|

|

|

|

|||||

|

|

|

Micron Technology's stock is cheap due to its cyclical nature.

Demand for memory is at an all-time high.

Production capacity to alleviate bottlenecks won't be online for a few years.

Finding dirt cheap stocks in the artificial intelligence (AI) world isn't an easy task. Most stocks have a bit of a premium valuation in anticipation of what could be developed down the road. However, there's one notable exception that appears to be incredibly cheap and that investors could take advantage of before it skyrockets.

Micron Technology (NASDAQ: MU) is a key provider of memory chips. Memory is a bit more cyclical than logic chips, but we're seeing a huge demand for memory that is expected to explode over the next few years. As a result, it could be the perfect time to buy this dirt cheap stock before it soars.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

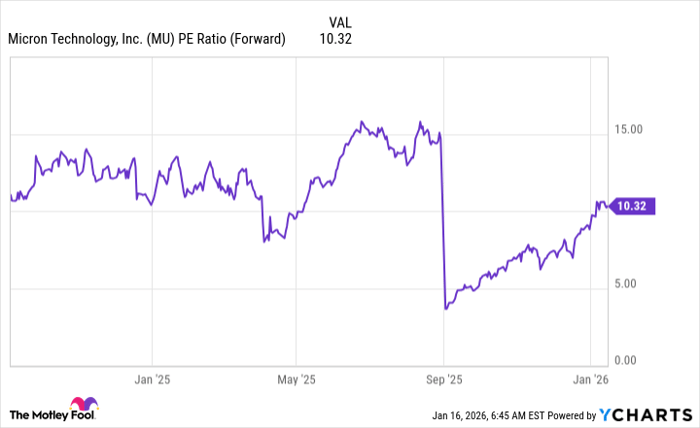

First, let's define how cheap Micron is. Most big tech companies trade for about 30 times forward earnings in today's market environment. There are also more exposed companies like Nvidia that have a higher valuation due to higher growth rates. However, Micron is far cheaper than any of those, and trades for a mere 10 times forward earnings.

MU PE Ratio (Forward) data by YCharts

Investors need to be careful here. Just because a stock is valued at a cheap level doesn't mean that it's actually cheap. Investors must pump the brakes and understand why Micron's stock is trading at a mere 10 times forward earnings, especially after it reported strong revenue growth over the past two years.

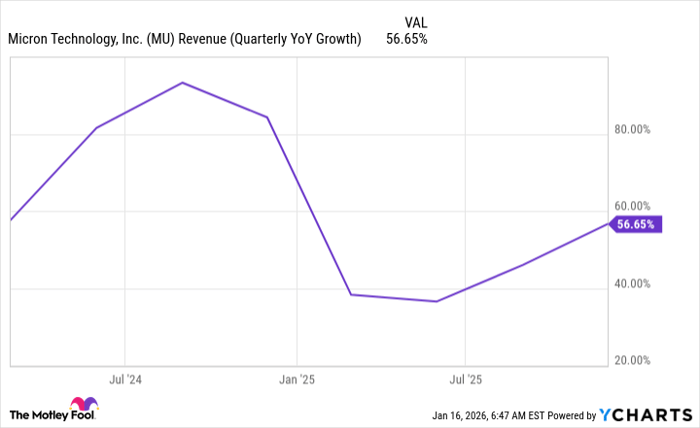

MU Revenue (Quarterly YoY Growth) data by YCharts

Furthermore, that growth rate isn't expected to slow down anytime soon. Wall Street analysts expect 133% growth during its next quarter, and 100% growth for fiscal year 2026 overall. Those are monster growth figures, so why is Micron's stock so cheap?

It all has to do with the cyclical nature of memory chips. Memory chips, unlike logic chips produced by companies like Taiwan Semiconductor Manufacturing, are fairly commoditized. There aren't really any massive technological innovations that set one company's product apart from another. Additionally, it costs a lot of money to construct fabrication facilities, so companies often overbuild capacity in preparation for the next demand wave. This creates excess capacity during periods when it isn't needed, causing memory prices to tank in cycles.

As a result, investors do not give a company like Micron a premium valuation because they know if they stick around for too long, they'll get burned. There's nothing different this time about memory technology or its cyclical nature. However, demand for memory is unlike anything we've ever seen, and it could provide a solid investment opportunity for 2026.

During its Q1 earnings report, Sumit Sadana, Micron's chief business officer, noted that the company is "more than sold out." This isn't expected to be alleviated anytime soon, as the market opportunity for its high-bandwidth memory (HBM) is expected to grow at a 40% compound annual growth rate (CAGR) to $100 billion by 2028. It's critical that Micron increases its production capacity to capitalize on this massive opportunity, but as of now, its production capacity is maxed out.

Several production facilities are under construction, and it is believed that its Idaho fab facility will have output starting in mid-2027. It's also starting construction on a second Idaho fab that should be operational by the end of 2028. Additionally, it is building another fabrication facility in New York that should be online in 2030.

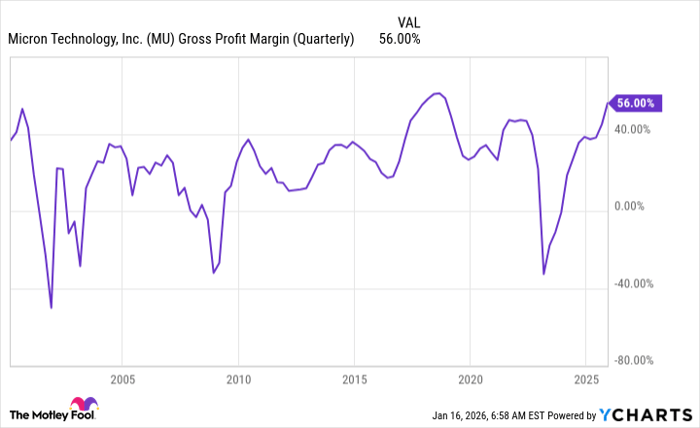

None of those facilities solves the production constraint problem that is showing up in 2026. As a result, memory prices could continue to soar, allowing Micron to profit from the shortage. Its gross margin is approaching recent highs, and if management's projections are correct, it will easily achieve record margins this year.

MU Gross Profit Margin (Quarterly) data by YCharts

For Q2, Micron expects its gross margin to be at an all-time high of 67%. This will supercharge Micron's earnings and allow its profitability to surge. I think this will cause Micron's stock to soar throughout 2026, as we're still years away from resolving the memory capacity crunch. Although Micron is cyclical, I think investors have an opportunity to scoop up one of the best investment AI opportunities in 2026.

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 19, 2026.

Keithen Drury has positions in Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Micron Technology. The Motley Fool has a disclosure policy.

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 7 hours | |

| 10 hours | |

| 10 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite