|

|

|

|

|||||

|

|

|

Over the past six months, Semrush has been a great trade, beating the S&P 500 by 21.4%. Its stock price has climbed to $11.91, representing a healthy 31.4% increase. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Semrush, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We’re glad investors have benefited from the price increase, but we don't have much confidence in Semrush. Here are three reasons why SEMR doesn't excite us and a stock we'd rather own.

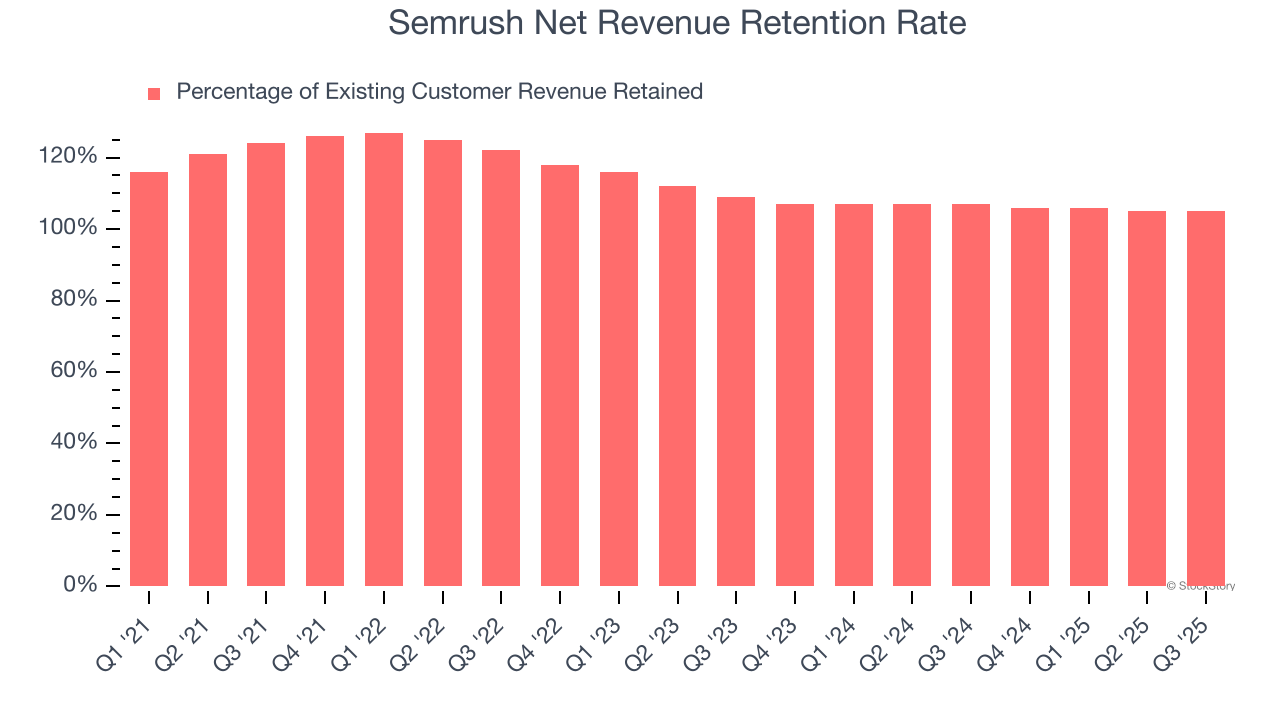

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Semrush’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 106% in Q3. This means Semrush would’ve grown its revenue by 5.5% even if it didn’t win any new customers over the last 12 months.

Semrush has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

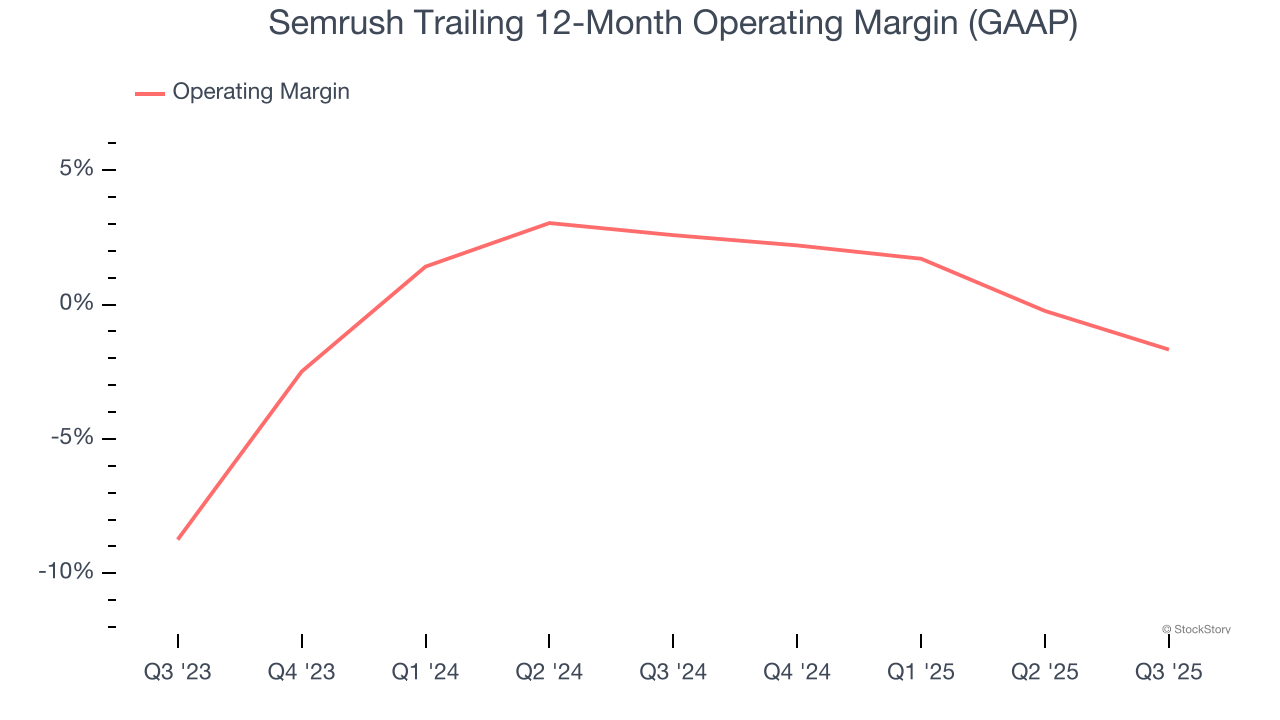

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Analyzing the trend in its profitability, Semrush’s operating margin decreased by 4.3 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Semrush’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 1.7%.

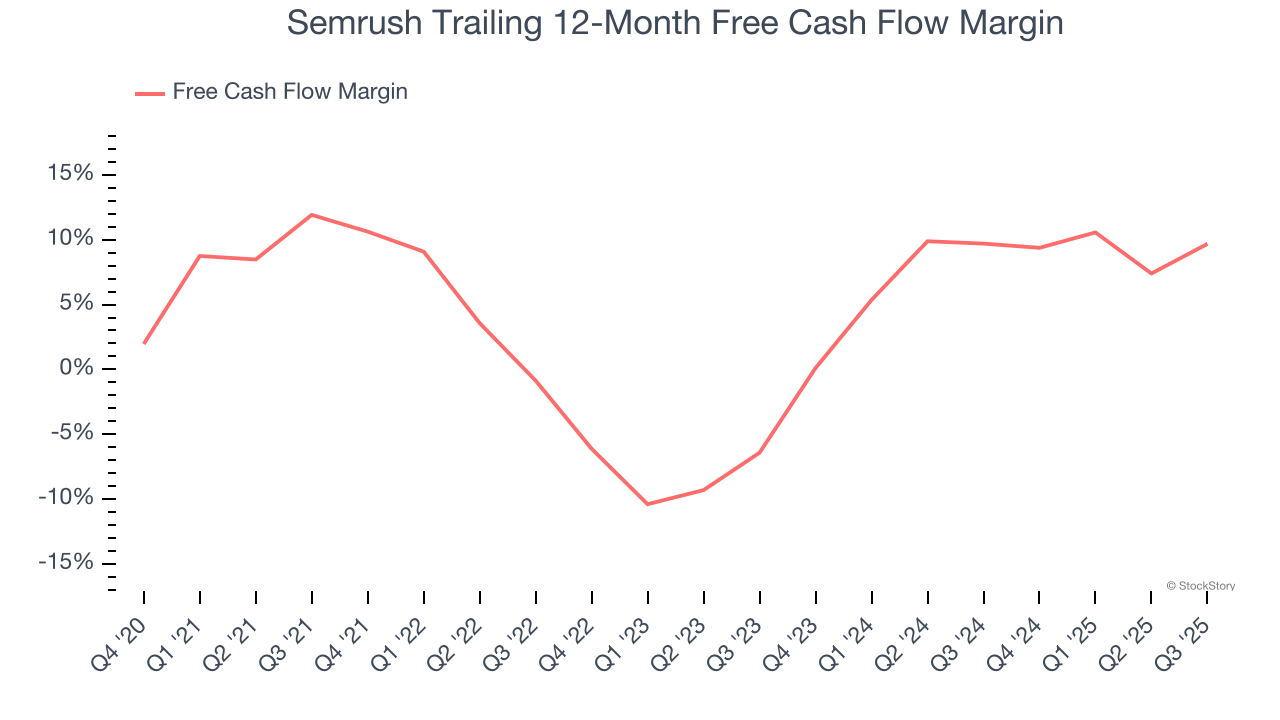

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Semrush has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.7%, subpar for a software business.

Semrush isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 3.6× forward price-to-sales (or $11.91 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. We’d suggest looking at one of our top digital advertising picks.

Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Apr-20 | |

| Mar-12 | |

| Mar-12 | |

| Mar-10 | |

| Mar-04 | |

| Mar-02 | |

| Mar-02 | |

| Mar-01 |

3 Cash-Heavy Stocks We Steer Clear Of

StockStory

|

| Feb-25 | |

| Feb-08 |

3 Stocks Under $50 with Warning Signs

StockStory

|

| Feb-06 | |

| Feb-03 | |

| Feb-03 | |

| Jan-29 |

Adobe Acquired Semrush Holdings (SEMR) at a 78% premium

Insider Monkey

|

| Jan-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite