|

|

|

|

|||||

|

|

|

Dell Technologies DELL is suffering from a decline in gross margin, which contracted 140 basis points (bps) year over year to 21.1% in the third quarter of fiscal 2026. The dip was primarily driven by a more competitive pricing environment, particularly in the Client Solutions Group segment, and an unfavorable geographical mix within traditional servers.

However, DELL’s Infrastructure Solutions Group (ISG) segment played a key role in supporting overall gross margin performance. In the third quarter of fiscal 2026, ISG revenues increased 24% year over year to $14.10 billion. The upside can be attributed to servers and networking revenues of $10.12 billion, which grew 37% year over year, driven by accelerating AI server demand.

In the third quarter of fiscal 2026, the company booked $12.3 billion in AI server orders, bringing year-to-date orders to $30 billion. The company shipped $5.6 billion worth of AI servers in the fiscal third quarter. The company concluded the fiscal third quarter with a record backlog of $18.4 billion in AI server orders, underscoring the sustained demand for its AI solutions. DELL expects to ship $9.4 billion in AI servers in the fiscal fourth quarter of 2026, which would bring full-year shipments to $25 billion, representing more than 150% year-over-year growth.

The strength of ISG, particularly in AI servers and Dell-IP storage solutions, provides a solid foundation for margin recovery. Dell Technologies’ focus on high-margin Dell-IP storage products, such as PowerStore and PowerMax, has already shown positive results, with double-digit growth in all-flash arrays for two consecutive quarters.

DELL is facing stiff competition in the AI infrastructure space against the likes of Hewlett-Packard HPE and Super Micro Computer SMCI.

Hewlett-Packard Enterprise is benefiting from a favorable mix shift to networking, stable gross margins across its largest business segments and disciplined pricing strategies. For the fourth quarter of fiscal 2025, Hewlett-Packard Enterprise’s non-GAAP gross margin expanded to 36.4%, up 550 bps year over year.

Super Micro Computer is evolving from just a server and hardware vendor into a full IT solutions provider. Products like DCBBS (Data Center Building Block Solutions) bundle hardware, software, cooling, networking, and support into complete systems. This strategy increases revenue per deal and improves margins. In the first-quarter fiscal 2026, Super Micro Computer reported that DCBBS is expected to carry more than 20% margins and become a major long-term profit contributor in its business.

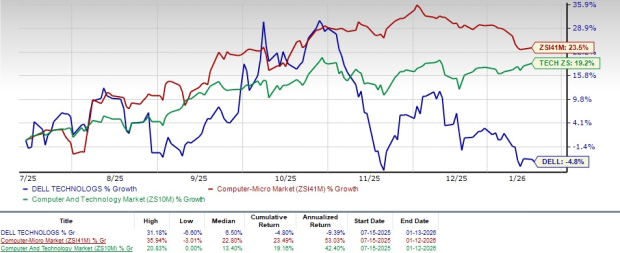

DELL’s shares have gained 4.8% in the trailing six-month period, underperforming the broader Zacks Computer & Technology sector’s return of 19.2% and the Zacks Computer - Micro Computers industry rise of 23.5%.

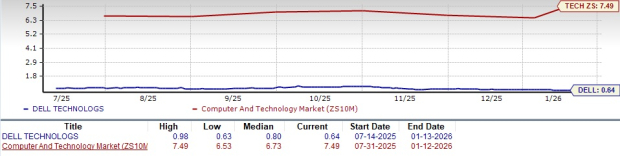

DELL shares are cheap, with a forward 12-month Price/Sales of 0.64X compared with the Computer & Technology sector’s 7.49X. DELL has a Value Score of A.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $9.89 per share, unchanged over the past 30 days. This suggests 21.50% year-over-year growth.

Dell Technologies Inc. price-consensus-chart | Dell Technologies Inc. Quote

DELL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite