|

|

|

|

|||||

|

|

|

Since July 2025, Westamerica Bancorporation has been in a holding pattern, posting a small return of 3.2% while floating around $51.15.

Is there a buying opportunity in Westamerica Bancorporation, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

We're sitting this one out for now. Here are three reasons you should be careful with WABC and a stock we'd rather own.

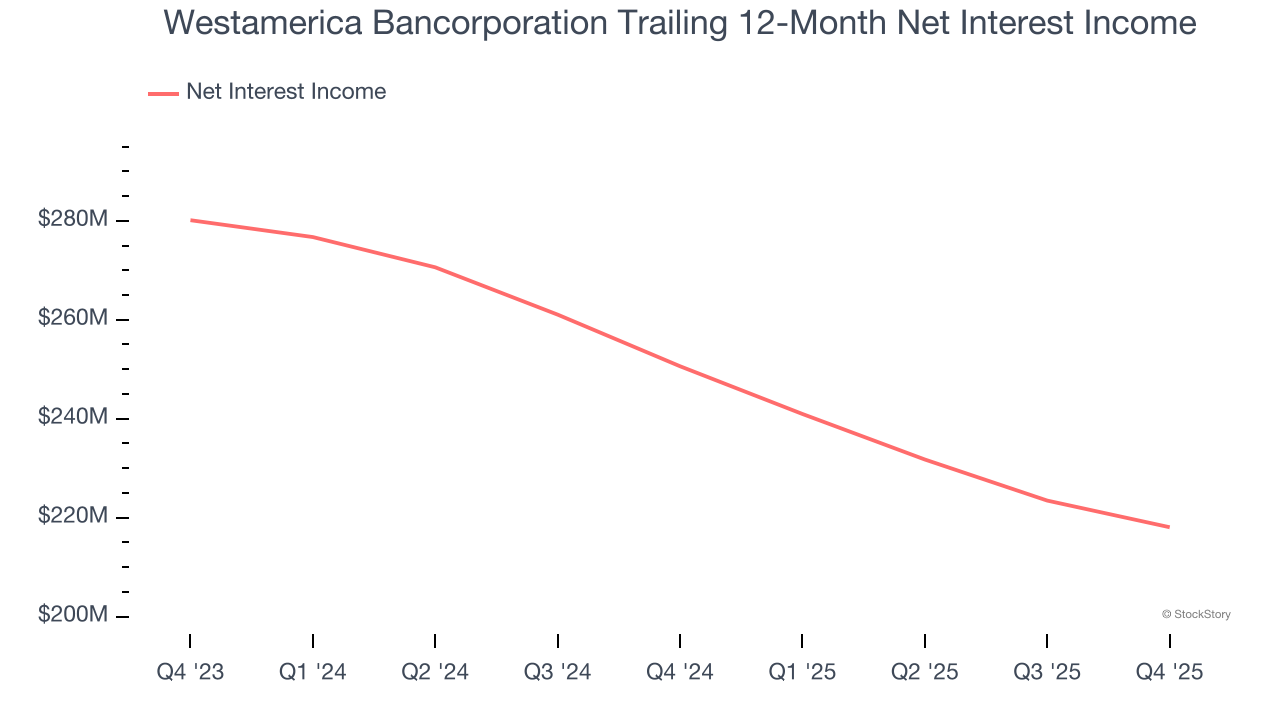

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Westamerica Bancorporation’s net interest income has grown at a 5.9% annualized rate over the last five years, worse than the broader banking industry.

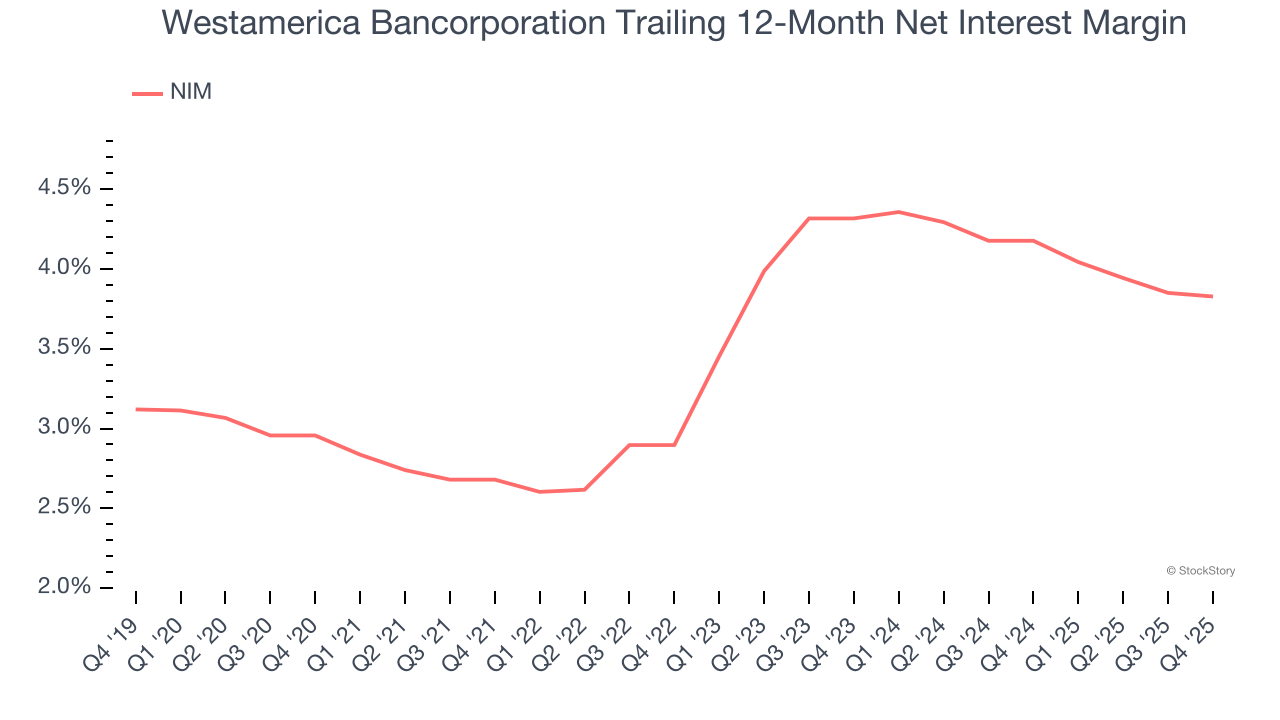

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Westamerica Bancorporation’s net interest margin averaged 4%. However, its margin contracted by 48.9 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Westamerica Bancorporation either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

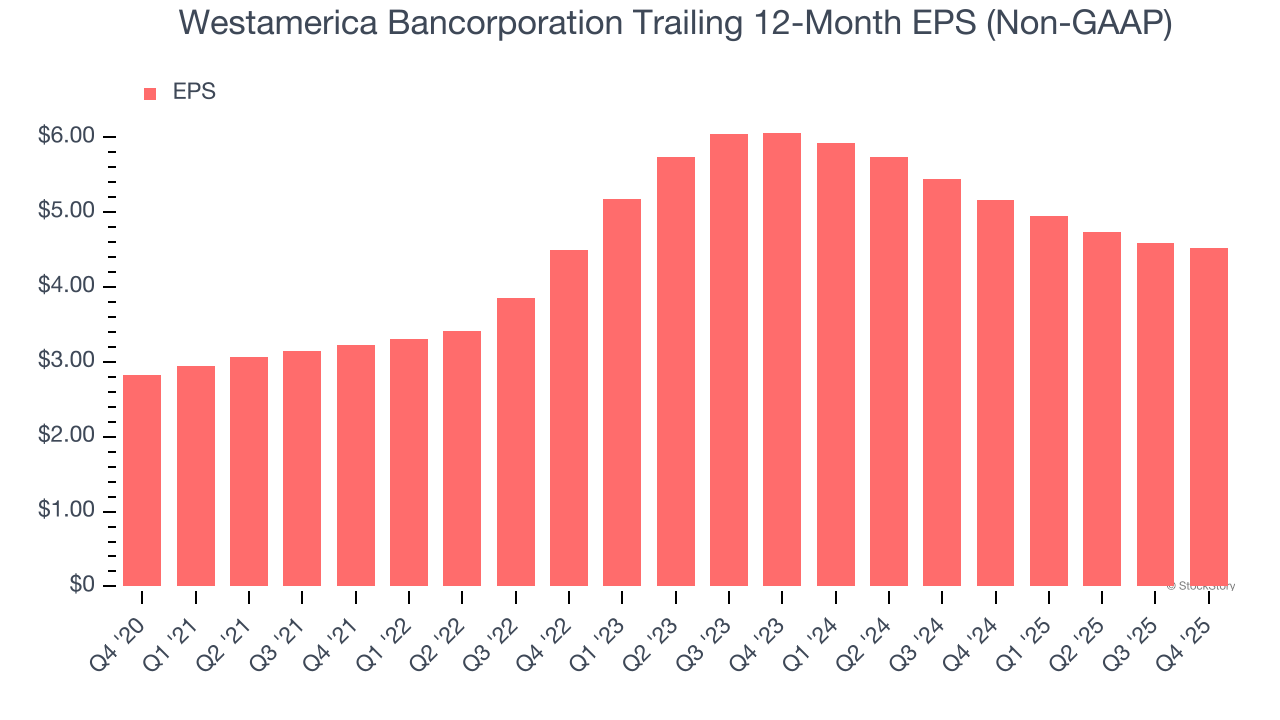

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Westamerica Bancorporation’s EPS grew at an unimpressive 9.8% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 4% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Westamerica Bancorporation doesn’t pass our quality test. That said, the stock currently trades at 1.3× forward P/B (or $51.15 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere. We’d recommend looking at one of our top software and edge computing picks.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Apr-24 | |

| Apr-23 | |

| Apr-16 | |

| Apr-16 | |

| Apr-14 | |

| Feb-22 | |

| Feb-02 | |

| Jan-22 | |

| Jan-21 | |

| Jan-15 | |

| Jan-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite