|

|

|

|

|||||

|

|

|

RTX Corporation RTX is slated to report fourth-quarter 2025 results on Jan. 27, 2026, before market open.

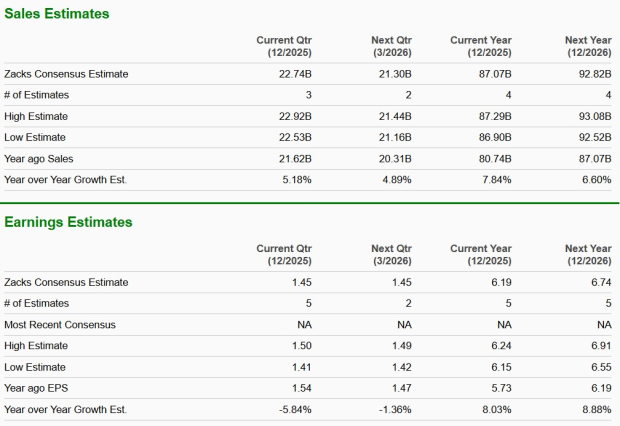

The Zacks Consensus Estimate for revenues is pegged at $22.74 billion, indicating an improvement of 5.2% from the year-ago quarter’s reported figure. The consensus mark for the bottom line is pegged at $1.45 per share, implying a decline of 5.8% from the prior-year quarter’s reported figure.

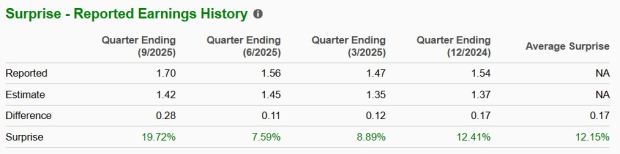

RTX’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 12.15%.

Our proven model does not conclusively predict an earnings beat for RTX this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is not the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

RTX has an Earnings ESP of 0.00% and a Zacks Rank of 3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Some stocks in the same industry that have the combination of factors indicating an earnings beat are Boeing BA and Northrop Grumman NOC. BA and NOC have an Earnings ESP of +16.73% and +0.54%, respectively. Both Boeing and Northrop Grumman carry a Zacks Rank of 3 at present.

Rising flight hours, supported by steady growth in both domestic and international air travel, continue to drive strong demand for commercial aircraft aftermarket services. This trend is likely to have supported RTX’s commercial aftermarket sales in the fourth quarter of 2025.

At the same time, increasing air passenger traffic is fueling demand for commercial jet engines, which is expected to have benefited RTX’s commercial original equipment manufacturer (OEM) sales. In this context, the upcoming quarterly results are likely to reflect healthy order activity, particularly for RTX’s geared turbofan (GTF) engines.

Overall, solid momentum across both commercial OEM and aftermarket channels is expected to have supported revenue growth in RTX’s Pratt & Whitney and Collins Aerospace segments during the reported quarter.

On the defense side, strong sales of military engines for key programs, including the F-35, are likely to have supported Pratt & Whitney’s top-line performance in the fourth quarter.

In addition, higher demand for RTX’s integrated air and missile defense systems, driven by rising global defense spending amid heightened geopolitical tensions, is expected to have boosted revenues at the Raytheon segment.

Higher tariff-related costs are likely to have offset some of the benefits from increased sales volume and improved operational performance across RTX’s three business segments, weighing on overall earnings.

RTX’s efforts to mitigate the impact of tariffs, including qualifying more components for military duty-free exemptions and increasing the use of free trade zones, are expected to have helped reduce this pressure. The impact of these measures is likely to be reflected in the upcoming quarterly results.

RTX’s shares have exhibited an upward trend, gaining a notable percentage over the past year. Specifically, the stock soared 57.9% in the time frame, outperforming the Zacks aerospace-defense industry’s growth of 30.4%. It has also outpaced the broader Zacks Aerospace sector’s return of 33.9% as well as the S&P 500’s gain of 14.1%.

Other industry players, such as Boeing and Northrop Grumman, have also delivered solid performance over the past year. However, their shares have risen by a comparatively smaller margin, gaining 42.4% and 30.9%, respectively, lagging RTX’s stronger share price performance.

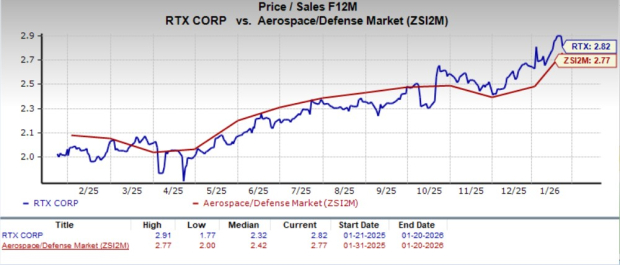

In terms of valuation, RTX’s forward 12-month price-to-sales (P/S) is 2.82X, a premium to its industry’s average of 2.77X. This suggests that investors will be paying a higher price than the company's expected sales growth compared with its industry’s P/S ratio.

However, its industry peers are currently trading at a discount compared with RTX. While the forward 12-month price/earnings multiple for Boeing is 1.99, the same for Northrop Grumman is 2.12.

RTX is well-positioned to benefit from long-term growth opportunities in both commercial aerospace and defense markets. A sustained recovery in global air travel, combined with strong defense demand from the US and allied nations, supports steady revenue growth and provides solid visibility through a healthy order backlog. The company’s diversified business model and strong free cash flow generation further strengthen its ability to invest in growth initiatives while continuing to return value to shareholders.

However, RTX faces near-term challenges that investors should monitor. Ongoing supply-chain constraints, tariff-related cost pressures and the risk of operational disruptions could weigh on margins and delay revenue realization despite healthy demand conditions. While management’s mitigation efforts are expected to help limit these impacts, their effectiveness will be an important factor in determining RTX’s earnings performance in the coming quarters.

RTX appears well-positioned ahead of its fourth-quarter earnings, supported by solid demand across its commercial aerospace and defense businesses, a strong backlog and healthy cash flow generation. However, with the stock having delivered significant gains over the past year and near-term pressures from tariffs, supply-chain constraints and cost dynamics still in play, a cautious approach may be warranted, making the stock more suitable for holding rather than taking new positions at this stage.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 39 min | |

| 41 min | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite