|

|

|

|

|||||

|

|

|

The big-box retailer’s issues extend beyond industry-wide slowdowns in consumer discretionary spending.

To boost foot traffic, Target must capitalize on its differentiating factors, such as exclusive partnerships and a competitive product lineup.

Even in a slowdown, Target generates substantial earnings that easily cover its generous dividend.

Target (NYSE: TGT) fell 27.7% in 2025, drastically underperforming the 16.4% gain in the S&P 500 (SNPINDEX: ^GSPC). The stock is now down a mind-numbing 61.7% from its all-time high, but has rallied more than 22% from its 52-week low, which was made in November.

Here's why Target's issues are far from over, and if the high-yield value stock is too cheap to ignore in 2026.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Target.

Target can't compete with Walmart or Amazon on price. Its business model depends more on the shopping experience, such as in-store Starbucks and Ulta Beauty locations, high-profile exclusive partnerships with celebrities like Taylor Swift, or its latest Valentine's Day exclusive with tumbler maker Stanley. Target is at its best when consumers are shopping in store on discretionary items like home décor and clothes -- not just low-margin essentials and groceries.

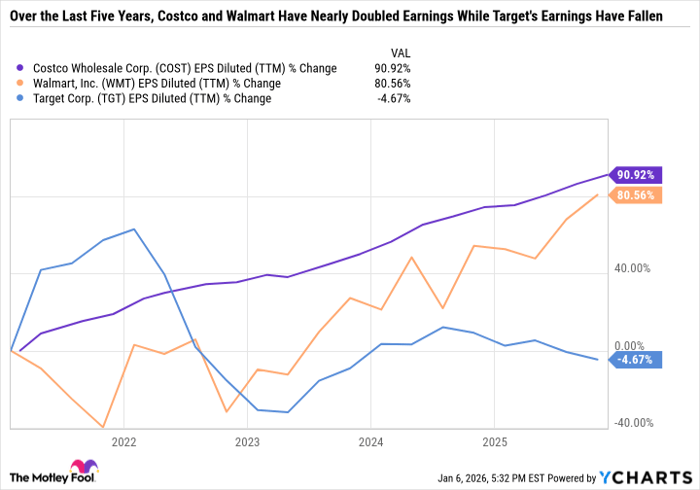

But with consumers spending strained by living costs outpacing wage growth, the in-store shopping experience is becoming less important. So consumers are turning to Walmart for value and bulk buying at Sam's Club and Costco.

COST EPS Diluted (TTM) data by YCharts

Target has struggled because it has failed to align its inventories with actual demand, leading to consistent price markdowns and promotions that reduce inventory but crush margins.

It has also faced significant backlash in recent years. In summer 2023, it was heavily criticized for its Pride Month merchandise. And then in early 2025, it reversed course and rolled back its diversity, equity, and inclusion (DEI) programs. Some consumers like supporting brands that align with their views -- or at least, a brand that doesn't outwardly go against them. Target had a reputation for being inclusive. However, that brand position eroded with the rollbacks of DEI, leading some consumers to boycott Target outright.

To further stir the pot, Target Chief Operating Officer Michael Fiddelke is taking over as CEO in February, replacing Brian Cornell, who was CEO for more than a decade and was instrumental in keeping Target relevant through the rise of Amazon and e-commerce.

Target has made blunder after blunder, is dealing with a downturn in consumer spending, costs associated with retail shrinkage (largely from theft), and is undergoing a major change at the executive level.

Entering 2026, it doesn't appear that there are clear answers to Target's issues either, as wage growth and hiring could be under pressure from macroeconomic challenges, geopolitical policy, and uncertainties regarding the impact of artificial intelligence on the labor market.

However, Target does have a plan to return to growth by improving its supply chain and fulfillment capabilities, growing its Target Circle rewards program, improving its products through innovation to keep customers engaged in-store and online, and tapping back into the "Tarzhay" spirit.

Target is already making progress, as its trailing-12-month operating margin is back above 5% -- which is a big improvement from a couple of years ago. And sales growth is ticking down slightly, but only by low single-digits.

TGT Revenue (TTM) data by YCharts

Target is forecasting $7 to $8 in adjusted fiscal 2025 earnings per share (EPS). Analyst consensus estimates have Target producing $7.31 in fiscal 2026 EPS (begins on Feb. 1) and $7.68 in fiscal 2027.

These projections are a far cry from the boom years during the pandemic. But with the stock hovering around just $102 per share, Target is dirt cheap from a valuation standpoint -- especially if it returns to modest earnings growth in the coming years.

Recency bias is a powerful psychological concept. If you closely follow markets, it's easy to think that poor-performing stocks will keep falling and red-hot stocks will never slow down. But Target's fundamentals point to an attractive deep value stock.

What's more, Target sports a 4.5% dividend yield, which is high-yield territory. And it has raised its dividend for 54 consecutive years, earning the company a spot on the list of Dividend Kings, which are companies that have boosted their payouts for at least 50 consecutive years.

Still, some investors may want to wait for the new CEO to take the helm next month, or for more concrete signs of a return to sales and earnings growth, before backing up the truck on Target.

Before you buy stock in Target, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Target wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $489,300!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,159,283!*

Now, it’s worth noting Stock Advisor’s total average return is 974% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 9, 2026.

Daniel Foelber has positions in Starbucks and Target. The Motley Fool has positions in and recommends Amazon, Starbucks, Target, Ulta Beauty, and Walmart. The Motley Fool has a disclosure policy.

| Jul-20 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite