|

|

|

|

|||||

|

|

|

New Elite Feature: Compare relative returns, fundamentals, and sector rankings head-to-head.

Carlyle trades at $65.68 and has moved in lockstep with the market. Its shares have returned 11.4% over the last six months while the S&P 500 has gained 11.1%.

Is now the time to buy CG? Find out in our full research report, it’s free.

Founded in 1987 with just $5 million in capital and named after the iconic New York hotel where the founders first met, The Carlyle Group (NASDAQ:CG) is a global investment firm that raises, manages, and deploys capital across private equity, credit, and investment solutions.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

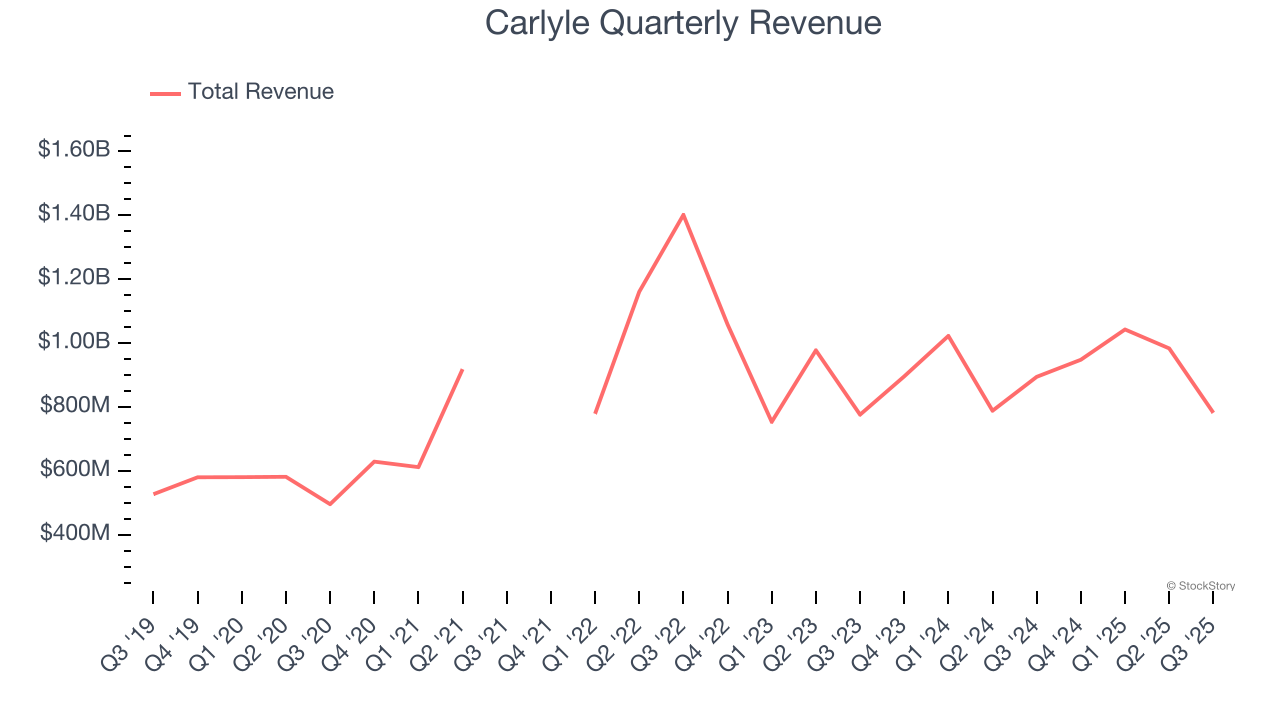

Luckily, Carlyle’s revenue grew at a decent 10.9% compounded annual growth rate over the last five years. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

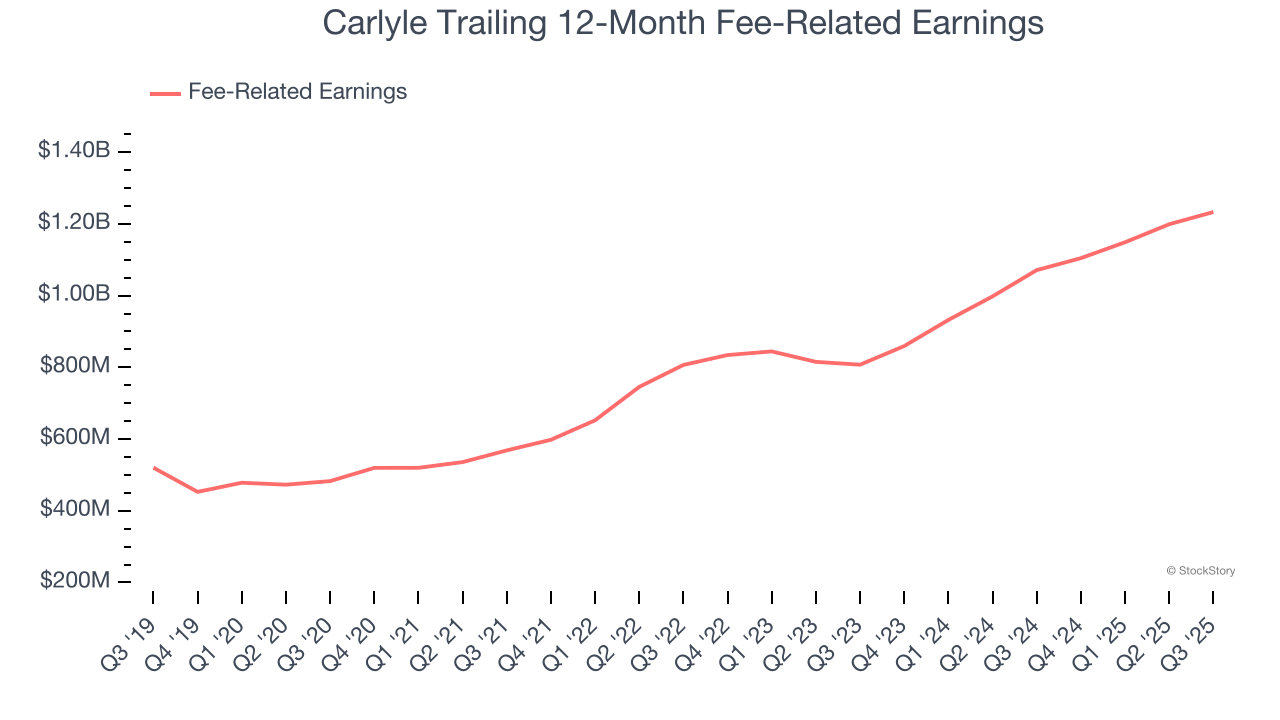

While revenue growth captures attention, the quality of that growth is what truly drives shareholder value. For asset management firms, fee-related earnings represent the stable, predictable profits from their core fee-based services, excluding the more unpredictable elements like performance fees and investment returns. This metric reveals the sustainable earnings power of the business.

Carlyle’s annual fee-related earnings growth over the last five years was 20.6%, a solid result.

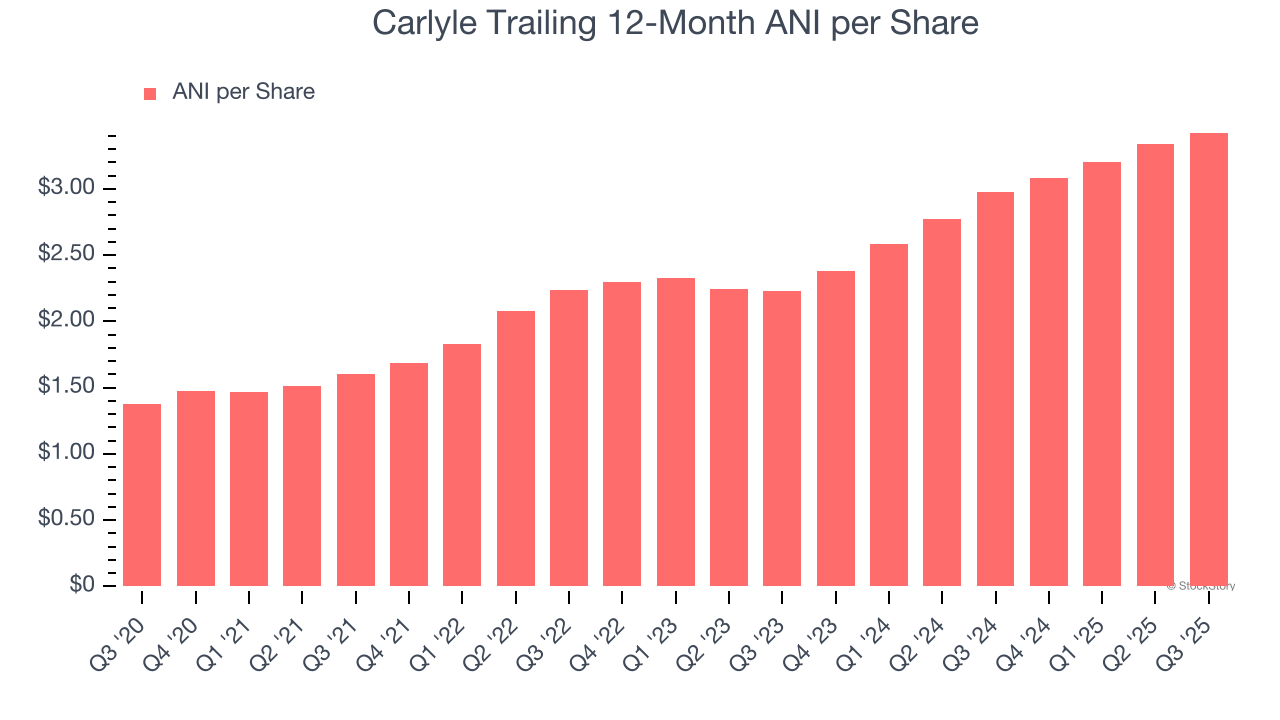

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Carlyle’s EPS grew at a remarkable 20% compounded annual growth rate over the last five years, higher than its 10.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

These are just a few reasons why we think Carlyle is a high-quality business, but at $65.68 per share (or 14.4× forward P/E), is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| 3 hours | |

| Jun-04 | |

| Jun-02 | |

| Jun-02 | |

| May-27 | |

| May-22 | |

| May-21 | |

| May-20 | |

| May-20 | |

| May-20 | |

| May-15 | |

| May-11 | |

| May-11 | |

| May-11 | |

| May-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite