|

|

|

|

|||||

|

|

|

Commercial Metals Company CMC reported solid first-quarter fiscal 2026 results, delivering year-over-year increases in its top and bottom lines. CMC also surpassed the Zacks Consensus Estimate on both metrics.

Commercial Metals shares have gained 51.6% in the past year compared with the industry’s 48.1% growth. In comparison, the Zacks Basic Materials sector and the S&P 500 have returned 41.8% and 23.5%, respectively.

The Steel-producer has also performed better than its peers like Nucor Corporation NUE and Cleveland-Cliffs Inc. CLF, which have rallied 35.5% and 21.7%, respectively.

Let us take a closer look at Commercial Metals’ fiscal first-quarter results to assess if this is the right time to buy CMC shares.

The company reported revenues of $2.12 billion, reflecting 11% year-over-year growth, attributed to solid demand for the North America Steel Group and Construction Solutions Group segments. However, this was partially offset by soft market conditions for the Europe Steel Group.

Even though demand in Europe continued to improve on strong Polish economic growth, import flows negatively impacted average price and margin levels. This, along with annual maintenance outages, pushed the Europe Steel Group’s adjusted EBITDA margin from 12.3% in the first quarter of fiscal 2025 to 4.4% in the first quarter of fiscal 2026.

In the North America Steel Group segment, the steel products metal margin increased by $132 per ton from the first quarter of fiscal 2025, achieving a year-over-year increase for the second consecutive quarter. The segment’s steel products margin climbed to the highest level in three years.

To better reflect the business composition, the company renamed its Emerging Businesses Group to Construction Solutions Group, effective as of the first quarter of fiscal 2025 . Solid demand and enhanced cost efficiency in the company’s Tensar division pushed the Construction Solutions Group segment’s adjusted EBITDA margin to a record 20%. The segment reported an adjusted EBITDA margin of 13.4% in the prior-year quarter.

Backed by the tailwinds, the company reported earnings per share of $1.84 in the quarter, a year-over-year surge of 142%. The Zacks Consensus Estimate for earnings and revenues was pegged at $1.55 and $1.99 billion, respectively.

CMC reported cash and cash equivalents, and restricted cash of $3 billion at the end of first-quarter fiscal 2026, with available liquidity of $1.9 billion. The company declared a quarterly dividend of 18 cents per share on Jan. 5, 2026, payable to stockholders of record as of Jan. 19, 2026. In comparison, Nucor maintains an annual dividend of $2.24, and Cleveland-Cliffs does not pay out any regular dividends as of now.

CMC closed two major acquisitions in December 2025 — Concrete Pipe and Precast, LLC ("CP&P") and Foley Products Company. The addition of these businesses will aid the company’s results in the second quarter of fiscal 2026, offsetting the impacts of seasonal slowdown within key markets.

However, the company will also bear several acquisition-related expenses in the fiscal second quarter, like transaction fees and debt issuance costs. CMC expects overall consolidated core EBITDA in the second quarter of fiscal 2026 to decline sequentially.

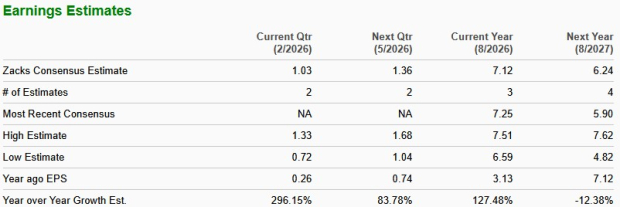

The Zacks Consensus Estimate for Commercial Metals’ fiscal 2026 sales is $8.54 billion, indicating a 9.6% year-over-year jump. The consensus mark for the year’s earnings is pegged at $7.12 per share, indicating a year-over-year upsurge of 127.5%.

The Zacks Consensus Estimate for fiscal 2027 sales implies a 3.9% year-over-year growth. The same for earnings suggests a dip of 12.4%.

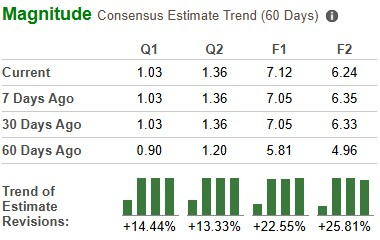

EPS estimates for fiscal 2026 have moved 22.5% north over the past 60 days, while the same for fiscal 2027 has moved up 25.8% over the past 60 days.

The recent acquisitions position Commercial Metals as a leading player in the Mid-Atlantic and Southeastern regions, which will operate one of the largest precast concrete platforms in the United States.

CMC has identified operational annual run-rate synergies of $25-$30 million from Foley and CP&P by year three, with additional synergies expected to be recognized in the upcoming years.

Commercial Metals also launched the Transform, Advance, Grow Program in September 2024, which focuses on driving higher through-the-cycle margins, earnings, cash flows, and ROIC. The company expects an annualized EBITDA benefit of $150 million in fiscal 2026 from the program.

Moreover, the company has a strong liquidity, financial position and focus on reducing debt through a capital allocation approach, which will likely stoke growth.

Commercial Metals is currently trading at a forward price/sales ratio of 0.93 compared with the industry's 1.56.

Peer Cleveland-Cliffs is a cheaper option, trading at a forward price/sales ratio of 0.31, while Nucor is trading at a higher price/sales ratio of 1.07.

CMC has delivered a strong stock performance and reported improved fiscal first-quarter results, with solid demand. It remains well-positioned to gain from the recent buyouts.

With an appealing valuation and upward earnings estimate revisions, now appears to be a favorable time to consider adding the stock to your portfolio. The company’s Zacks Rank #1 (Strong Buy) supports our thesis. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-28 | |

| Jul-28 |

Steel Tariffs Are Working Even as Imports Edge Up, Nucor CEO Says

NUE +7.17%

The Wall Street Journal

|

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite