|

|

|

|

|||||

|

|

|

Novo Nordisk NVO shares have surged 18.8% in the past month. The stock price gain was primarily induced by the much-anticipated FDA approval of NVO’s Wegovy pill (once-daily oral semaglutide 25 mg) for obesity and reducing the risk of cardiovascular events.

The approval of oral Wegovy in late December and its subsequent launch in early January mark a major milestone for Novo Nordisk, making it the first GLP-1 RA available in an oral form for weight management. Compared to injectable formulations, the pill offers a far more convenient administration option, significantly reducing the treatment burden and potentially improving patient adherence.

By beating Eli Lilly LLY to market with an oral obesity drug, Novo Nordisk has gained a meaningful competitive edge at a time when rising rivalry has pressured its market share. The new pill is likely to reignite demand for Wegovy and help reaccelerate growth that has softened in recent quarters. However, Eli Lilly remains close on the heels of Novo Nordisk as its regulatory application seeking the approval of its oral GLP-1 pill, orforglipron, for obesity is currently under review by the FDA.

The stock price rally has also likely been influenced by the submission of a regulatory application seeking approval for Novo Nordisk’s next-generation once-weekly injection, CagriSema, for weight management. The FDA is expected to review the application in 2026.CagriSema is a fixed-dose combination of a long-acting amylin analogue, cagrilintide 2.4 mg and Wegovy (semaglutide 2.4 mg). If approved, NVO’s CagriSema would be the first injectable therapy to combine a GLP-1 RA with an amylin analogue.

Despite the recent wins, Novo Nordisk is far from being out of the woods yet. The company stumbled through 2025 despite finally resolving U.S. supply constraints for its semaglutide-based GLP-1 blockbusters — Ozempic for type II diabetes (T2D) and Wegovy for obesity. NVO had cut its sales and operating profit growth outlook twice in 2025 due to weaker-than-expected momentum of Ozempic and Wegovy because of intensifying GLP-1 competition from Eli Lilly, foreign exchange headwinds, and widespread compounded semaglutide use in the United States.

To turn things around, Novo Nordisk underwent a major structural shift, appointing a new CEO and making significant changes to its board of directors. CEO Mike Doustdar announced a major restructuring program in September 2025 to streamline operations and reinvest in its core diabetes and obesity businesses.

Novo Nordisk is also facing mounting U.S. pricing pressure and has introduced early self-pay price cuts for Wegovy and Ozempic in 2025 to revive demand, expand access and counter intensifying competition, particularly from Eli Lilly. While the strategy aims to regain market share across diabetes and obesity, investors remain cautious as aggressive discounting risks margin compression and adds uncertainty to NVO’s long-term GLP-1 economics, competitive position and medium-term growth outlook. Let’s dig deeper and understand the company’s strengths and weaknesses to understand how to play the stock.

Novo Nordisk’s success in recent years has been driven by the sales of Ozempic and Rybelsus (oral) for T2D, and Wegovy for obesity. Despite recent market turmoil, the company is still a dominant player in the diabetes and obesity care market, with one of the industry's broadest portfolios.

Ozempic and Wegovy are the major revenue drivers, generating DKK 152.5 billion in the first nine months of 2025. Novo Nordisk is expanding access to Wegovy through broader distribution and partnerships with major U.S. pharmacies, telehealth providers, and proprietary and third-party platforms to ensure patients can obtain authentic, FDA-approved treatments. If successful, this strategy could help shift demand away from compounded alternatives and reignite Wegovy’s sales momentum in 2026.

Novo Nordisk is expanding semaglutide's reach through new indications. Wegovy injection is now approved for reducing major cardiovascular events, easing HFpEF symptoms, and relieving osteoarthritis-related knee pain in obesity.

Rybelsus’ label in the United States and the EU has been expanded to include cardiovascular benefits in diabetes patients. A 7.2 mg Wegovy dose, showing up to 25% weight loss in the STEP UP study, is under review in the United States and the EU. Label expansion is also being sought for Ozempic in treating peripheral artery disease in the United States and the EU.

Eli Lilly is Novo Nordisk’s fierce competitor in the diabetes/obesity space. Despite being on the market for a shorter period, LLY’s tirzepatide-based injections, Mounjaro (T2D) and Zepbound (obesity), have become its key top-line drivers, eating away market share from NVO. Following strong third-quarter results, Eli Lilly raised its 2025 full-year revenue and EPS guidance. In the first nine months of 2025, the drugs generated combined sales of $24.8 billion, accounting for 54% of Eli Lilly’s total revenues.

Beyond its GLP-1 portfolio, Novo Nordisk is broadening its presence in rare diseases. The company has submitted a regulatory filing seeking approval for Mim8 in hemophilia A in the United States. NVO has also secured both EU and U.S. approvals for Alhemo to treat hemophilia A and B, with or without inhibitors.

The FDA has also granted accelerated approval to Wegovy as the first GLP-1 therapy to treat noncirrhotic metabolic dysfunction-associated steatohepatitis with moderate-to-advanced liver fibrosis. This marked a significant milestone in liver care by offering patients a treatment that can both halt disease activity and reverse liver damage.

Novo Nordisk is also developing several next-generation obesity candidates in its pipeline, especially targeting the lucrative U.S. market. Apart from CagriSema, currently awaiting FDA evaluation, NVO is gearing up to launch a dedicated late-stage program evaluating cagrilintide as a monotherapy for obesity.

Novo Nordisk is also gearing up to advance another next-generation candidate, amycretin, for weight management into late-stage development. The phase III program on amycretin is planned to be initiated during the first quarter of 2026. The company is also developing oral monlunabant in a mid-stage obesity study. It recently signed a $2.2 billion deal with Septerna for developing and commercializing oral small-molecule medicines for treating obesity, diabetes, and other cardiometabolic diseases.

In the past six months, Novo Nordisk shares have lost 13.2% against the industry’s 19.1% growth. The company has also underperformed the sector and the S&P 500 during the same time frame, as seen in the chart below.

Novo Nordisk is trading at a discount to the industry, as seen in the chart below. Going by the price/earnings ratio, the company’s shares currently trade at 17.02 forward earnings, which is lower than 17.56 for the industry. The stock is trading much below its five-year mean of 29.25.

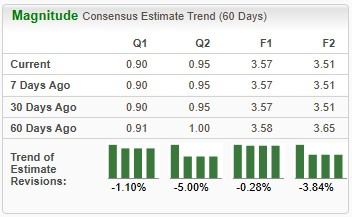

Earnings estimates for 2025 have deteriorated from $3.58 to $3.57 per share over the past 60 days. During the same time frame, Novo Nordisk’s 2026 earnings estimates have declined from $3.65 to $3.51.

Novo Nordisk, currently carrying a Zacks Rank #3 (Hold), has had a good start to 2026 with the approval and launch of oral Wegovy, making it the first company to bring a GLP-1 pill to market. The easier-to-use formulation of oral Wegovy gives Novo Nordisk a competitive edge over Eli Lilly, which is still awaiting FDA review for its oral GLP-1 candidate. Sentiment has also been supported by the regulatory filing for CagriSema, a next-generation injectable combination therapy that could further strengthen Novo Nordisk’s obesity franchise if approved in 2026. Together, these developments have reinforced confidence in the company’s innovation engine and its long-term leadership in diabetes and obesity care.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

However, the bigger picture remains challenging. Novo Nordisk struggled through 2025 despite resolving U.S. supply constraints, cutting its growth guidance twice amid intensifying competition from Eli Lilly, foreign-exchange headwinds, and widespread use of compounded semaglutide in the United States. The company is also facing mounting pricing pressure and has introduced early self-pay discounts for Wegovy and Ozempic, raising concerns around margin compression and long-term GLP-1 economics. A major management reshuffle and restructuring program raises operational risk for the company. Analysts also continue to trim earnings estimates, leaving valuations at risk of further downside.

Moreover, competition in the obesity treatment market is intensifying as the space attracts new contenders beyond leaders Eli Lilly and Novo Nordisk. Smaller biotech firms, like Viking Therapeutics VKTX, are advancing GLP-1–based therapies to challenge the incumbents. Viking Therapeutics is developing its dual GIPR/GLP-1 RA, VK2735, both as oral and subcutaneous formulations for the treatment of obesity. While Novo Nordisk retains strong fundamentals, a broad pipeline, and leadership in diabetes, obesity, rare diseases and liver care, near-term volatility is likely to persist. Long-term investors may consider staying invested given the company’s innovation depth and market positioning, but short-term investors are advised to steer clear to avoid ongoing volatility.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 7 hours | |

| 12 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite