|

|

|

|

|||||

|

|

|

This stock is trading near its lowest valuation in a year.

The company has put the focus on AI and is aggressively investing in that area.

"The Magnificent Seven" first grabbed attention as a Western back in 1960. But in recent times, the words describe a group of tech stocks that have wowed investors year after year. They are innovators, many are heavily involved in the hot growth area of artificial intelligence (AI), and they've proven their ability to generate earnings growth over time.

Many of these companies have become household names, as they offer products and services most of us use on a daily basis. And their strengths have translated into stock market performance. The Magnificent Seven stocks have powered the S&P 500 higher over the past few years, and this positive momentum may not be over.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Now, considering these gains, you might imagine that each of these players boasts a high valuation. But some actually are trading at reasonable levels right now, and one in particular looks dirt cheap -- is this player, the cheapest of the Magnificent Seven, a buy for 2026? Let's find out.

Image source: Getty Images.

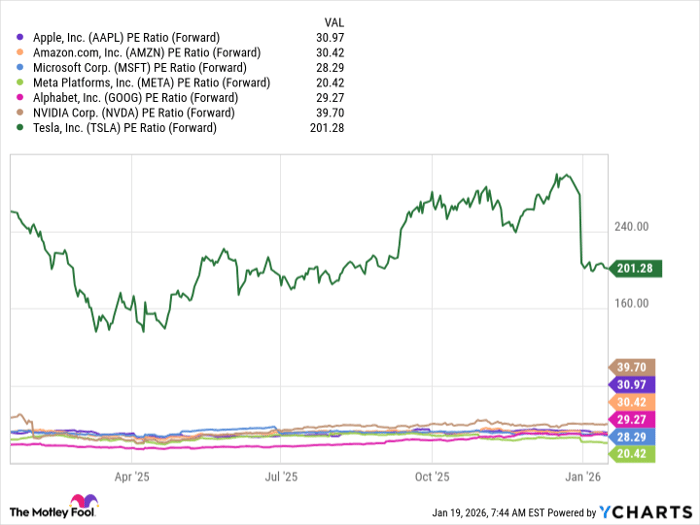

So, first, let's take a look at the Magnificent Seven players and their valuations. As the chart below shows, Meta Platforms (NASDAQ: META) stands out, trading for only 20x forward earnings estimates, while fellow Magnificent Seven players trade for at least 28x estimates and in some cases much higher.

AAPL PE Ratio (Forward) data by YCharts

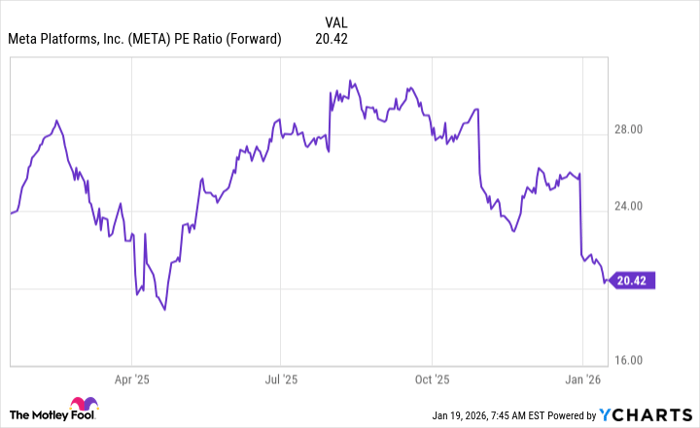

And a closer look at Meta shows that it's trading near its lowest valuation in a year.

META PE Ratio (Forward) data by YCharts

Now, let's consider Meta's AI story and what may lie ahead in 2026. You probably know Meta best for its social media apps, as they're world-famous -- about 3.5 billion people use at least one of these every day. I'm talking about Facebook, Messenger, Instagram, and WhatsApp. This platform generates revenue for Meta thanks to advertising. Advertisers turn to Meta to advertise on these apps because they know they can easily reach their target audience there.

This business model has been successful for Meta, allowing earnings to rise over the long term, and this financial strength has given Meta the power to invest in growth and offer investors passive income -- it launched its dividend in 2024.

So, where does AI fit into the picture? A few years ago, Meta recognized the potential of AI to spur growth and decided to go all in on this new technology. The company has been steadily increasing spending on AI, building out its own data centers, and developing and updating its large language model. And the tech giant has taken things one step further with the creation of Meta Superintelligence Labs, a division focused on the development of AI. To power this, the company went on a talent hiring spree last year and hired Alexandr Wang, who founded Scale AI when he was a student at MIT, to lead this new division.

Though Meta could benefit from AI in many ways, one clear win may be scored in the area of advertising. The company aims to completely automate advertising by the end of 2026, The Wall Street Journal reported last year. This would make the process faster and easier for advertisers, and importantly, generate better results. The idea is that AI not only could streamline and manage the actual advertising process, but AI features also may better design and target ads.

Considering that advertising drives Meta's revenue growth, a victory here could be big. Of course, success won't happen overnight, and as mentioned, the effort requires major spending -- these elements have weighed on the stock in recent months. And investors also have worried that Meta's aggressive infrastructure buildout may leave the company with too much capacity if there's any slowdown in the AI story.

Meta chief Mark Zuckerberg addressed those concerns in a recent earnings call, saying demand for compute remains high -- and in the worst-case scenario, Meta could slow its buildout and grow into existing infrastructure.

Today, considering Meta's reasonable valuation and all of the points I've mentioned above, the stock looks like a buy. And a potential rollout of AI advancements in advertising also could be a catalyst for revenue and stock price growth in 2026 or beyond.

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 21, 2026.

Adria Cimino has positions in Amazon and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 10 min | |

| 16 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite