|

|

|

|

|||||

|

|

|

Paychex has gotten torched over the last six months - since July 2025, its stock price has dropped 25.9% to $107.19 per share. This might have investors contemplating their next move.

Is there a buying opportunity in Paychex, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons there are better opportunities than PAYX and a stock we'd rather own.

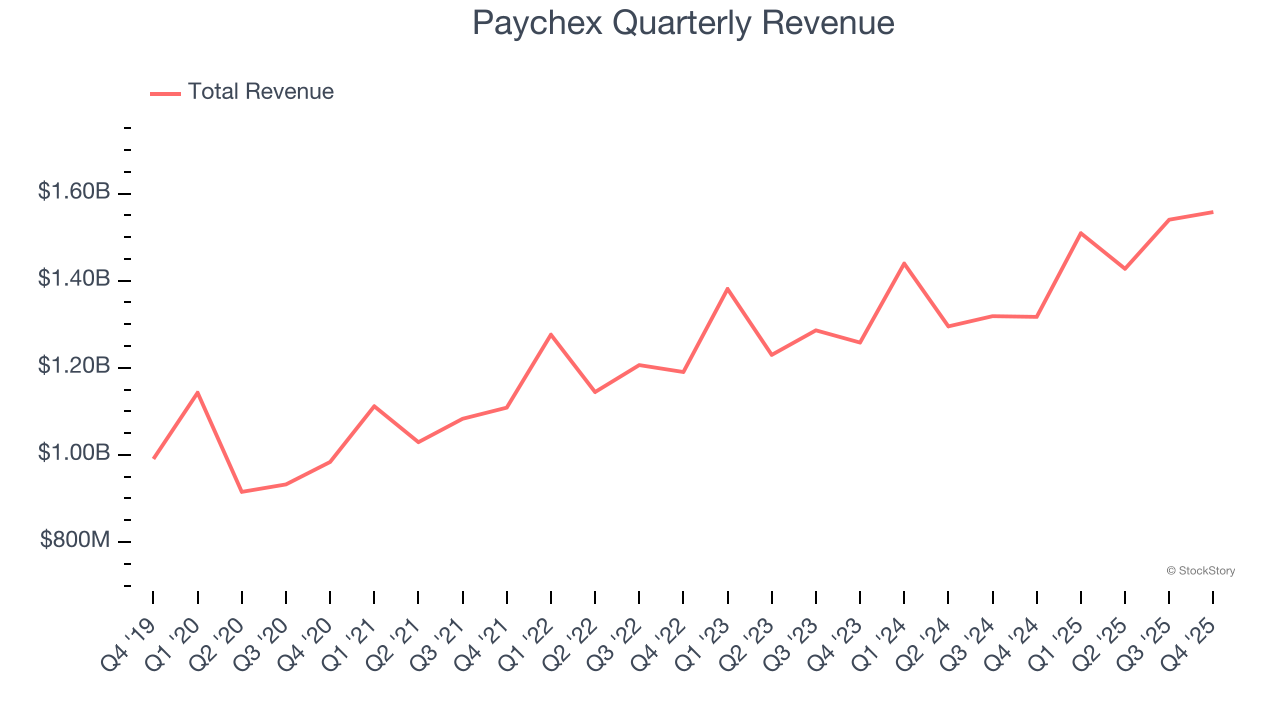

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Paychex’s sales grew at a sluggish 8.7% compounded annual growth rate over the last five years. This was below our standard for the software sector.

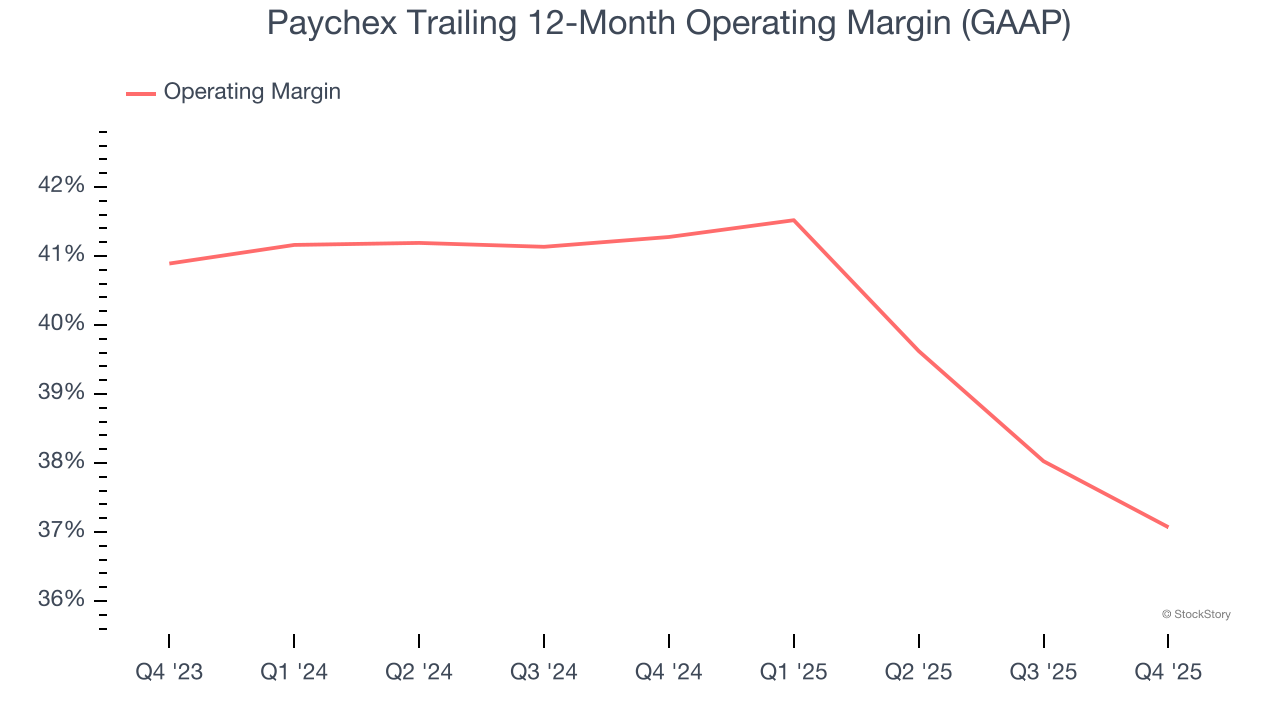

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Analyzing the trend in its profitability, Paychex’s operating margin decreased by 4.2 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 37.1%.

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Paychex’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 33.9% for the last 12 months will decrease to 31.1%.

Paychex isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 5.8× forward price-to-sales (or $107.19 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d suggest looking at the most entrenched endpoint security platform on the market.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-22 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-08 | |

| Jun-30 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-22 | |

| Jun-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite