|

|

|

|

|||||

|

|

|

Micron Technology Inc (NASDAQ:MU) might be the hottest name in tech right now and, as a consequence, suffers from downside consternation. After all, MU stock is trading for sky-high multiples. On the technical side, MU is soaring well above key moving averages. In addition, multiple indicators are stretching the upper bounds of their parameters, all pointing to one conclusion: Micron is overheated.

The problem? MU stock is up 38% on a year-to-date basis and we haven't even finished January yet. It's almost as if the market doesn't care what the multiples and oscillators have to say. But then, what explains this extraordinary rally?

One of the common fundamental arguments for selling MU stock right now is that the underlying robust financial performance has been priced in. Analysts have been very encouraged with Micron's most recent earnings report, citing robust memory chip pricing, continued high-bandwidth memory (HBM) momentum and a multi-year supercycle in artificial intelligence and data-center spending as powerful catalysts. However, MU basically tripled in value in 2025. It was difficult to see how the security could move any higher.

What may be missing, though, is the broader context. In prior paradigms, it wasn't unusual to see memory pricing encounter sharp boom-bust cycles. Micron and its peers would routinely ramp up production and introduce supply to the market at the same time. This created a piston-like mechanism that led to wild fluctuations in pricing. Therefore, it's only natural that investors are skeptical about MU stock maintaining its current momentum.

However, AI has radically altered the paradigm by stabilizing demand upward. In other words, as much as there may be fears of a bubble in machine intelligence, institutions are throwing their full weight behind the innovation. That's why looking at past valuations may not be the most appropriate gauge of reality.

The fact of the matter may be that the broader sentiment regime has shifted — and we must look to contextual changes for insights.

From the perspective of first-order analyses, it's not difficult to sympathize with the skeptical argument against Micron stock. For example, looking at volatility skew — which shows implied volatility (IV) across different strike prices on the same expiration date — the readout identifies higher put premiums for strike prices south of the current spot price.

Again, it's not hard to see why so many traders are buying downside insurance on MU stock. People are genuinely concerned that volatility could materialize. But here's the reason why this fear could ironically be the fuel that keeps Micron stock in play: the smart money is buying protection, not outright selling the security.

Obviously, by not selling, MU isn't suffering from acute downside pressure. More importantly, the bullish narrative is allowed to nibble forward instead of ravenously soaking up capital. The latter dynamic is what typically contributes to reflexive selling. Here, Micron stock is elevated but the rise is disciplined, not unrestrained and chaotic.

Also, with traders buying downside protection, calls are relatively cheap. So, if you had justification for buying, MU stock would technically be a discount.

Right now, the Black-Scholes model for the Feb. 20 options chain is calling for an expected price range between $340.82 and $449.86. This dispersion is essentially a symmetrical distribution that falls within one standard deviation of the current spot price while accounting for volatility and days to expiration.

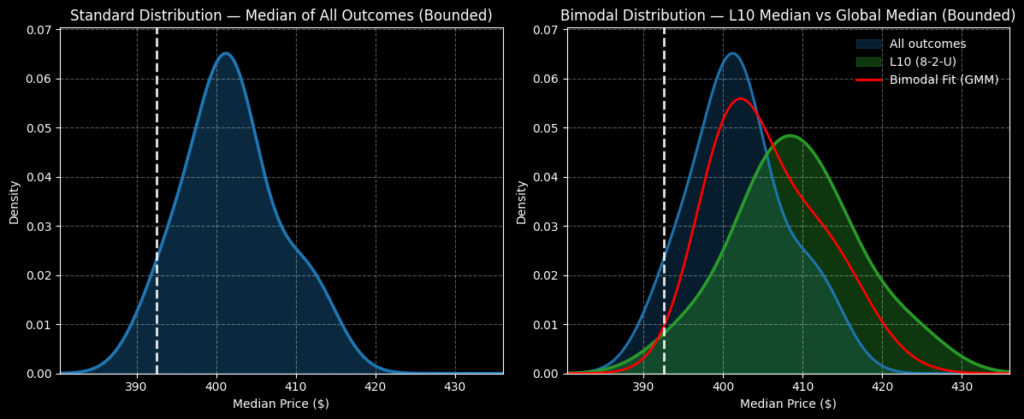

Unfortunately, the above dispersion doesn't tell us where MU stock is likely to congregate on Feb. 20. For that, we need a second-order analysis and that's where the Markov property comes into view. Under Markov, the future state of a system depends solely on the current state. In other words, everything is contextual.

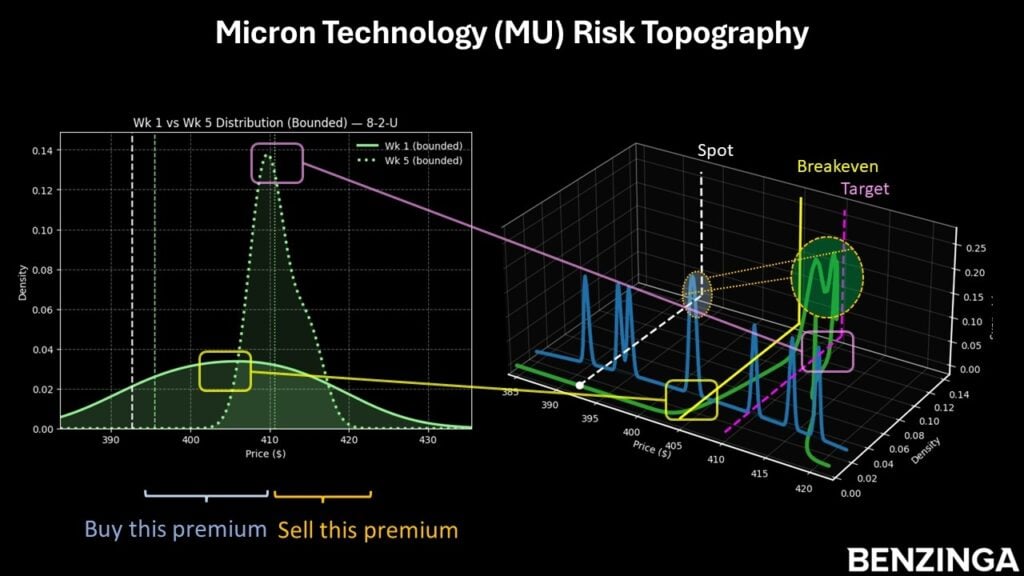

For MU stock, the current context is that, in the trailing 10 weeks, the security printed eight up weeks, leading to an upward slope. Under this 8-2-U sequence, the next 10 weeks would likely range between $380 and $440, with probability density peaking around $408. Over the next five weeks, the expected range would most likely fall between $400 and $420, with probability density also peaking around $408.

In many ways, betting on MU stock is like a contrarian's contrarian bet. While the market is obviously bullish on Micron, there is a natural tendency to be skeptical about blisteringly hot securities. However, in Micron's case, there is both a fundamental and statistical reason why optimism may be justified.

With that said, I'm looking at the 400/410 bull call spread expiring Feb. 20. This wager involves two simultaneous transactions: buy the $400 call and sell the $410 call. The net debit required is $480, which is the most that can be lost.

Should MU stock rise through the second-leg strike ($410) at expiration, the maximum profit would be $520, a payout of over 108%. Breakeven lands at $404.80, thereby improving the probabilistic credibility of the trade.

The opinions and views expressed in this content are those of the individual author and do not necessarily reflect the views of Benzinga. Benzinga is not responsible for the accuracy or reliability of any information provided herein. This content is for informational purposes only and should not be misconstrued as investment advice or a recommendation to buy or sell any security. Readers are asked not to rely on the opinions or information herein, and encouraged to do their own due diligence before making investing decisions.

Image: Shutterstock

| 6 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why Tesla, Google, and other Mag 7 stocks are losing billions in valuation

MU -6.99%

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Is Wall Street buying Intel's comeback story after blowout Q2 earnings?

MU -6.99%

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite