is 7.93%. The Zacks Consensus Estimate for NI’s 2026 earnings per share (EPS) implies an improvement of 8.2% year over year.

LNT’s long-term earnings growth rate is 7.15%. The company delivered an average earnings surprise of 13.5% in the last four quarters.

EIX’s long-term earnings growth rate is 10.93%. The Zacks Consensus Estimate for EIX’s 2026 EPS implies an improvement of 2.8% year over year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-24 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite