|

|

|

|

|||||

|

|

|

Over the last six months, ZoomInfo’s shares have sunk to $9.02, producing a disappointing 14.4% loss - a stark contrast to the S&P 500’s 10.1% gain. This might have investors contemplating their next move.

Is now the time to buy ZoomInfo, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons there are better opportunities than GTM and a stock we'd rather own.

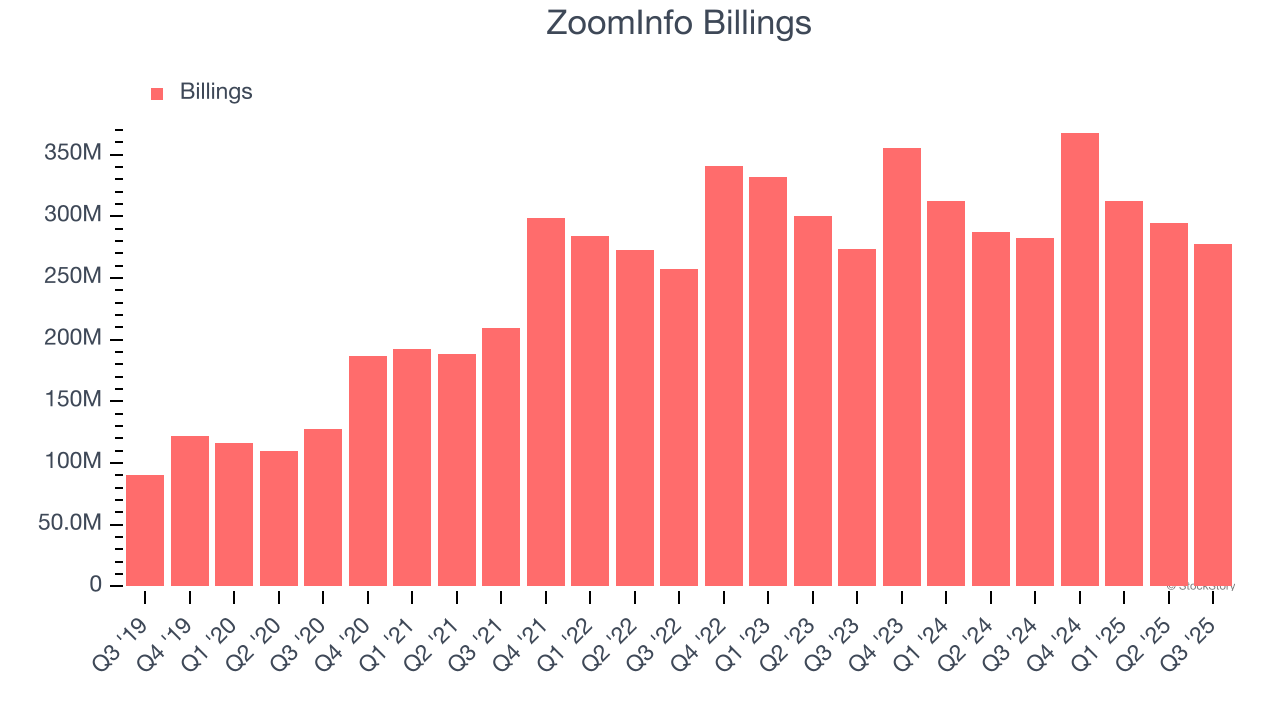

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

ZoomInfo’s billings came in at $277.6 million in Q3, and over the last four quarters, its year-on-year growth averaged 1%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect ZoomInfo’s revenue to stall, close to its 23.3% annualized growth for the past five years. This projection doesn't excite us and implies its newer products and services will not lead to better top-line performance yet.

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Analyzing the trend in its profitability, ZoomInfo’s operating margin rose by 5.1 percentage points over the last two years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 16.3%.

ZoomInfo doesn’t pass our quality test. After the recent drawdown, the stock trades at 2.5× forward price-to-sales (or $9.02 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite