|

|

|

|

|||||

|

|

|

Wall Street analysts think Palantir and Intel will experience slumps this year.

Palantir would need consistent, near-perfect performances to come close to justifying its valuation.

Intel still hasn't made meaningful improvements to its chip manufacturing business.

Palantir Technologies (NASDAQ: PLTR) and Intel (NASDAQ: INTC) both had impressive returns in 2025, finishing the year up 145% and 84%, respectively. These were some of the highest returns from S&P 500 companies. Unfortunately, some Wall Street analysts think the party will be ending soon for these stocks.

How their stocks continue to perform remains to be seen, but if they drop to the projected targets, it would spell bad news for current investors. Let's take a look at a couple of high-level reasons why it could happen.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Palantir.

Palantir develops artificial intelligence (AI) software that helps governments, institutions, and businesses organize and analyze vast amounts of data. What started with software used only by governments has developed into a budding commercial business. Palantir's U.S. commercial segment has been its fastest-growing business in recent quarters.

Business performance aside, an analyst at RBC Capital has set Palantir's share price target at $50, a 70% drop from its latest closing price of nearly $171.

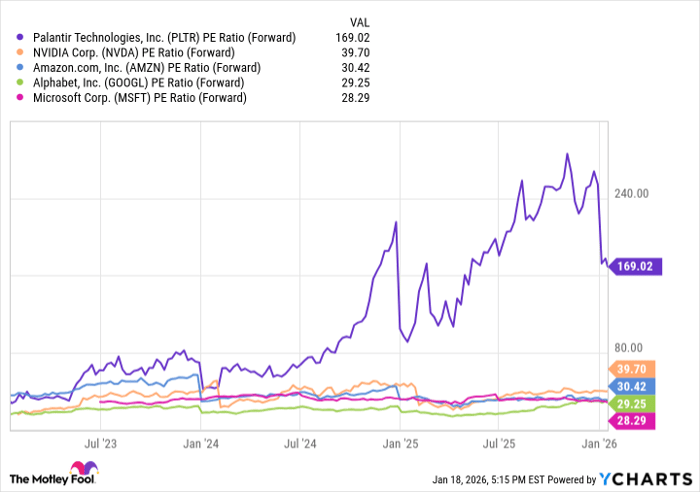

Much of the skepticism surrounding Palantir's stock comes from its valuation. It's currently trading at 169 times its projected earnings for the next year (as of Jan. 20), which is extremely expensive by virtually all standards. It's noticeably higher than the valuation of even some of the world's fastest-growing tech giants.

For Palantir to even remotely justify its valuation (and I do mean remotely), it would need to maintain triple-digit percentage growth for many years. And that's very unlikely to happen.

Data by YCharts.

Intel's 2025 stock performance was a much-needed turnaround from its 2024 performance. It seems investors took a liking to the increased demand for its central processing units, which help power data centers crucial to the current AI boom.

This demand didn't stop an analyst at Morgan Stanley from setting Intel's bear-case share price target at $19, a 60% decline from its latest price around $47 per share.

One problem with Intel is that it hasn't made much meaningful progress in getting its chip manufacturing business anywhere close to industry leader Taiwan Semiconductor Manufacturing. With Intel's delays, unexpected increased costs, and lower yields (the percentage of chips that work as intended), major companies would rather go to TSMC because of its efficiency and proven track record.

If Intel wants sustained success, it will need to improve its manufacturing technology and become No. 2 in the industry. It won't catch up to TSMC's scale, but it should try to compete on the same level as Samsung. So far, though, it hasn't shown signs of making that happen.

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 20, 2026.

Stefon Walters has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Intel, Palantir Technologies, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| 10 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite