|

|

|

|

|||||

|

|

|

What a time it’s been for Viatris. In the past six months alone, the company’s stock price has increased by a massive 41.5%, reaching $13.07 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Viatris, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re happy investors have made money, but we're swiping left on Viatris for now. Here are three reasons why VTRS doesn't excite us and a stock we'd rather own.

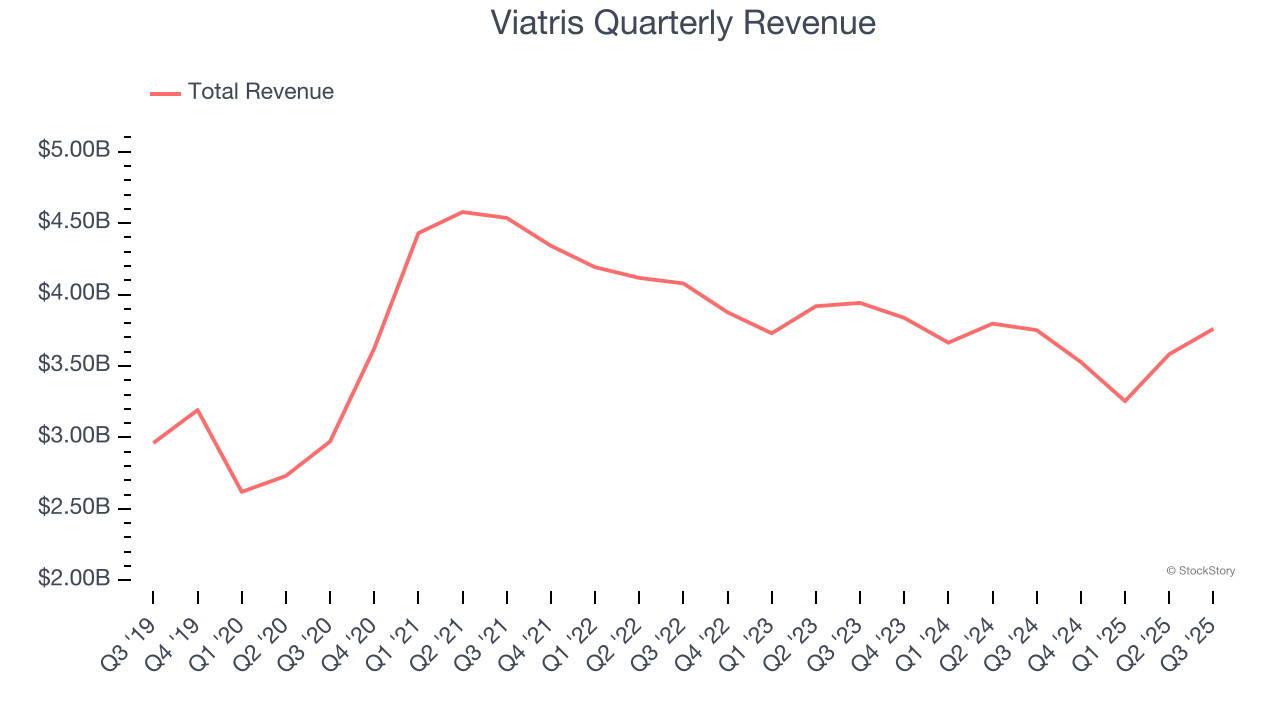

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Viatris’s sales grew at a mediocre 4.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector.

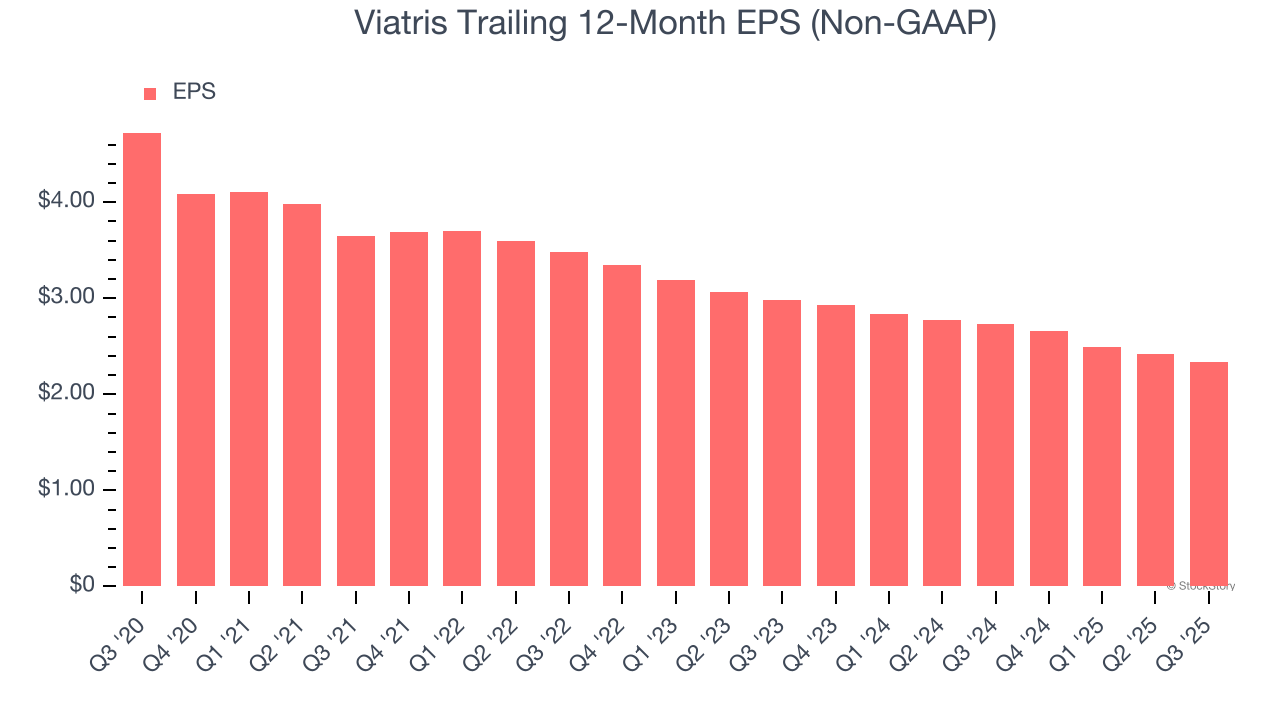

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Viatris, its EPS declined by 13.1% annually over the last five years while its revenue grew by 4.2%. This tells us the company became less profitable on a per-share basis as it expanded.

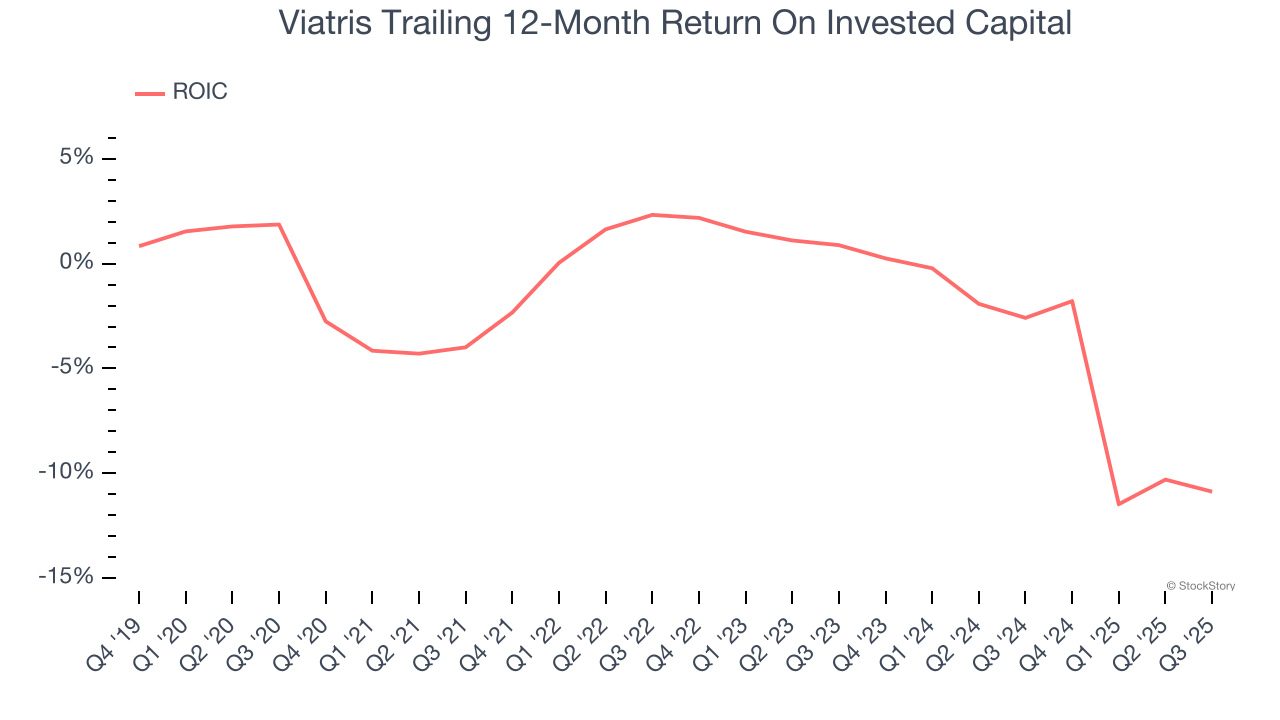

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Viatris’s five-year average ROIC was negative 2.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

Viatris falls short of our quality standards. After the recent rally, the stock trades at 5.3× forward P/E (or $13.07 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-29 | |

| Jul-22 | |

| Jul-01 | |

| Jun-29 | |

| May-18 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-05 | |

| May-05 | |

| May-04 | |

| Apr-13 | |

| Apr-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite