|

|

|

|

|||||

|

|

|

Healthy competition helps drive innovation and in turn, investor returns.

That’s exactly what we’ve seen between two of the world’s largest chipmakers. The past year has been particularly noteworthy for Advanced Micro Devices, which not only staged a strong recovery but meaningfully outperformed Nvidia, the longtime AI leader.

In terms of percentage returns, AMD shares rose approximately 77% in 2025, nearly doubling Nvidia's more modest 39% gain. While the two stocks moved in tandem during the first half of the year, the divergence gained steam in the latter half, particularly after AMD inked a multi-year deal to power OpenAI’s next-generation AI infrastructure.

AMD CEO Lisa Su referred to the partnership as a “true win-win, enabling the world’s most ambitious AI buildout and advancing the entire AI ecosystem.” The terms of the deal included deploying 6 gigawatts of AMD GPUs.

As we progress into 2026 with AMD trading around $250 per share in mid-January, the stock’s story remains compelling. The company's disciplined execution and expanding AI footprint provide a sincere opportunity for those seeking exposure to the ongoing data center transformation.

AMD's ascent in 2025 stemmed from a confluence of factors that highlighted its evolution from a perennial challenger to a credible threat in high-performance computing. The data center segment, now the core growth engine, delivered record revenue throughout the year. In Q3 2025, this segment posted $4.3 billion in revenues—up 22% year-over-year—driven by robust demand for 5th Gen EPYC processors and Instinct accelerators.

AMD’s MI300 series ramps exceeded expectations, securing wins with major hyperscalers and enterprises seeking alternatives amid Nvidia supply constraints and pricing pressures. Management's guidance for greater than 60% CAGR in data center revenue over the next several years underscored this momentum, reflecting confidence in product superiority and ecosystem partnerships.

A pivotal moment came with the MI355X accelerator, positioned as a cost-effective competitor to Nvidia's offerings, gaining traction for its performance-per-dollar advantages. This helped AMD capture incremental share in inference workloads, where efficiency matters as much as raw training power.

Client and gaming segments also contributed, with Ryzen processors benefiting from AI PC refreshes. Overall, AMD's total revenue growth accelerated to the mid-30% range during the third quarter of last year, translating into sharp earnings expansion and a consistent trend of exceeding expectations.

In contrast, Nvidia – while still dominant with explosive growth earlier in the cycle – faced a higher bar in 2025. Its shares advanced solidly but lagged AMD as investors digested potential saturation in training demand, export restrictions impacting China revenue, and a premium valuation that left less room for error.

Nvidia's NVDA quarterly growth remained impressive, but AMD's relative undervaluation at the time—trading at lower forward multiples despite comparable AI exposure—drew rotation. AMD's gains were amplified in the year's second half, as evidence mounted of diversifying customer bases and open ecosystems reducing Nvidia lock-in risks.

This outperformance wasn't a mere catch-up; it signaled structural shifts. In addition to the OpenAI deal, partnerships with Microsoft, Meta, and Oracle for custom deployments provided validation for AMD shareholders.

Looking to 2026, there’s no doubt that AMD AMD stock still holds appeal. The AI inferencing market—projected to grow faster than training—is AMD's sweet spot, with MI400 series accelerators unveiled at CES 2026 promising significant leaps in efficiency and scale. The full MI400 lineup, including Helios racks for exascale computing, positions AMD to capitalize on broadening deployments beyond hyperscalers.

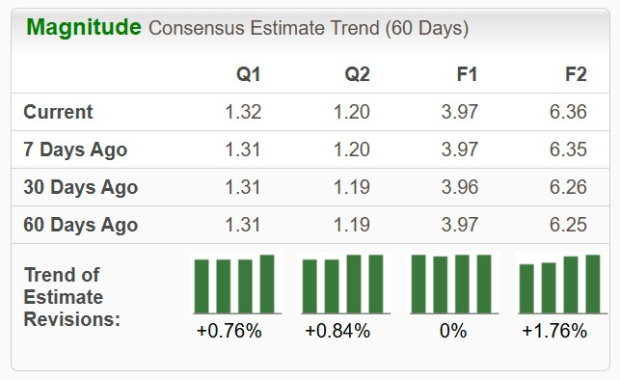

The upcoming Q4 2025 earnings report is set to be released on February 3rd and should be a key catalyst. Analysts have bumped up EPS estimates by 0.76% in the past 60 days. The Zacks Consensus Estimate now stands at $1.32 per share, reflecting a 21.1% improvement versus the year-ago period. Revenues are anticipated to jump 26% to $9.65 billion.

The Zacks Earnings ESP (Expected Surprise Prediction) indicator seeks to find companies that have recently seen positive earnings estimate revision activity. This more recent information has proven to be very useful in finding positive earnings surprises, giving investors a leg up during earnings season. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time according to our 10-year backtest.

AMD is currently a Zacks Rank #3 (Hold) stock and boasts a +2.01% Earnings ESP. Another beat may be in the cards when the company reports its Q4 results in early February.

In reflecting on this dynamic duo, competition ultimately benefits the industry—pushing boundaries in power efficiency and accessibility.

For investors, AMD offers a balanced way to participate in AI's next phase. It's a story of perseverance paying off, and one worth considering thoughtfully.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite