|

|

|

|

|||||

|

|

|

The past six months have been a windfall for DigitalBridge’s shareholders. The company’s stock price has jumped 44.7%, hitting $15.31 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in DigitalBridge, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We’re glad investors have benefited from the price increase, but we're cautious about DigitalBridge. Here are three reasons we avoid DBRG and a stock we'd rather own.

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

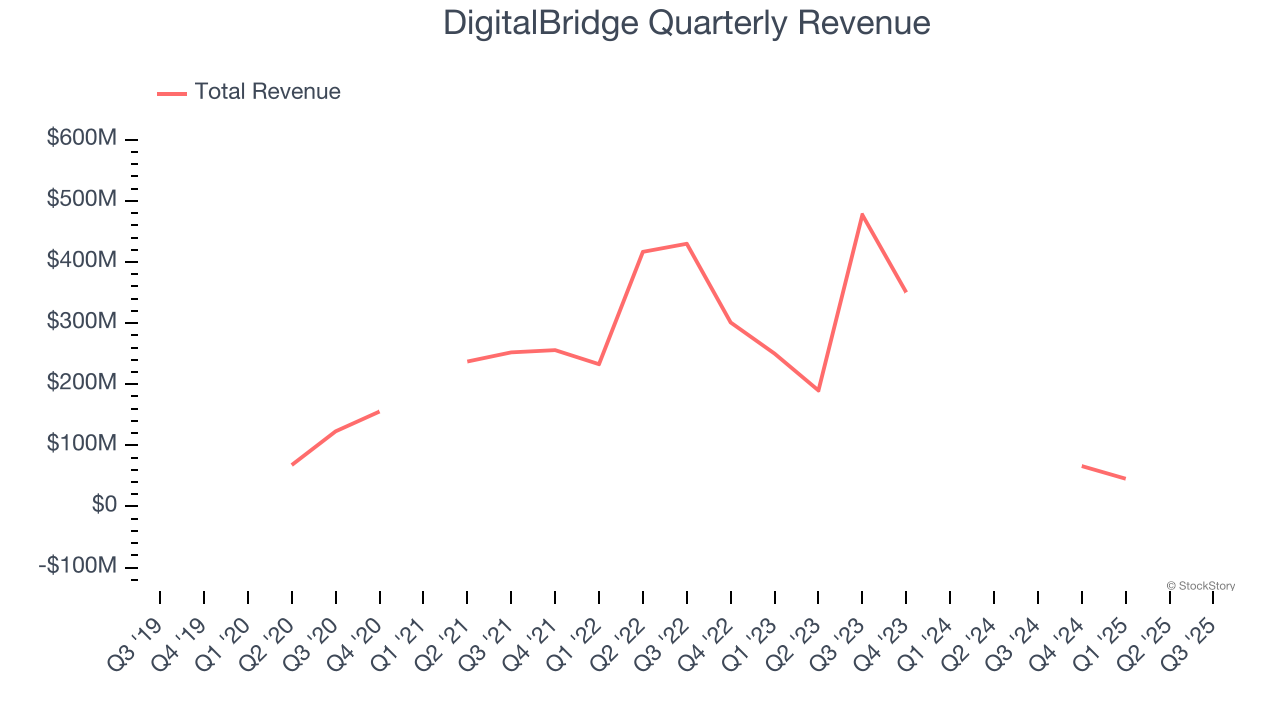

DigitalBridge’s demand was weak over the last five years as its revenue fell at a 37.5% annual rate. This was below our standards and is a sign of lacking business quality.

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, DigitalBridge has averaged an ROE of 1.4%, uninspiring for a company operating in a sector where the average shakes out around 10%.

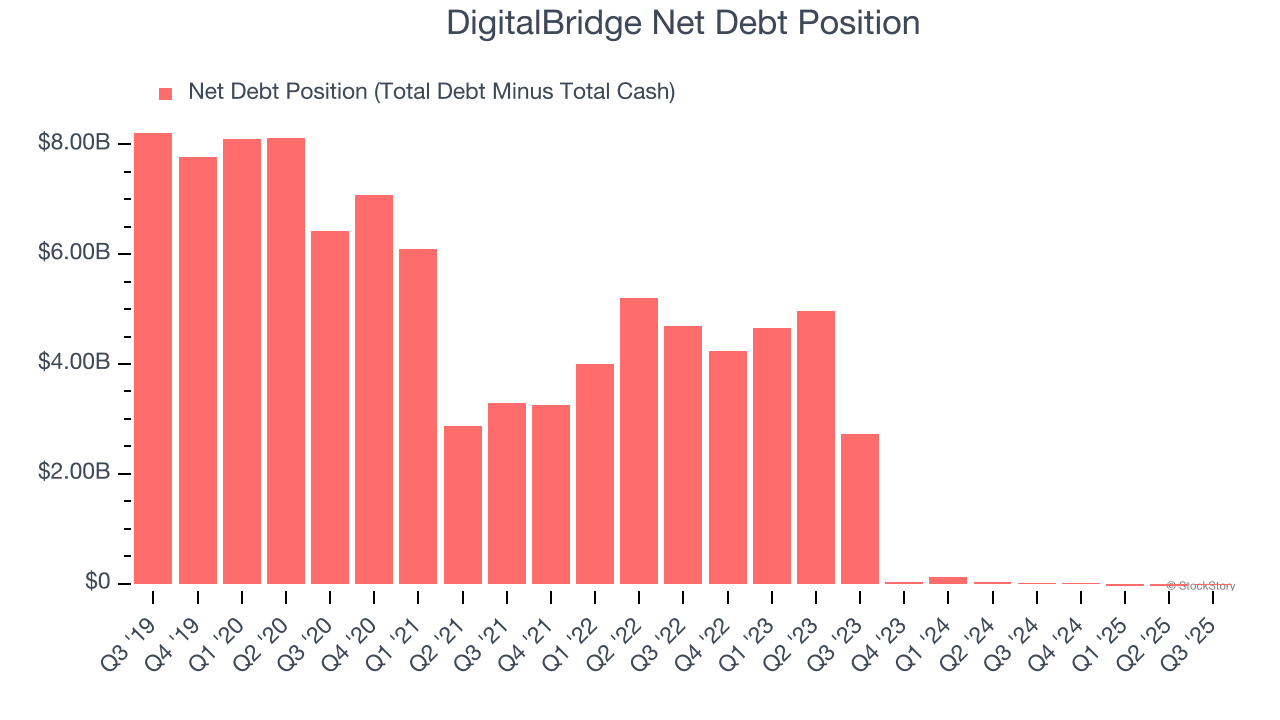

DigitalBridge reported $358.4 million of cash and $327.9 million of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With negative $18.6 million of EBITDA over the last 12 months, we view DigitalBridge’s 1.6× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

DigitalBridge isn’t a terrible business, but it doesn’t pass our bar. Following the recent surge, the stock trades at 2.3× forward P/E (or $15.31 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| 9 hours | |

| Jul-27 | |

| Jul-20 | |

| Jun-30 | |

| Jun-25 | |

| Jun-08 | |

| May-27 | |

| May-22 | |

| May-11 | |

| May-01 | |

| Apr-23 | |

| Apr-22 | |

| Apr-20 | |

| Apr-14 | |

| Apr-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite