|

|

|

|

|||||

|

|

|

Diebold Nixdorf has had an impressive run over the past six months as its shares have beaten the S&P 500 by 8.3%. The stock now trades at $69.92, marking a 18.4% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Diebold Nixdorf, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Despite the momentum, we're sitting this one out for now. Here are three reasons there are better opportunities than DBD and a stock we'd rather own.

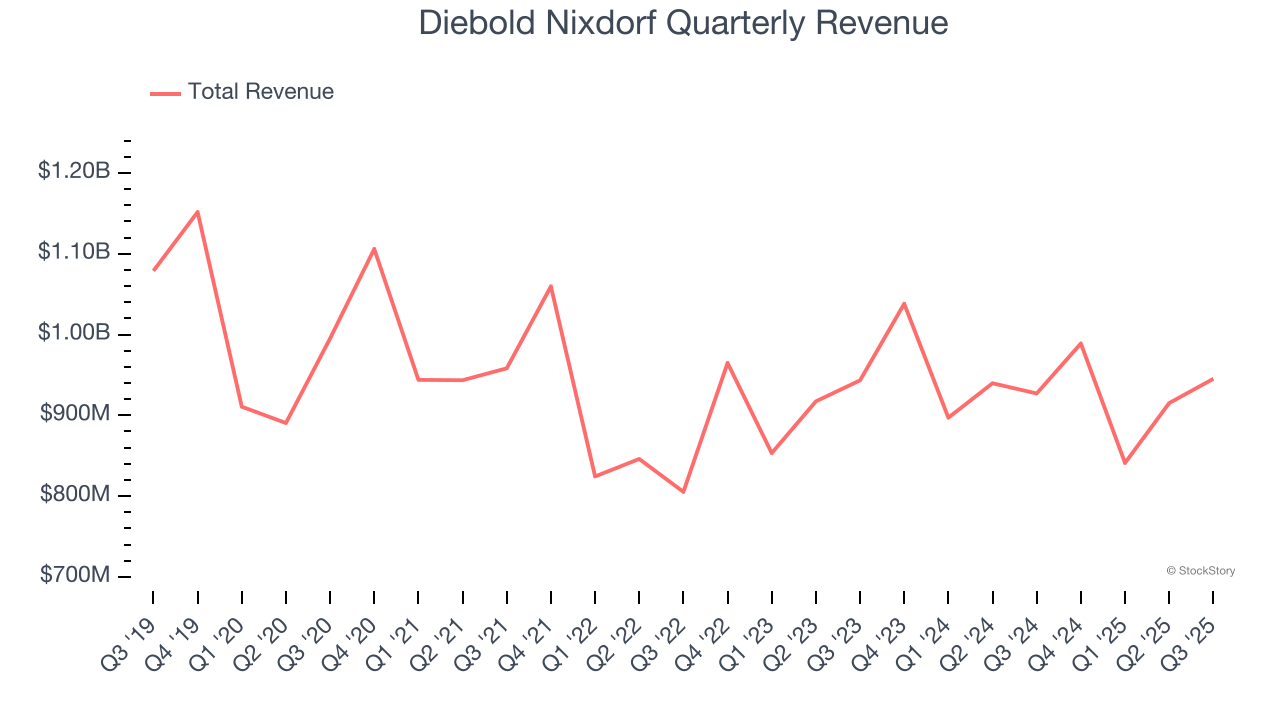

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Diebold Nixdorf’s demand was weak and its revenue declined by 1.3% per year. This was below our standards and signals it’s a lower quality business.

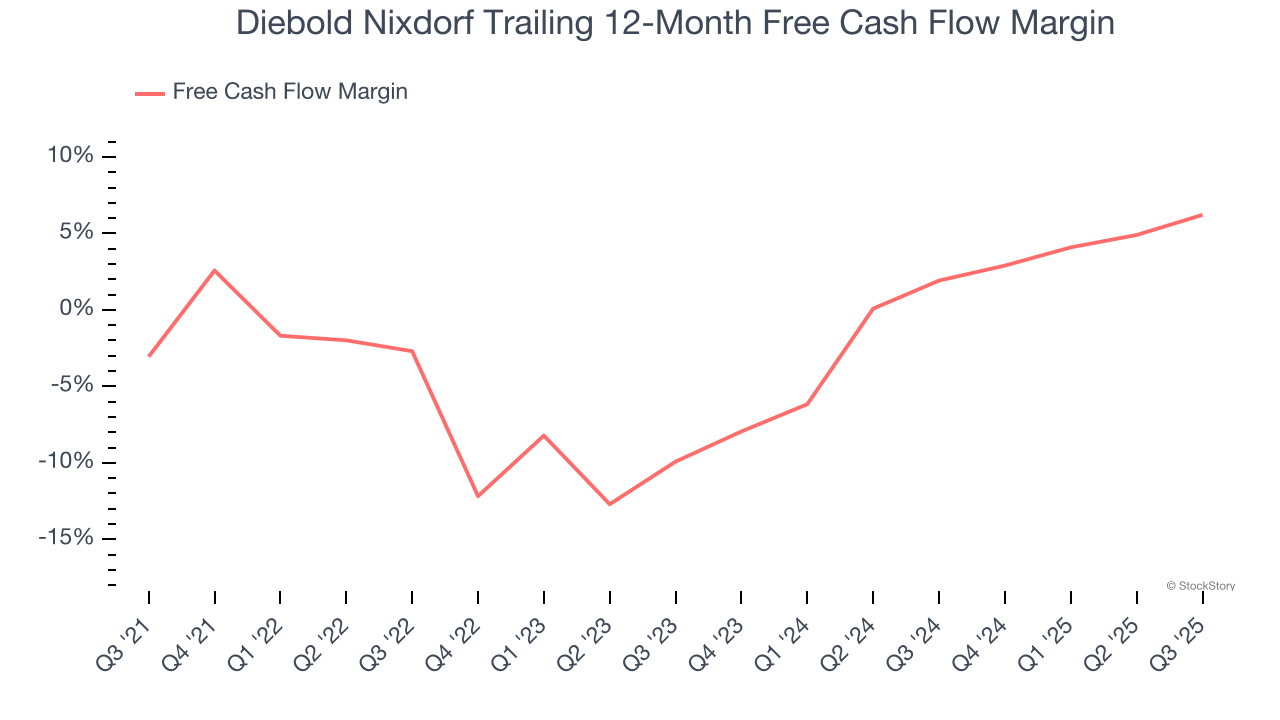

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Diebold Nixdorf posted positive free cash flow this quarter, the broader story hasn’t been so clean. Diebold Nixdorf’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.5%, meaning it lit $1.49 of cash on fire for every $100 in revenue.

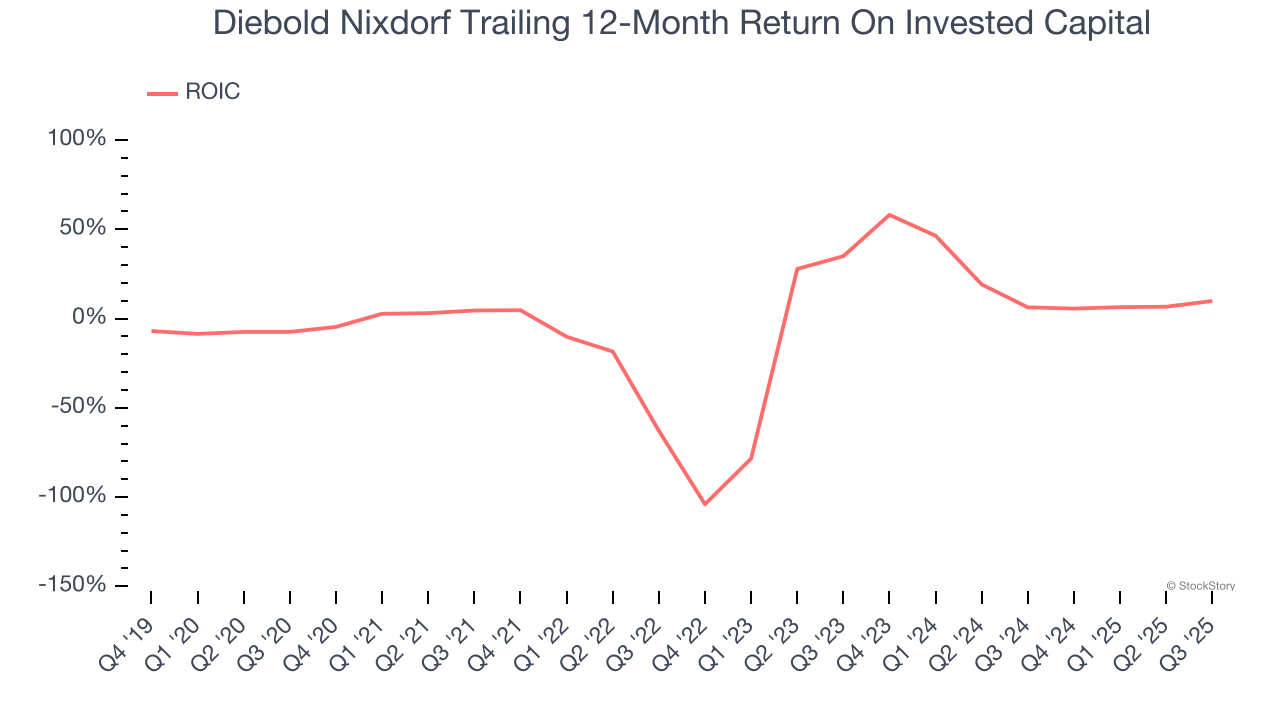

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Diebold Nixdorf’s five-year average ROIC was negative 1.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the business services sector.

Diebold Nixdorf isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 14.5× forward P/E (or $69.92 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. Let us point you toward the most entrenched endpoint security platform on the market.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-08 | |

| Jul-03 | |

| Jun-03 | |

| May-28 | |

| May-18 | |

| May-05 | |

| May-01 | |

| Apr-30 | |

| Apr-30 | |

| Apr-30 | |

| Apr-24 | |

| Apr-23 | |

| Apr-10 | |

| Apr-09 | |

| Apr-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite