|

|

|

|

|||||

|

|

|

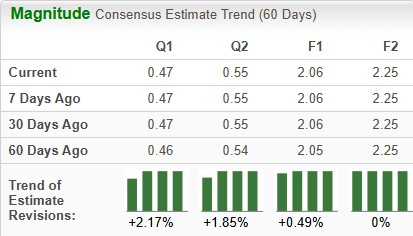

AT&T Inc. T is scheduled to report fourth-quarter 2025 earnings on Jan. 28, before the opening bell. The Zacks Consensus Estimate for revenues and earnings is pegged at $32.75 billion and 47 cents per share, respectively. The earnings estimate for AT&T for 2025 has increased 0.49% to $2.06 per share over the past 60 days, while the same for 2026 has remained unchanged at $2.25 per share.

The communications service provider delivered a four-quarter earnings surprise of 3.66%, on average.

Our proven model does not conclusively predict an earnings beat for AT&T for the fourth quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

AT&T currently has an ESP of 0.00% and a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

During the quarter, AT&T has deployed mid-band spectrum from EchoStar at approximately 23,000 cell sites across the country. This is expected to significantly increase speed and capacity for customers in 5,300 cities across 48 states. The acquisition of EchoStar is a smart approach from AT&T, as it eliminates the requirement for capital-intensive construction of cell sites to boost network capacity.

The company is also collaborating with AST SpaceMobile to expand into the emerging satellite connectivity space. T has also activated its fourth satellite ground gateway, while AT&T had successfully launched Bluebird 6, the largest commercial communications array deployed in low earth orbit. These factors are expected to have boosted commercial prospects for the company.

However, it faces stiff competition in the U.S. telecom market from other major players, such as T-Mobile, US, Inc. TMUS and Verizon Communications, Inc. VZ. Despite efforts to expand into the broadband space, competition remains from Charter, Verizon and other emerging service providers. T-Mobile and Verizon, along with AT&T, cover more than 300 million people. In such a highly saturated market, it’s very challenging to retain customers and expand the user base. To enhance customer churn rate, AT&T often provides healthy discounts, freebies and cash credits. Such a strategy escalates the pressure on margin.

AT&T is expanding its portfolio outside of its legacy telecom framework to gain a competitive edge. It has been expanding into public safety space and healthcare. However, Verizon and T-Mobile are also solutions that cater to this domain in their product suite. This is intensifying the competition.

Over the past year, AT&T has gained 5.2% against the industry’s decline of 5.9%, outperforming peers like Verizon Communications and T-Mobile. Verizon has gained 0.8%, while T-Mobile has declined 16.5%.

From a valuation standpoint, AT&T appears to be trading relatively cheaper than the industry and below its mean. Going by the price/earnings ratio, the company shares currently trade at 10.35 forward earnings, lower than 11.11 for the industry and the stock’s mean of 12.56.

AT&T is set to be affected by declining trends in the Business Wireline market. Lower demand for legacy voice and data services, as customers shifted to more advanced IP-based offerings, is causing the decline.

As of Sept. 30, 2025, AT&T had $20.27 billion of cash and cash equivalents with long-term debt of $128.09 billion compared with respective tallies of $10.5 billion and $123.06 billion in the previous quarter. This indicates that although its short-term liquidity has improved, its long-term debt burden has increased significantly.

AT&T usually witnesses a lower level of new connections during holiday seasons. Management expects to see lower fiber net adds in the fourth quarter owing to this factor.

However, growing traction in the consumer wireline business is backed by healthy demand for fiber broadband. Collaboration with space-based connectivity provider ASTS will likely bring long-term benefits. By leveraging ASTS Satcom capabilities, T aims address the limitations of terrestrial network infrastructure. Such initiatives will likely boost T’s prospects in rural and remote regions.

Stiff competition in each of its served markets and high debt obligations are major concerns. The development of gateways for satellite connectivity is also driving up the costs. This will likely bring long-term benefits, but in the short run, it will put pressure on the margin. The company’s wireline division is struggling with persistent losses in access lines as a result of competitive pressure from voice-over-Internet protocol (VoIP) service providers. Owing to these factors, it is suggested to avoid investment in AT&T at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 23 min | |

| 23 min | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Elon Musk Wants Starlink To Take On T-Mobile, Verizon, AT&THere's Why That's Easier Said Than Done

TMUS T VZ

Benzinga Prediction Markets

|

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite