|

|

|

|

|||||

|

|

|

Snowflake SNOW is benefiting from its expansion of cloud infrastructure reach, which positions the company for significant growth and increased market share in the data and AI space. In the third quarter of fiscal 2026, Snowflake’s product revenue increased 29% year over year, reaching $1.16 billion, with remaining performance obligations totaling $7.88 billion, reflecting 37% year-over-year growth.

Snowflake’s collaboration with major cloud providers like AWS and Google Cloud has been a major growth driver. The company surpassed $2 billion in sales through AWS Marketplace in a single calendar year and received 14 AWS Partner awards, more than any other independent software vendor. The partnership with Google Cloud to integrate Gemini models into Snowflake’s AI offerings further enhances customer choice and access to advanced AI capabilities.

Snowflake’s focus on AI capabilities has also been a game-changer. The company achieved a $100 million AI revenue run rate one quarter earlier than anticipated, driven by the rapid adoption of Snowflake Intelligence and Cortex AI. These products enable customers to harness next-generation AI capabilities, transforming how businesses interact with their data and driving real-world impact. With AI influencing 50% of bookings signed in the third quarter of fiscal 2026 and 28% of all deployed use cases incorporating AI, Snowflake is solidifying its position as a leader in enterprise AI.

Snowflake’s expansion into cloud infrastructure, coupled with its focus on AI innovation and strategic partnerships, positions the company for sustained growth. For the fourth quarter of fiscal 2026, Snowflake expects product revenues in the range of $1.195-$1.2 billion. The projection range indicates year-over-year growth of 27%.

Snowflake faces stiff competition from the likes of Alphabet GOOGL and MongoDB MDB, which are also expanding their footprint in the cloud analytics space.

Alphabet is expanding its presence in the cloud analytics market with its cloud computing platform, Google Cloud’s BigQuery, a strong serverless data warehouse solution. Alphabet has been growing quickly in the booming cloud market. In third-quarter 2025, Google Cloud revenues increased 33.5% year over year to $15.16 billion.

MongoDB’s cloud database platform, Atlas, has shown strong performance, with year-over-year growth accelerating to 30% in the third quarter of fiscal 2026. Atlas now represents 75% of MongoDB’s total revenue, driven by new workloads and the expansion of existing workloads.

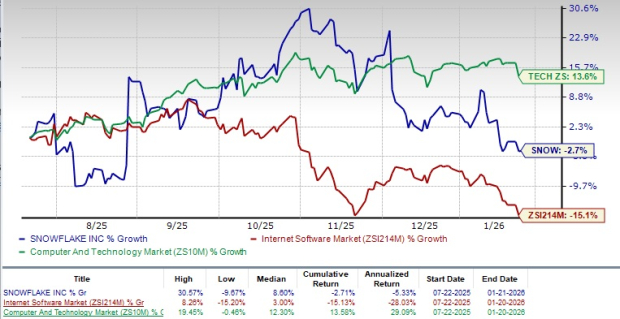

Snowflake shares have lost 2.7% in the trailing 12-month period, underperforming the broader Zacks Computer & Technology sector’s return of 13.6%. However, the company’s shares have outperformed the Zacks Internet Software industry’s decline of 15.1%.

Snowflake stock is trading at a premium, with a forward 12-month Price/Sales of 12.42X compared with the Internet Software industry’s 4.34X. SNOW has a Value score of F.

The Zacks Consensus Estimate for SNOW’s fiscal 2026 earnings is pegged at $1.20 per share, unchanged over the past 30 days. The figure indicates a 44.58% increase year over year.

Snowflake Inc. price-consensus-chart | Snowflake Inc. Quote

Snowflake currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite