|

|

|

|

|||||

|

|

|

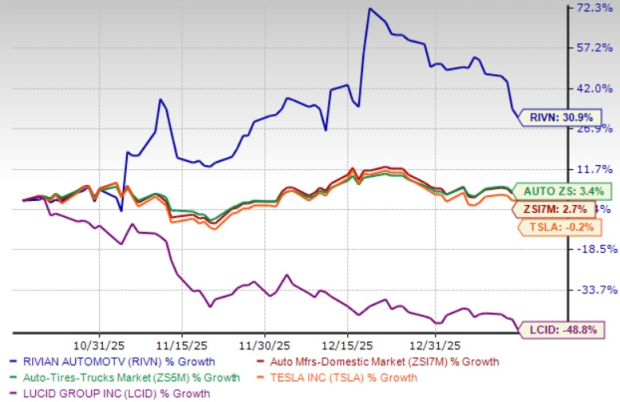

Shares of Rivian Automotive RIVN have climbed 30.9% in the past three months compared with the industry and sector’s growth of 2.7% and 3.4%, respectively. Its peers, Tesla TSLA and Lucid Group LCID, have lost 0.2% and 48.8%, respectively, over the same time frame.

Given Rivian’s impressive performance, investors might wonder if it is the right time to keep the stock in their portfolio. But a deep dive into the company's fundamentals suggests that the EV maker has a bumpy road ahead.

Rivian delivered 42,247 vehicles in 2025, down from 51,579 in 2024, while production totaled 42,284 units compared with 49,476 a year earlier. In the fourth quarter, the company produced 10,974 vehicles at its Normal, IL, plant and delivered 9,745 units.

For the full year, Tesla delivered over 1,635,000 vehicles in 2025 versus more than 1,789,000 units in 2024. Tesla reported deliveries of more than 418,000 vehicles in the fourth quarter of 2025 compared with over 495,000 units in the same period of 2024. Tesla’s production in the quarter totaled above 434,000 vehicles, down from 459,000 a year earlier.

Lucid, however, was an outlier. Lucid’s deliveries reached 15,841 units in 2025, up 55% year over year. Fourth-quarter deliveries of Lucid rose 31% sequentially to 5,345 units and exceeded the 3,099 units delivered in the year-ago quarter, resulting in an eight-quarter streak of new highs.

The broader auto industry has been grappling with slowing EV demand, partly due to the expiration of a $7,500 U.S. tax credit at the end of September, which pushed vehicle prices higher. For Rivian, which sells the premium-priced R1T pickup and R1S SUV, this backdrop has intensified questions around whether demand can hold up as production scales. The EV market is becoming increasingly crowded, with legacy automakers and new entrants fighting for market share. Rivian must differentiate itself while maintaining growth in a highly competitive environment to stay relevant.

Rivian’s cash balance declined to $7.1 billion at the end of the third quarter of 2025, down from $7.7 billion in 2024. In the fourth quarter, cash flow is likely to have remained under pressure due to two reasons. First, capital expenditures are likely to have risen due to the company’s plan on spending more cash on investments, while working capital trends that were favorable through the first three quarters are likely to have reversed.

Looking into 2026, working capital is expected to remain a use of cash as the company builds inventory for its R2 program. This inventory buildup is a deliberate move to support future production, but it does weigh on operating cash flow in the interim. Capital spending will also remain elevated in 2026. Beyond ongoing investments, additional capital will be required to begin vertical construction at the Georgia facility.

While Rivian’s vehicle manufacturing is entirely U.S.-based and most components are sourced from the U.S. or USMCA partners, the company remains vulnerable to global trade and economic disruptions. These factors could affect material costs, availability, and demand. Notably, LG battery cells for the R2 will initially be imported from Korea, potentially subject to tariffs, until U.S. production begins in Arizona by early 2027.

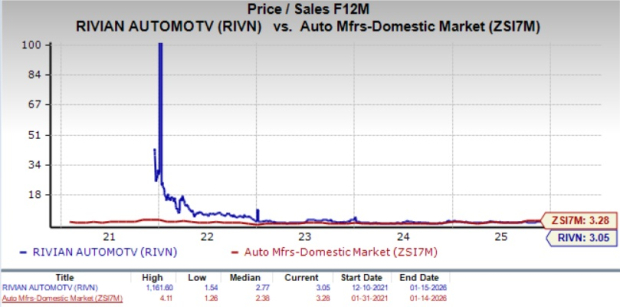

From a valuation perspective, Rivian appears undervalued. Based on its price/sales ratio, the company is trading at a forward sales multiple of 3.05, lower than the industry’s five-year average.

The Zacks Consensus Estimate for RIVN’s 2025 sales and EPS implies a year-over-year decline of 27.2% and 30.8%, respectively. Loss per share estimates for 2026 have widened by a penny in the past 30 days.

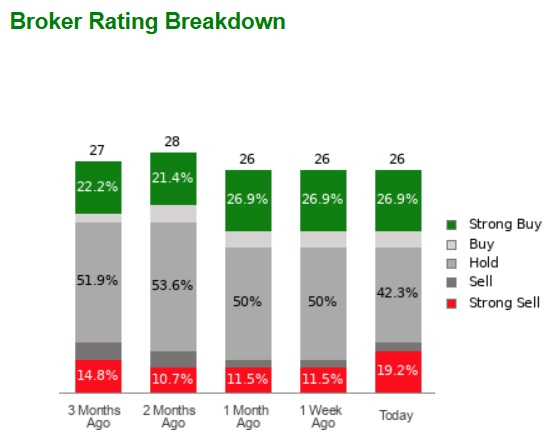

Rivian currently has an average brokerage recommendation of 2.78 on a scale of 1 to 5 (Strong Buy to Strong Sell), calculated based on the actual recommendations (Buy, Hold, Sell, etc.) made by 26 brokerage firms.

Despite strong share price performance, Rivian is facing slowing deliveries, softening EV demand and intensifying competition in a crowded market. At the same time, heavy capital expenditures, rising inventory levels for the R2 program and ongoing cash burn are likely to keep pressure on cash flows well into 2026.

External risks, including trade-related cost exposure and tariff uncertainties, add another layer of unpredictability. While the stock may look attractive on a valuation basis, declining sales and EPS estimates, along with a neutral-to-cautious broker consensus, suggest limited near-term upside.

Rivian’s recent stock rally appears to have outpaced the company’s underlying fundamentals, making this a prudent moment for investors to consider trimming or exiting their positions.

The stock currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 4 hours |

Tesla Autopilot under scrutiny after crash involving 49ers coach Kyle Shanahan

TSLA

Yahoo Finance Video

|

| 5 hours | |

| 5 hours | |

| 9 hours | |

| 11 hours | |

| 13 hours | |

| 14 hours | |

| 14 hours | |

| 15 hours | |

| 16 hours | |

| 20 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite