|

|

|

|

|||||

|

|

|

Aflac trades at $110.01 per share and has stayed right on track with the overall market, gaining 8.4% over the last six months. At the same time, the S&P 500 has returned 10.6%.

Is there a buying opportunity in Aflac, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We don't have much confidence in Aflac. Here are three reasons there are better opportunities than AFL and a stock we'd rather own.

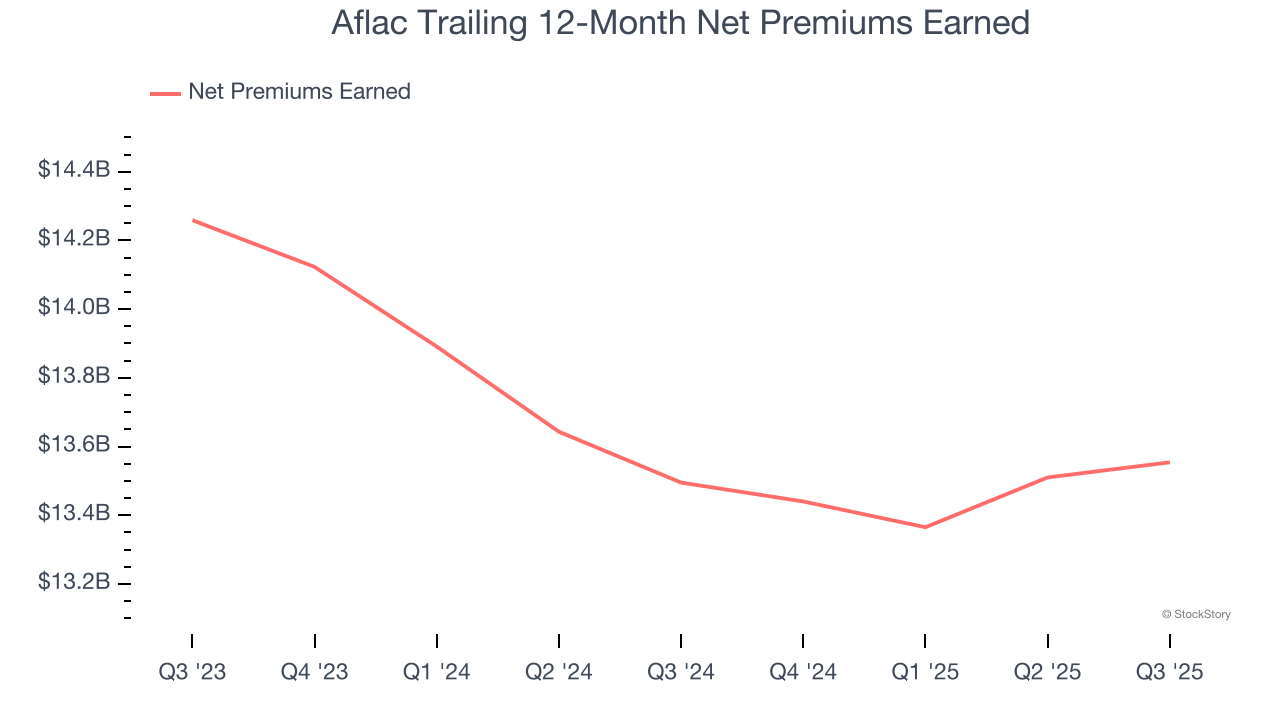

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

Aflac’s net premiums earned has declined by 6.2% annually over the last five years, much worse than the broader insurance industry. This shows that policy underwriting underperformed its other business lines.

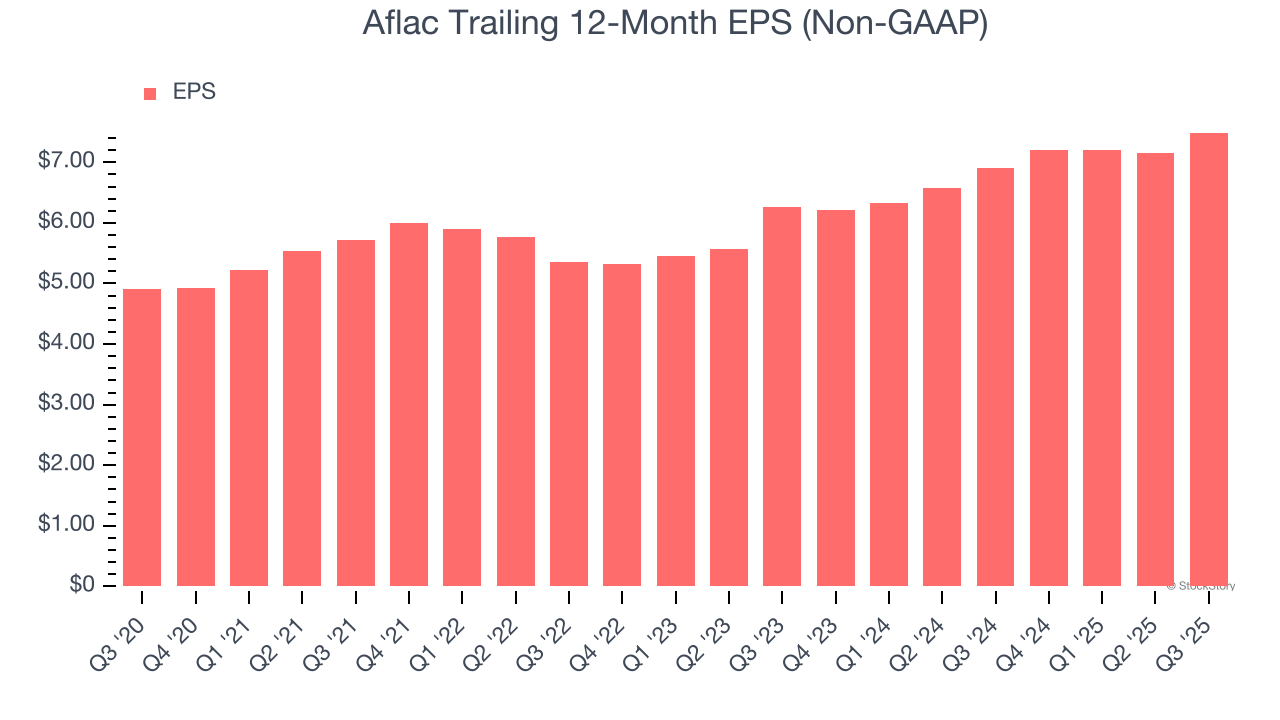

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Aflac’s EPS grew at an unimpressive 8.8% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 4.6% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

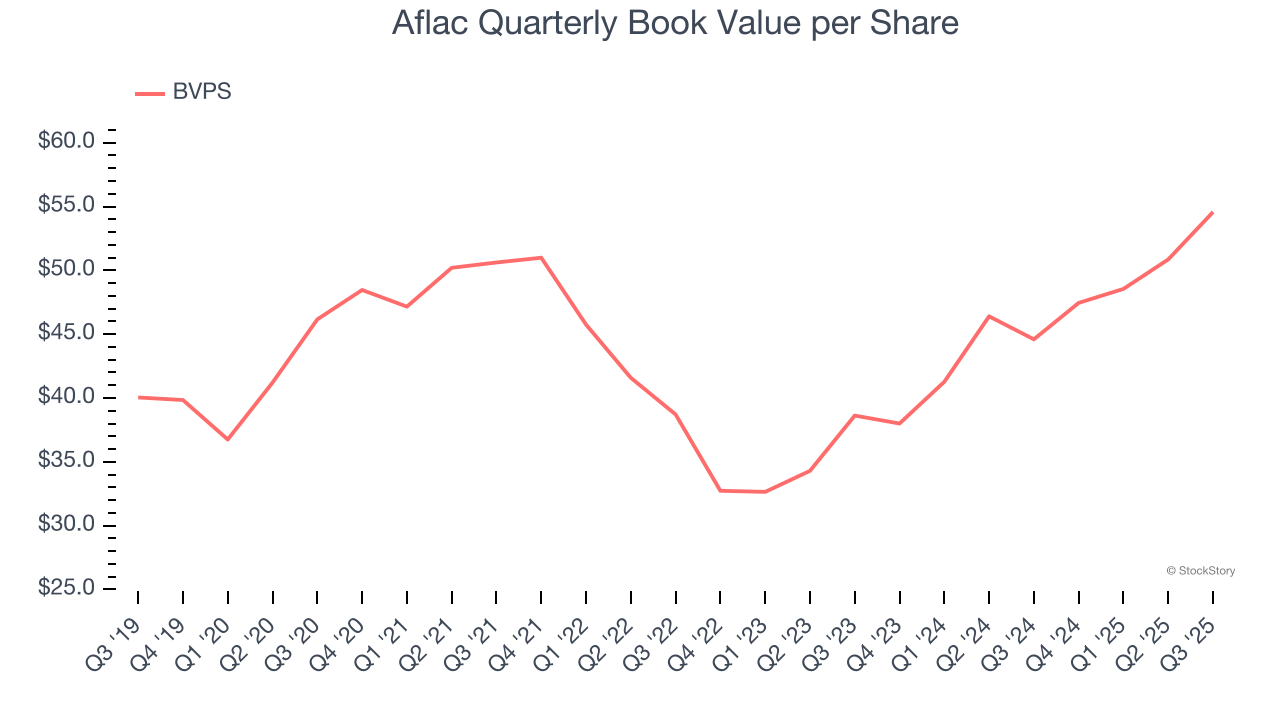

The key to book value per share (BVPS) growth is an insurer’s ability to earn underwriting profits while generating strong returns on its float - Warren Buffet’s secret sauce.

Over the next 12 months, Consensus estimates call for Aflac’s BVPS to remain flat at roughly $50.55, a disappointing projection.

Aflac’s business quality ultimately falls short of our standards. That said, the stock currently trades at 2× forward P/B (or $110.01 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jun-30 | |

| Jun-29 | |

| Jun-23 | |

| Jun-01 | |

| May-21 | |

| May-01 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-23 | |

| Apr-02 | |

| Mar-31 | |

| Mar-23 | |

| Mar-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite