|

|

|

|

|||||

|

|

|

Thermo Fisher Scientific Inc.’s TMO recent slew of strategic collaborations reflects its ongoing commitment to sustainable long-term growth. Additionally, the slew of product launches is expected to bolster the company’s top line. Meanwhile, a weak solvency and fierce competitive pressure raise concerns for Thermo Fisher’s operations.

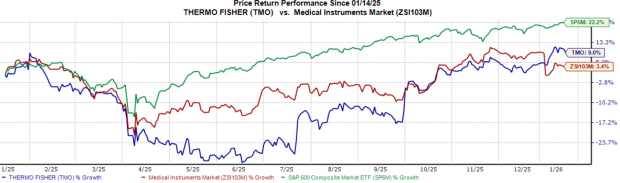

In the past year, this Zacks Rank #3 (Hold) stock has gained 9% compared with the industry’s 3.4% growth. The S&P 500 composite has gained 22.2% in the said period.

The renowned medical and laboratory equipment provider has a market capitalization of $231.23 billion. TMO has an earnings yield of 4% compared with the industry’s 0.6%. The company’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 3%.

Let’s delve deeper.

Strategic Acquisitions to Boost Growth: Thermo Fisher’s business strategy primarily includes expansion through strategic acquisition of technologies and businesses that augment its existing products and services. In September 2025, the company completed the $4.1 billion acquisition of Solventum’s Purification & Filtration business, now part of the Life Sciences Solutions segment. Last year, Thermo Fisher acquired Olink, a Swedish-based provider of next-generation proteomics solutions. The buyout advanced Thermo Fisher’s capabilities in the high-growth proteomics market by adding highly differentiated solutions.

Product Launch Impressive: Thermo Fisher continues to make significant investments in research and development (R&D) to deliver a steady flow of innovative products and strengthen its competitive position. The company introduced the Thermo Scientific Hypulse Surface Analysis System to accelerate the understanding of material surfaces. Thermo Fisher expanded the Efficient-Pro medium and feed system with Efficient-Pro Medium (+) Insulin, supporting optimized growth and productivity for insulin-dependent CHO cell lines with streamlined workflow and handling.

Other important launches this year include two next-generation Thermo Scientific Orbitrap mass spectrometers, the Invitrogen Attune Xenith Flow Cytometer and the Thermo Scientific Krios 5 Cryo-Transmission Electron Microscope (TEM).

Unfavorable Solvency: As of the end of the third quarter of 2025, Thermo Fisher reported cash and cash equivalents and short-term investments of $3.55 billion and current debt of $3.82 billion. Long-term debt totaled $31.86 billion. The company reported a leverage ratio of 3.2 times gross debt to adjusted EBITDA and 2.9 times on a net debt basis.

Image Source: Zacks Investment Research

Exposure to Foreign Currency: International markets account for a substantial portion of Thermo Fisher’s revenues and the company intends to continue expanding its presence in these regions. International revenues and costs are subject to foreign exchange risk, as fluctuations in currency exchange rates may adversely impact reported revenues and profitability when translated into U.S. dollars for financial reporting purposes. For instance, in the first quarter of 2025, currency translation had an unfavorable effect of 1% on revenues due to the strengthening of the U.S. dollar relative to other currencies in which the company sells its products and services.

The Zacks Consensus Estimate for earnings per share (EPS) has moved up 1 cent to $22.73 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2025 revenues is pegged at $44.27 billion, suggesting a 3.2% rise from the year-ago reported number.

Some better-ranked stocks in the broader medical space are Phibro Animal Health PAHC, Boston Scientific BSX and Envista NVST.

Phibro Animal Health has an earnings yield of 7.4% compared with the industry’s 0.2% yield. Shares of the company have surged 86.2% in the past year against the industry’s 5% decline. PAHC’s earnings outpaced estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 20.8%.

PAHC sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Boston Scientific, currently carrying a Zacks Rank #2 (Buy), has an estimated long-term earnings growth rate of 16.4% compared with the industry’s 13.9% growth. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 7.36%. BSX shares have surged 130.2% compared with the industry’s 5.2% growth in the past year.

Envista, carrying a Zacks Rank #2 at present, has an earnings yield of 5.4% compared with the industry’s 2.8% yield. Shares of the company have jumped 13.9% compared with the industry’s 5.2% growth. NVST’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 12.8%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

The 'Standout Performance' That Could Save Thermo Fisher, Danaher And Others

TMO +8.71%

Investor's Business Daily

|

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite